Don’t be afraid of fintech. The truth is, you can optimize almost every investment using fintech effectively.

Don’t be afraid of fintech. The truth is, you can optimize almost every investment using fintech effectively.

Fintech is a popular term used to describe financial technology, an innovation that aims to compete with traditional commercial methods in the delivery of financial services. Typically, fintech is divided into 10 categories:

- Mortgage and real estate

- Lending

- Blockchain and cryptocurrency

- Payments and billing

- Personal finance

- Regulation technology

- Insurance

- Capital markets

- Wealth management

- Money transfer and remittance

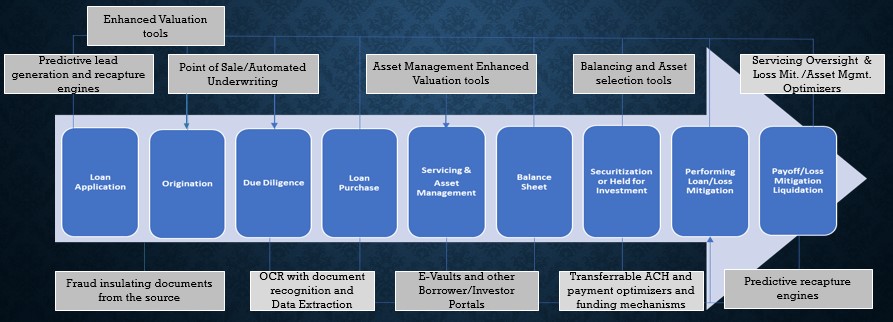

Integrated properly into both the trading and operational side of the mortgage lifecycle, fintech can not only increase margins but also allow for lenders to originate more loans in less time and in a more efficient and secure manner. Additionally, by using fintech throughout the mortgage lifecycle, each phase of management is enhanced and therefore produces optimized outcomes leading to better investment returns, while still providing the borrower with a great customer experience.

A “High Level” Tech-Enabled Residential Mortgage Lifecycle*

*This chart is provided as a “high level” example of what types of fintech can optimize the lifecycle. It is not to be considered a complete integration or feature roadmap.

Is All Fintech Created Equal?

The simple answer is, no. It takes time and effort to find the proper fintech partners and solutions for your business. We have spent over two years dissecting a vast array of fintech platforms to find those that work for the operating businesses we all run every day. Also, there is a “knowledge gap” at times between technology thought leaders and the business operators.

If the fintech companies do not understand what lenders do, they cannot provide you with solutions. The name that is the most familiar to you may not have the best product.

The Right Balance?

Fintech companies in partnership with industry veterans that have sat in the seats of each “stakeholder” to ensure that what you are looking to streamline, enhance, and achieve can truly be accomplished and if it cannot today, providing you with this truthful feedback. With increased regulation and the vast array of other challenges in today’s market, you need to be in the specific businesses (origination, servicing, structured finance, etc.) to truly understand the challenges that these businesses, face each day.

So, if an “industry veteran” is no longer sitting in a seat similar to yours, for example, building or operating loan business, servicing assets, or structuring bonds themselves, they will not be up to date on the actual challenges facing your business.

Fintech: An Opportunity for Non-Bank Lenders

Deals in fintech financing rose by almost 20 percent to $27.4 billion in 2017, with the value of transactions in the United States increasing by over 30 percent to $11.3 billion. In just this one year, the number of fintech deals rose from approximately 1,800 in 2016 to nearly 2,700 in 2017, as more investors gravitated toward this type of investment.

Since 2013, 80 percent of the top 50 banks by total assets operating in the United States have not acquired a fintech startup. These banks include Bank of America, Wells Fargo, Citibank, and Morgan Stanley, but they are now beginning to catch up. Since September 2017, there have been six fintech acquisitions by five different banks, of which four were making their first fintech acquisition (JPMorgan, BNP Paribas, Credit Suisse, and TD Bank). This equates to more than half of the number of acquisitions made between 2013 and 2017.

Also, major technology platforms such as Amazon, PayPal, and Quickbooks are now pursuing business lending, which are data-driven products, to enhance the value of their primary businesses. Amazon has also recently announced that they intend to take on mortgages.

Smaller businesses have one crucial challenge: obtaining financing. According to a Federal Reserve study, 70 percent of companies that are less than five years old are in need of funding to grow, but only approximately 23 percent of them can secure funding. Recognizing this, these companies are using the data they’ve accumulated to reinvent traditional business lending models to provide capital to these clients.

The thought is that by automating collection methods and improving underwriting techniques, Amazon, PayPal, and Quickbooks could pose a significant long-term threat to traditional lenders, as well as newcomers in the mortgage and alternative lending spaces. This is why it is so important to focus on fintech now. By doing this and executing efficiently, you can strive to compete in a market that is moving quickly toward a “big tech” world.