While mortgage balances in the United States ticked up slightly over-the-year in Q2, home equity lines of credit (HELOC) balances dropped by 4.2 percent—their 26th consecutive quarter of annual declines, according to the Household Debt and Credit Report for Q2 2016 released Tuesday by the New York Fed.

While mortgage balances in the United States ticked up slightly over-the-year in Q2, home equity lines of credit (HELOC) balances dropped by 4.2 percent—their 26th consecutive quarter of annual declines, according to the Household Debt and Credit Report for Q2 2016 released Tuesday by the New York Fed.

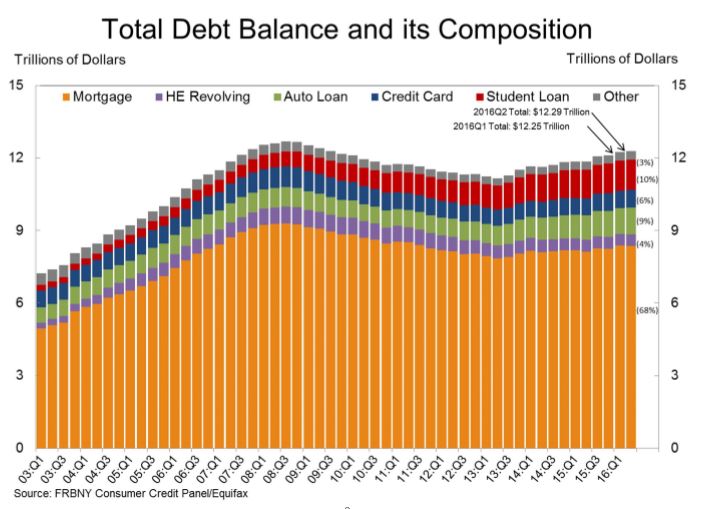

As of the end of the second quarter, mortgage balances shown on consumer credit reports totaled $8.36 trillion, which was an increase of 2.6 percent over the previous year. The increase in mortgage balances is likely due to the increase in mortgage originations and new extensions of credit during Q2. Mortgage balances totaled $427 billion during the quarter, the New York Fed reported.

During their 26 consecutive quarters of decline, HELOCs have shrunk by a total of 32.3 percent. By contrast, mortgage debt rose by about 3 percent, or $246 billion, its 11th consecutive quarter of increase. Home mortgage debt has increased by 5.9 percent during those 11 quarters but is still currently 10 percent lower than its pre-recession peak level.

Why are HELOC balances on the decline for 26 quarters and counting while overall mortgage debt has been rising for 11 quarters and counting?

For starters, HELOCs that were originated during the housing bubble are reaching their 10-year end of draw period and some borrowers cannot handle the payment shock from a higher interest rate or principal amortization, according to Michael Neal, Senior Economist with the National Association of Home Builders (NAHB). The result is that many of the HELOCs originated during the bubble are becoming delinquent, and some are becoming seriously delinquent (90 or more days past due)—which ultimately results in a decline in HELOC balances. While banks are originating more mortgages, they may not be so much with HELOCs due to the number of serious delinquencies.

“Ultimately balances that are seriously delinquent have a high likelihood of entering default,” Neal said, while also noting that high delinquency rates on HELOCs tend to “make banks shy about originating more of them.”

The New York Fed reported that the serious delinquency rate on mortgages is 1.8 percent as of the end of Q2, whereas for HELOCs the rate is 2.0 percent.

The New York Fed reported that the serious delinquency rate on mortgages is 1.8 percent as of the end of Q2, whereas for HELOCs the rate is 2.0 percent.

“It’s not that great of a difference,” Neal said. “But if you compare it to what it was pre-boom, you’ll see it’s not what we’re accustomed to.”

Neal reported last year for the NAHB that the 20 largest banks are where HELOC balances are shrinking. In 2001, HELOC balances at the 20 largest banks was nearly equal to all other banks combined; in 2003, however, the balances of HELOCs at the 20 largest banks soared while it began to decline for all other banks. The result as a peak of $475.9 billion in HELOC balances in 2009 for the 20 largest banks; by 2015, however, that number had fallen to $315 billion. Meanwhile, the outstanding HELOC balances for all other banks has held steady and not endured the same up-and-down cycle as they have at the 20 largest banks; for all other banks, HELOC balances totaled $163.3 billion in 2015.

“Since the outstanding amount of HELOCs on the balance sheets of all other banks is rising while declining at the Top 20 banks, then the gap between the two cohorts is converging,” Neal said.

Click here to view the New York Fed’s complete report for Q2 2016.