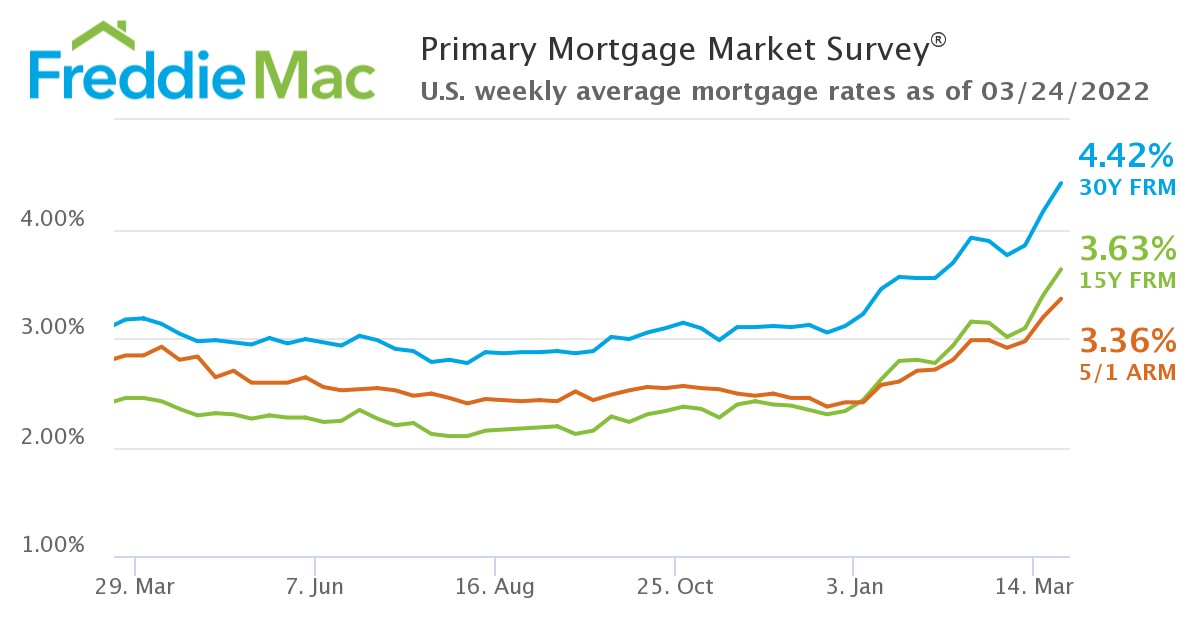

As anticipated with news of last week’s Fed funds rate hike, Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) showed that the 30-year fixed-rate mortgage (FRM) averaged 4.42% this week for the week ending March 24, 2022, up from last week when it averaged 4.16%. A year ago at this time, the 30-year FRM averaged 3.17%.

As anticipated with news of last week’s Fed funds rate hike, Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) showed that the 30-year fixed-rate mortgage (FRM) averaged 4.42% this week for the week ending March 24, 2022, up from last week when it averaged 4.16%. A year ago at this time, the 30-year FRM averaged 3.17%.

It had been approximately four years since the Federal Reserve Open Market Committee (FOMC) cut interest rates in an emergency meeting in light of COVID-19; however that changed last week as the FOMC raised the nominal interest rate by 25 basis points to 0.25-0.50%.

“This week, the 30-year fixed-rate mortgage increased by more than a quarter of a percent as mortgage rates across all loan types continued to move up,” said Sam Khater, Freddie Mac’s Chief Economist. “Rising inflation, escalating geopolitical uncertainty and the Federal Reserve’s actions are driving rates higher and weakening consumers’ purchasing power. In short, the rise in mortgage rates, combined with continued house price appreciation, is increasing monthly mortgage payments and quickly affecting homebuyers’ ability to keep up with the market.”

Also this week, Freddie Mac reported the 15-year FRM averaged 3.63% with an average 0.8 point, up from last week when it averaged 3.39%. A year ago at this time, the 15-year FRM averaged 2.45%. The five-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.36% with an average 0.3 point, up from last week when it averaged 3.19%. A year ago at this time, the five-year ARM averaged 2.84%.

Evidence of affordability issues can be seen in the latest mortgage application volume report from the Mortgage Bankers Association (MBA), as overall application volume fell 8.1% week-over-week on the heels of the Fed rate hike.

"Real estate markets reached unprecedented territory during the past two years of the pandemic. From the shock of never-before-seen mass quarantines and towering job losses, to the eye-watering monetary and fiscal stimulus, American homes played a central role, serving as shelter, work places, virtual schools, gyms and safe havens," said Realtor.com Manager of Economic Research George Ratiu. "Forbearance measures and rock-bottom mortgage rates ensured that families kept their abodes, and enabled many to buy their first home. However, the window of record-breaking mortgage rates has closed, and the road ahead points to a return toward rates more typical of the past two decades. For buyers and sellers, this spring will offer a period of transition, in which high prices will combine with rising interest rates to challenge budgets already contending with high inflation. The bottom line is that at today’s rate, the buyer of a median-priced home is spending $375 per month more on their monthly payment than they did a year ago. Predictably, we’re seeing early signs of market adjustment, with sales of both new and existing homes down.”

Higher rates are impacting refinance options for most Americans, as last week, as the refinance share of mortgage activity decreased to 44.8% of total applications, down from 48.4% the previous week.

Limited supply is driving up prices and pricing many out of the market, as the U.S. Department of Housing & Urban Development (HUD) and the Census Bureau reported the median sales price of new houses sold in February 2022 stood at $400,600, with the average sales price hitting $511,000.

“Affordability is a growing challenge as higher new-home prices and rising rates may be pricing out some buyers,” said First American Deputy Chief Economist Odeta Kushi. “One year ago, 31% of new home sales were priced below $300,000. In February 2022, only 18% of new home sales were priced below $300,000.”