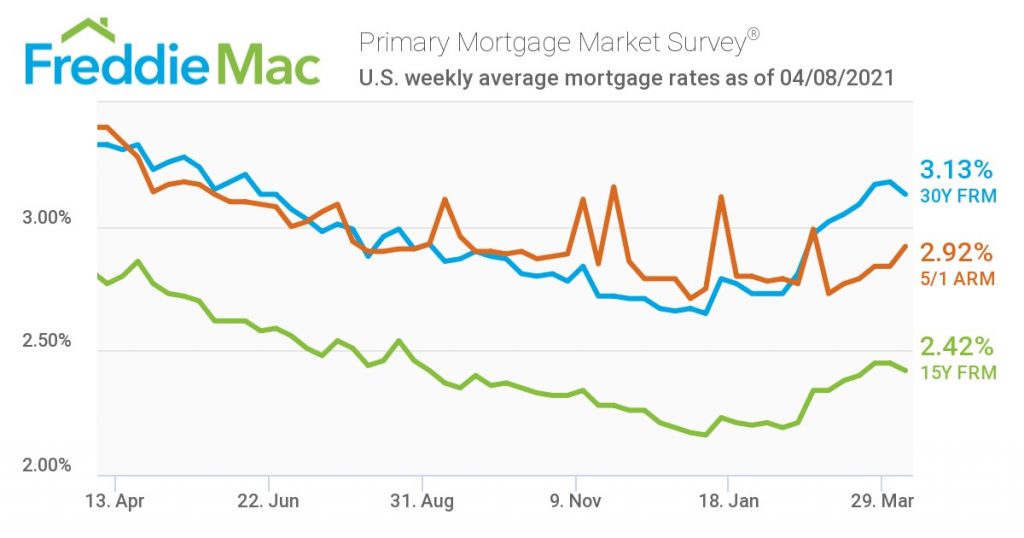

In a change of trend, mortgage rates dropped this week for the first time after seven weeks of rising, as Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) reports rates dropping to an average 3.13% for the week ending April 8, 2021, down from last week’s total of 3.18%.

In a change of trend, mortgage rates dropped this week for the first time after seven weeks of rising, as Freddie Mac’s latest Primary Mortgage Market Survey (PMMS) reports rates dropping to an average 3.13% for the week ending April 8, 2021, down from last week’s total of 3.18%.

“After moving up for seven consecutive weeks, mortgage rates have dropped due to the recent, modest decline of U.S. Treasury yields,” said Sam Khater, Freddie Mac’s Chief Economist. “As the economy recovers, it should experience a strong rebound in the labor market. Combined, these positive signals will continue to bolster purchase demand. The drop in rates creates yet another opportunity for those who have not refinanced to take a look at the possibility.”

Last year, the 30-year fixed-rate mortgage (FRM) stood at 3.33%.

Also this week, the 15-year fixed-rate averaged 2.42% with an average 0.6 point, down from last week when it averaged 2.45%. A year ago at this time, the 15-year FRM averaged 2.77%. The five-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.92% with an average 0.1 point, up from last week when it averaged 2.84%. A year ago at this time, the five-year ARM averaged 3.40%.

“Even with the positive numbers in the service sector as well as the jump in job openings, investors remained wary of the economic outlook as the Federal Reserve argued for continued monetary support, keeping funds flowing into bonds,” said realtor.com Senior Economist George Ratiu. “With the 10-year Treasury rate sliding, these moves pushed Freddie Mac’s interest rate down.”

And as rates may be slipping, those on the fence considering refis are now faced with either jumping in or waiting to see what lies ahead.

The Mortgage Bankers Association (MBA) reported that the refinance share of mortgage activity volume last week tailed off slightly to 60.3% of total applications from 60.6% the previous week.

Even with rates declining, short supply and high sale prices nationwide continues to pose an issue for would-be homebuyers. CoreLogic reported that home prices reached a 15-year high in February, as demand continues to clash with historically low supply, as prices increased 10.4% nationally, 1.2% over January 2021’s totals.

“Realtor.com’s latest weekly data show listing prices 17.2% higher than a year ago, as buyers snap up homes as soon as they hit the listing portals, and new supply remains scarce,” said Ratiu. “Sellers are locked in a Catch-22, unable to find suitable a replacement home before listing their existing one, further contributing to the vacuum of homes for sale. For buyers, rising rates mean higher monthly payments and lower budgets. The monthly payment for a median loan with a 20% down payment exceeds $1,210, the same level as what markets saw at the housing market’s pre-COVID pandemic peak during 2018-19. Without a significant boost to inventory, we can expect sales activity to come in below expectations during the critical spring season.”