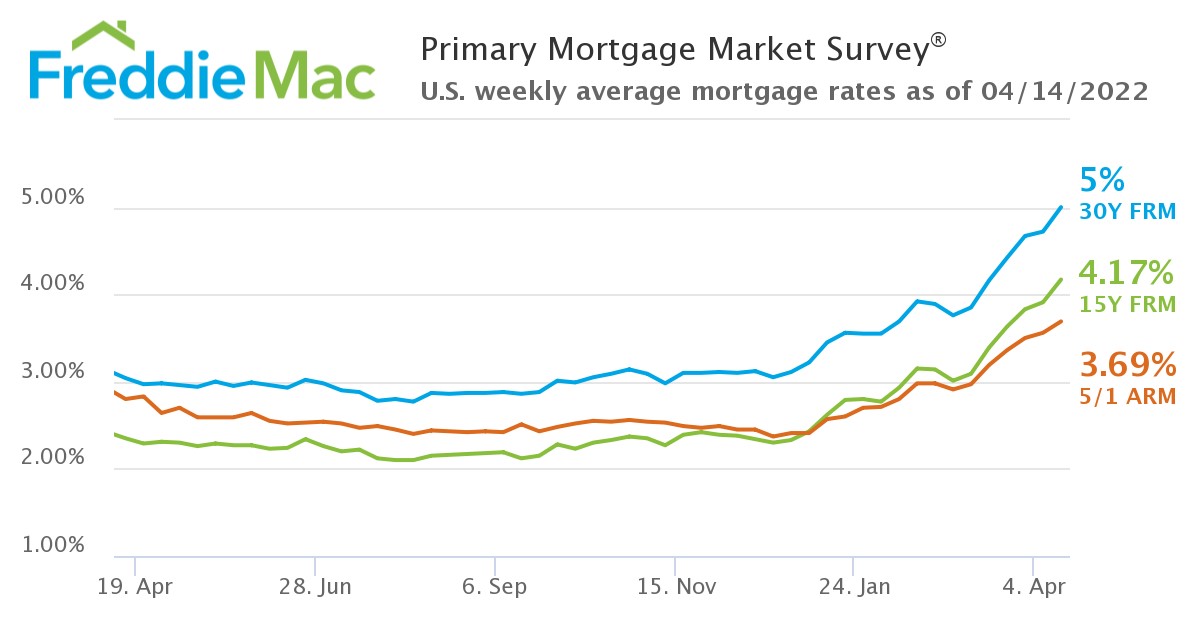

After mortgage rates fell to all-time lows just 15 months ago, for the first time since 2011, mortgage rates have hit the 5% mark, as reported by Freddie Mac in its weekly Primary Mortgage Market Survey (PMMS). By reaching 5%, fixed-rate mortgages (FRMs) were up week-over-week as last week, they averaged 4.72%. A year ago at this time, the 30-year FRM stood near two full percentage points lower at 3.04%.

After mortgage rates fell to all-time lows just 15 months ago, for the first time since 2011, mortgage rates have hit the 5% mark, as reported by Freddie Mac in its weekly Primary Mortgage Market Survey (PMMS). By reaching 5%, fixed-rate mortgages (FRMs) were up week-over-week as last week, they averaged 4.72%. A year ago at this time, the 30-year FRM stood near two full percentage points lower at 3.04%.

“This week, mortgage rates averaged five percent for the first time in over a decade,” said Sam Khater, Freddie Mac’s Chief Economist. “As Americans contend with historically high inflation, the combination of rising mortgage rates, elevated home prices and tight inventory are making the pursuit of homeownership the most expensive in a generation.”

Also this week, the 15-year FRM averaged 4.17% with an average 0.9 point, up from last week when it averaged 3.91%. A year ago at this time, the 15-year FRM averaged 2.35%. The five-year Treasury-indexed hybrid adjustable-rate mortgage (ARM), a product gaining in popularity amid the rise in rates, averaged 3.69% with an average 0.3 point, up from last week when it averaged 3.56%. A year ago at this time, the five-year ARM averaged 2.80%.

“Higher costs and declining real wages weigh heavily on people contemplating housing choices this spring,” added Realtor.com Manager of Economic Research George Ratiu. “On one hand, rents are hitting new records in markets across the country, as landlords look to make up for lost income during the pandemic. Higher rents are encouraging many tenants to take a second look at buying a home, especially in cities where a mortgage payment may be on par or lower than monthly rent.”

Realtor.com’s Monthly Rental Report found that U.S. rental prices grew from March 2020 to 2022 during the pandemic, as median rental prices hit a new high of $1,807 in March, up 19.3% in just two years.

“While the jobs market is strong, it's unlikely that we'll see enough income growth to keep rents under 30% of monthly paychecks–especially with higher inflation and everyday costs,” said Realtor.com Chief Economist Danielle Hale. “Still, there is a silver lining for renters, as rents won't be able to sustain an accelerated pace if incomes can't keep up."

Affordability woes continue for buyers as Redfin reports that 32% of renters nationwide are doing so because they cannot afford to buy a home in the area they desire to live in. The same report found that while 30% of renters are unable to save for a down payment, 45% claim debt is preventing them from buying a home.

And those who can afford to move on from renter to homeowner are faced with the challenge of limited supply, as Redfin also reported that the number of active listings now sits at 381,950, a number that is down 18.9% year-over-year, and is also down 62.3% year over year, from the onset of the COVID-19 pandemic in March 2020. This means that for every five homes that were for sale before the pandemic, there are only two homes today.

“On the other hand, the for-sale market continues to be undersupplied, making it difficult to find an affordable home,” added Ratiu. “However, some relief might be on the way this spring, according to Realtor.com’s latest weekly data. The number of new listings rose for the second week in a row and there are signs of moderation in the pace of sales and price gains. The fresh supply of homes hints at a housing market taking its foot off the accelerator and beginning to coast toward a new normal. For now, many first-time buyers are still feeling the sting of sticker shock, with the mortgage payment for a median-priced home running $530 above a year ago, adding over $6,300 to the annual housing budget.”