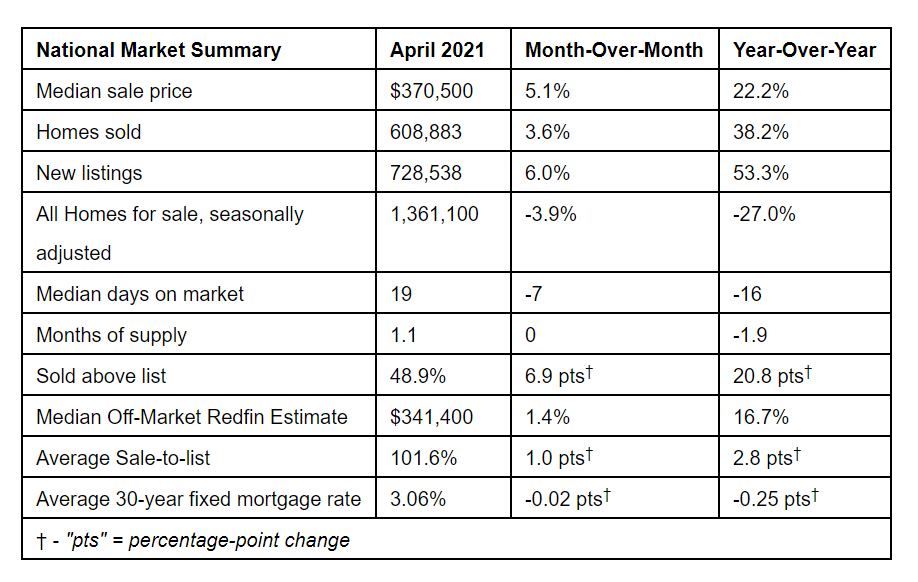

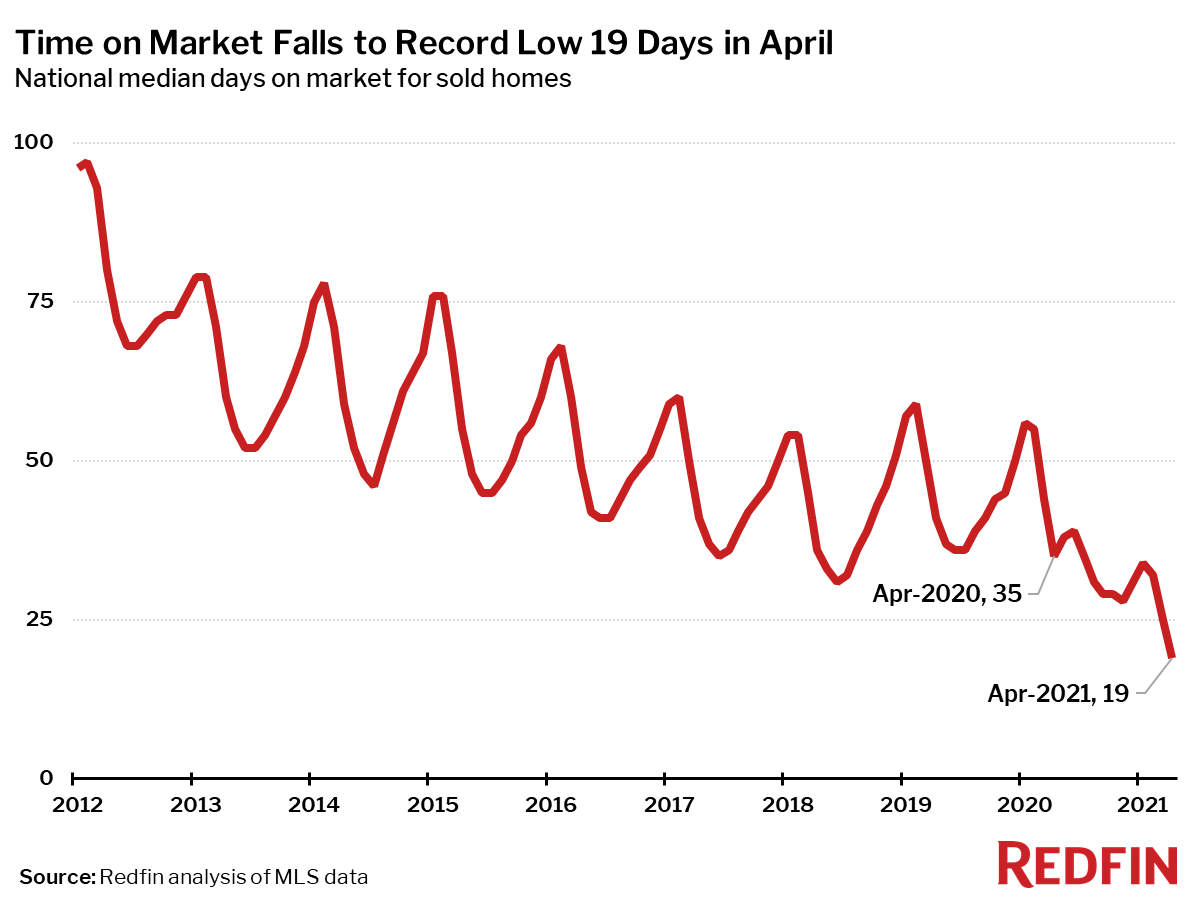

Scarce supply is leading to lightning-fast sales in some markets, as Redfin reported that in April 2021, the typical single-family home went under contract in 19 days, 16 days fewer than just a year ago and the fastest pace on record. Combined with the speed in which homes are selling, the national median home-sale price hit a record high of $370,528 in April, up 22% year-over-year from April 2020.

Scarce supply is leading to lightning-fast sales in some markets, as Redfin reported that in April 2021, the typical single-family home went under contract in 19 days, 16 days fewer than just a year ago and the fastest pace on record. Combined with the speed in which homes are selling, the national median home-sale price hit a record high of $370,528 in April, up 22% year-over-year from April 2020.

"To put the scarcity of housing into context, there is plenty of room for supply to increase and demand to taper off, and we would still find ourselves in a historically strong seller's market," said Redfin Chief Economist Daryl Fairweather. "While Americans brace themselves for a lot of changes as workplaces and schools reopen, the story of the housing market will largely remain the same. There simply aren't enough homes for sale in America for everyone with the desire and the means to buy one right now. Until new construction takes off—over the course of years, not months—home prices will continue to increase. This housing boom is nowhere close to over."

Regionally, the hottest market in terms of days listed was Indianapolis where the typical home went under contract after just four days on the market in April, down from 10 days a year earlier. Homes in Denver; Omaha, Nebraska; Portland, Oregon; and Seattle also sold exceptionally fast in April, with half of all homes pending sale in just five days in each of those metros.

April brought with it a drop in housing starts, as the U.S. Department of Housing and Urban Development (HUD) and U.S. Census Bureau reported starts dropping to 1.57 million units in April 2021, down 9.5% from March, but 67.3% above April 2020’s rate of 938,000.

Tight supply and high demand resulted in big paydays for sellers as 49% of homes sold above list price in April, the largest share on record. The average sale-to-list price ratio continued to surge well past 100% in April, hitting a Redfin record high of 101.6%.

California offered three of the five most competitive markets where in Oakland, 81.5% of homes sold above list price; followed by San Jose (78.2%); Tacoma, Washington (73.7%); Austin, Texas (73.7%); and Sacramento (72.5%).

Median sale prices increased from a year earlier in all of the 85 largest metro areas Redfin tracks. Austin boasted the nation’s highest price growth, rising 42.3% since last year to $465,000, followed by Oxnard, California with the second highest growth at 25.8% year-over-year price growth, followed by Miami (25.8%), Phoenix (24.9%), and Tacoma, Washington (24.9%). The smallest increase was found in Honolulu, Hawaii where home prices were up just 0.2% in April year-over-year.

April home sale volume was up 34% from a year earlier, but only 8% from the same time in 2019. Compared to April 2020, home sales rose in all but one of the 85 largest metro areas that Redfin tracks. The only metro area that saw home sales decline was Rochester, New York which saw a 3% decline. The largest gains in sales were found in San Francisco (+184%), San Jose (+150%), and Miami, Florida (+120%).

In terms of housing inventory, the biggest year-over-year declines in active housing supply in April were found in Salt Lake City (-70%); Baton Rouge, Louisiana (-60%); and North Port, Florida (-48%).