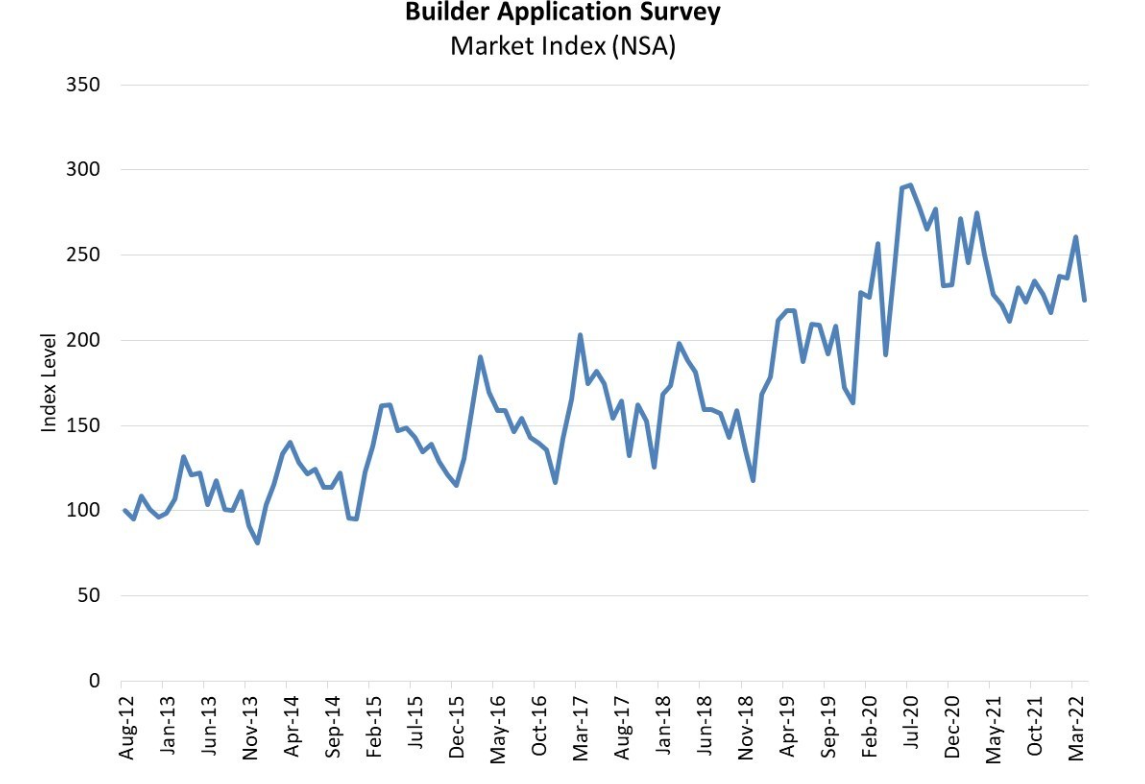

The Mortgage Bankers Association (MBA) Builder Application Survey (BAS) data for April 2022 shows mortgage applications for new home purchases decreased 10.6% compared to a year ago. Month-over-month, mortgage apps decreased by 14% (this change does not include any adjustment for typical seasonal patterns).

The Mortgage Bankers Association (MBA) Builder Application Survey (BAS) data for April 2022 shows mortgage applications for new home purchases decreased 10.6% compared to a year ago. Month-over-month, mortgage apps decreased by 14% (this change does not include any adjustment for typical seasonal patterns).

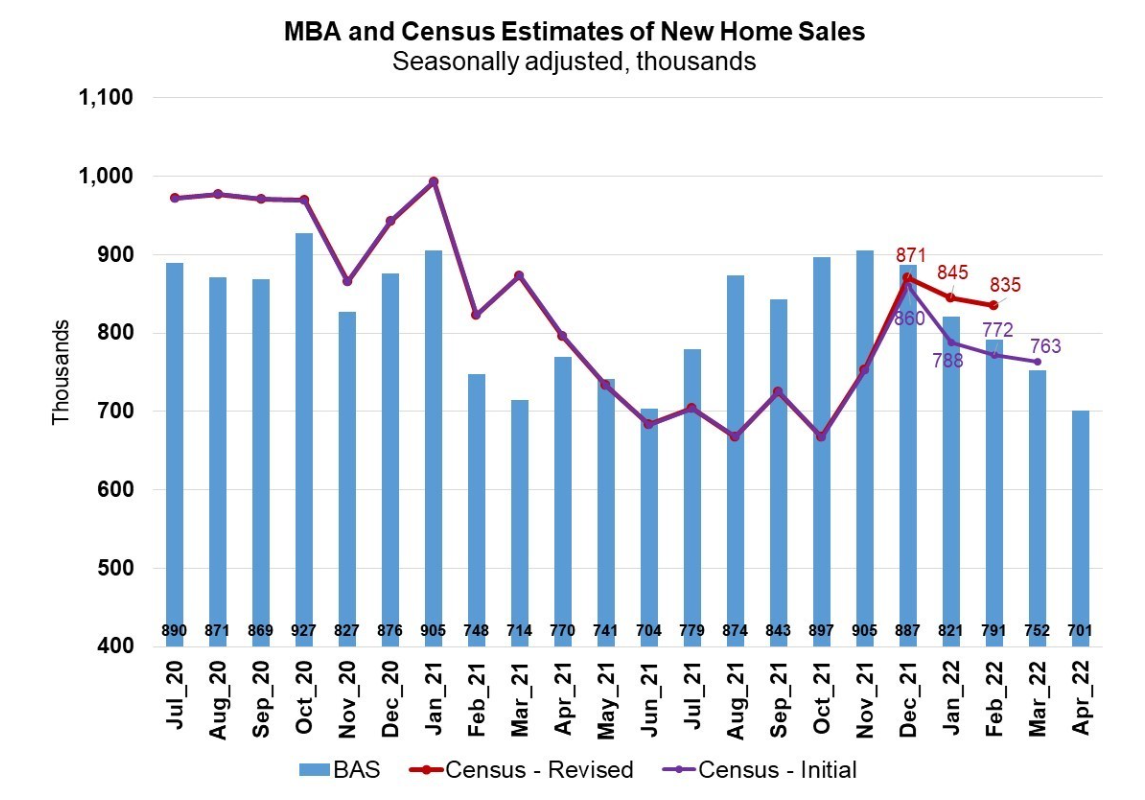

MBA estimates new single-family home sales were running at a seasonally adjusted annual rate of 701,000 units in April 2022.

The MBA’s new home sales estimate is derived using mortgage application information from the BAS, as well as assumptions regarding market coverage and other factors.

“New home purchase activity declined on a monthly and annual basis in April, as the spike in mortgage rates cooled demand, and homebuilders continued to grapple with rising costs, supply-chain issues, and extended completion timelines,” said Joel Kan, MBA’s Associate VP of Economic and Industry Forecasting. “With the supply of existing homes on the market still at extremely low levels, the new home market is an important source of housing supply. However, the pace of construction has slowed in recent months. MBA’s estimate of new home sales declined for the fifth consecutive month to 701,000 units, the slowest sales pace since May 2020.”

The National Association of Home Builders (NAHB) recently reported in its Home Building Geography Index (HBGI) that the rate of year-over-year single-family construction growth in small and large metro urban, suburban and rural regional submarkets slowed in Q1 year-over-year, with notable deceleration in large suburban markets.

Add to that, the NAHB also reported a significant slide in builder confidence in the market for newly built single-family homes, which fell eight points to 69 in May, marking the fifth consecutive month that builder sentiment has declined reaching its lowest reading since June 2020.

The MBA’s BAS reported that the seasonally adjusted estimate for April is a decrease of 6.8% from March’s pace of 752,000 units. On an unadjusted basis, the MBA estimates that there were 65,000 new home sales in April 2022, a decrease of 12.2% from 74,000 new home sales in March.

“The average loan size increased to a new survey high of $436,576, and over half of applications were for loan amounts greater than $400,000,” said Kan. “Higher rates and sales prices and larger loan sizes are eroding housing affordability and pricing some buyers out of the market.”

Freddie Mac reported that the 30-year fixed-rate mortgage (FRM), while sliding the past few weeks, still remains above the 5% mark, further causing affordability issues for many prospective buyers.

By product type, conventional loans composed 76.7% of loan applications, while FHA loans composed 13.1%, RHS/USDA loans composed 0.2%, and VA loans comprised 10.1%.

In terms of average loan size, new homes increased more than $400 month-over-month, from $436,151 in March to $436,576 in April 2022.

However, Redfin reports that more sellers are feeling the pressure to sell and have resorted to dropping the price of their homes amid rising interest rates and growing affordability concerns. More than one in five sellers polled by Redfin dropped their price, the highest rate since October 2019.

“The sudden surge in mortgage rates led to a sudden and significant cooldown in the housing market in May,” said Redfin Economics Research Lead Chen Zhao. “However, mortgage rates are now stabilizing, and homes remain in short supply, so while we do expect home-price growth rates to decline, we don’t expect prices to fall much at the national level. For homebuyers trying to determine the best timing this year, the main benefit of waiting is that there may be less competition as supply starts to build up.”