A recent Fannie Mae report revealed their latest projection of the 2022 real gross domestic product (GDP) to be flat at 0.0 percent growth on a Q4/Q4 basis. The latest GDP reading showed an expected decline in Q2, but recent data point to a return to modest growth in Q3.

As Fannie Mae continues to view the economy as stagnating in light of tighter monetary policy and high inflation, indicators are painting a mixed picture, most prominently the negative GDP readings in the first half of the year despite strong employment growth over the same period. As the full effects of tighter monetary policy and fading fiscal stimulus work through the economy and suppress consumer spending, they expect a moderate contraction to occur in 2023 along with a weakening of the labor market. Their forecast for 2023 GDP on a Q4/Q4 basis is negative 0.4%, unchanged from the prior forecast.

Inflation indicators have been volatile over the past couple months, in part due to swings in energy prices. Since the completion of the July forecast, two consumer price index (CPI) readings have been reported. The June measure came in stronger than expected at 1.3% month-over-month while the July reading was weaker than anticipated at zero percent growth over the month. The latter may indicate the start of a sustained slowdown in future inflation. However, Fannie Mae does not wish to overinterpret a single reading.

Fannie Mae has said they project the underlying inflation trend to be slowing gradually but tenuously, as a rebound in energy commodity prices and/or additional global disruptions to manufacturing could reverse much of the progress seen in July. Fannie Mae currently forecasts the CPI on an annual basis to average 7.2% in Q4 2022 —a slowdown from 8.5% on an annual basis measured for July— with the core measure averaging 5.9%, only modestly lower than the readings in June and July.

They also lowered their 2022 forecast for total home sales slightly to 5.78 million units, a 16.2% decline from 2021, down from their previous forecast of a 15.6% drop. Despite a pullback in mortgage rates over the past month, recent incoming data point to a faster near-term slowdown in sales than expected, especially for new homes. In contrast, the total sales outlook for 2023 was revised upward slightly from 5.15 million to 5.18 million units. Given changes to the outlook for both home sales and mortgage rates, they have slightly lowered their forecast for 2022 mortgage originations to $2.47 trillion —previously $2.53 trillion— while modestly raising the 2023 originations forecast to $2.29 trillion from $2.22 trillion.

The Economy is Stagnating

A puzzle in analyzing the current state of the economy has been the wide divergence between the trends of GDP and employment. GDP is estimated to have declined for two consecutive quarters, while the labor market has remained robust with 528,000 payroll jobs added in July and 461,000 on average added monthly over the first half of the year. Some of this divergence may be a measurement error, potentially in both series.

Real gross domestic income (GDI), a theoretically similar measure to GDP, was positive in Q1, potentially indicating GDP may eventually be revised upward. Further, there is a large recent discrepancy in employment levels measured by the establishment survey, which measures payroll growth, and the household survey, used to estimate the unemployment rate. Similar to GDP and GDI, one possibility is that some of this measured labor market strength may eventually be revised away, shrinking the divergence.

However, Fannie Mae does not believe measurement error fully explains the disconnect between GDP and the labor market. The implication of the current divergence is that economic output per worker is falling quickly. While the series is volatile, Q2 labor productivity fell 4.6% on an annualized basis, the second consecutive quarterly decline. On an annual basis, output per hour of labor worked fell 2.6%, the largest annual decline on record.

There is no certainty as to what is driving this development, but it’s hypothesized that at least three factors are involved:

- The economy is still adjusting to post-COVID norms, and this is leading to a significant amount of physical capital becoming partially obsolete and less productive (an example would be the continued underutilization of commercial office space due to remote working).

- The elevated worker job-switching rate in recent quarters is temporarily suppressing labor productivity as a higher-than-normal share of workers are in new jobs and not yet at full productivity.

- High and volatile inflation is disrupting price signals in the economy that guide labor, capital, and other business resource allocation decisions leading to greater inefficiencies and transaction costs as firms try to adjust. Rising inflation in the 1970s also coincided with periods of negative productivity growth.

Modest economic growth is expected to resume in the near term, but the effects of tightening monetary policy and rolling-off fiscal policy, as well as slowdowns in growth abroad, have not yet fully been felt in the US economy. It's also expected that employment gains to slow over the coming quarters with growth turning negative in 2023, coinciding with a modest recession. The treasury yield curve has more severely inverted over the past month, one of the more historically accurate predictors of upcoming recessions.

This is especially true when the move is driven in part by the long end of the yield curve declining as markets begin to anticipate slower economic growth and a reversal of Federal Reserve policy. Other indicators such as the Institute for Supply Management (ISM) Manufacturing Index and the Empire State Manufacturing Survey are also pointing to slower activity moving forward. Further, the recent pullback in oil and other commodity prices do not appear to be due to improving supply-side conditions but rather concerns over slowing global economic growth, as evidenced by the S&P Global Purchasing Managers’ Index (PMI) reaching a 25-month low and ongoing manufacturing disruptions in China.

Very Volatile Recent Inflation Numbers

The July CPI report was the first in the current inflationary period to come in meaningfully below both consensus and our expectations. Headline inflation was flat over the month, while the annual rate fell from 9.1% in June to 8.5% in July. Much of the deceleration was due to a large pullback in gasoline prices over the month but the month-over-month change in the core index decelerated, as well, to 0.3% from 0.7%. The year-over-year core measure remained at 5.9%.

Most commodity prices have fallen significantly over the last month, which will likely put downward pressure on future inflation measures, both directly in headline measures and indirectly in energy-sensitive core components. A weakening in the demand for goods in the coming months is also expected, which should lead to lower price pressure. However, some of the key drivers of underlying inflation remain. Shelter-related inflation is projected to still drive core inflation well into 2023 due to the lagged effects between rising home and rental prices and when this translates into shelter costs in the inflation measures.

Additionally, while job openings are starting to decline, the labor market remains tight, and the employment cost index, a measure of labor compensation growth, remains above a level consistent with a 2% inflation target. There is a higher than typical level of risk around the topline inflation forecast due to volatility in energy and food prices (oil prices have fallen considerably as of this writing following our forecast’s completion), however, it’s expected that core inflation will slow only modestly over the next couple quarters.

The Fed is projected to moderately slow its pace of tightening by increasing the funds rate by 50 basis points at its next meeting in September, given the benchmark rate is now close to its theoretical neutral rate. However, Chairman Powell at the last Federal Open Market Committee (FOMC) meeting stated that the Fed would be relying less heavily on policy guidance going forward and would now be more “data dependent.” The Fed has another labor report and CPI reading between now and its September meeting. Further weakness in commodity prices would weigh on the August CPI reading and could prompt the Fed to back off its recent trend of 75-basis point hikes, as would a marked slowed down in job growth. It's expected that core inflation will remain high in August and, because the labor market reversed in July what had appeared to be a slowing trend, a 75-basis point hike is still very much on the table. The baseline view is that the Fed Funds rate will peak at around 3.4% by year end, which leaves approximately 100 basis points in hikes remaining to be distributed. However, the risks to this Fed call are on the high side.

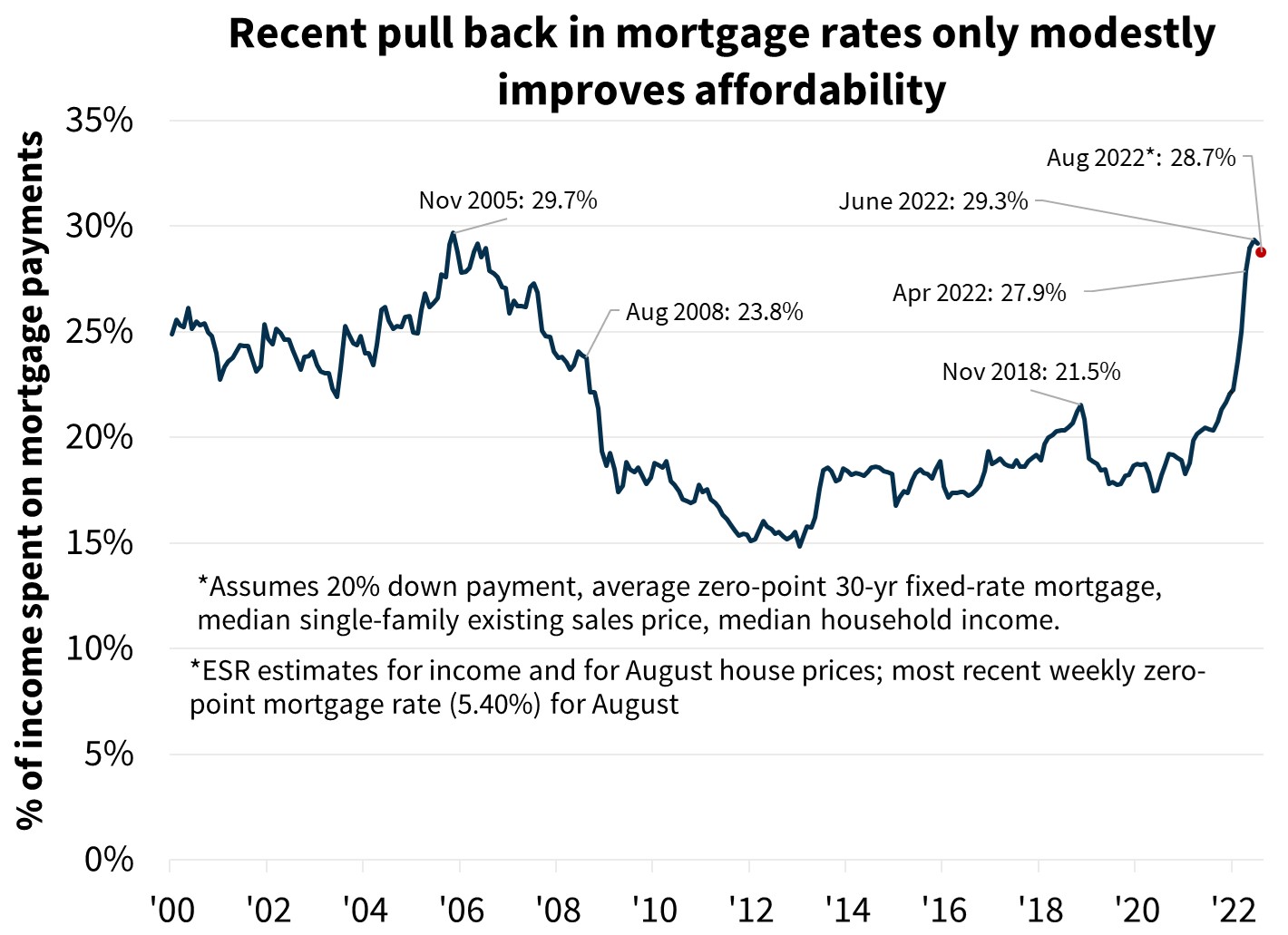

Housing Still Expected to Slow Despite Mortgage Rate Pull Back

Despite mortgage rates pulling back over the past month, now down 59 basis points from the recent peak —5.22% as of the last Freddie Mac survey— Fannie Mae continues to anticipate a slowdown in home sales activity. Even with the mortgage rate decline, housing affordability is still a major constraint for potential homebuyers. As a share of median household income, the estimate of the principal and interest payment on a median-priced home is still just below the highest since 2005. Mortgage rates are up about 235 basis points from a year earlier and house prices have appreciated on an annual basis by 19.4% through Q2 according to the Fannie Mae House Price Index. Additionally, a strong “lock-in” effect for consumers remains: Many existing homeowners are likely reluctant to move due to having a current mortgage with a rate well below current market rates. At 5.22%, it’s estimated that 84% of outstanding mortgages are at least 100 basis points below current market rates.

While June existing home sales were somewhat stronger than anticipated, recent leading indicators of July home sales, such as pending sales and mortgage applications, point to a continued slow down. Pending sales, which lead closings by approximately 30-45 days on average, fell 8.6% over the month in June. In total, Fannie Mae has modestly downgraded their 2022 existing home sales outlook to 5.14 million, down 16% from 2021 existing sales.

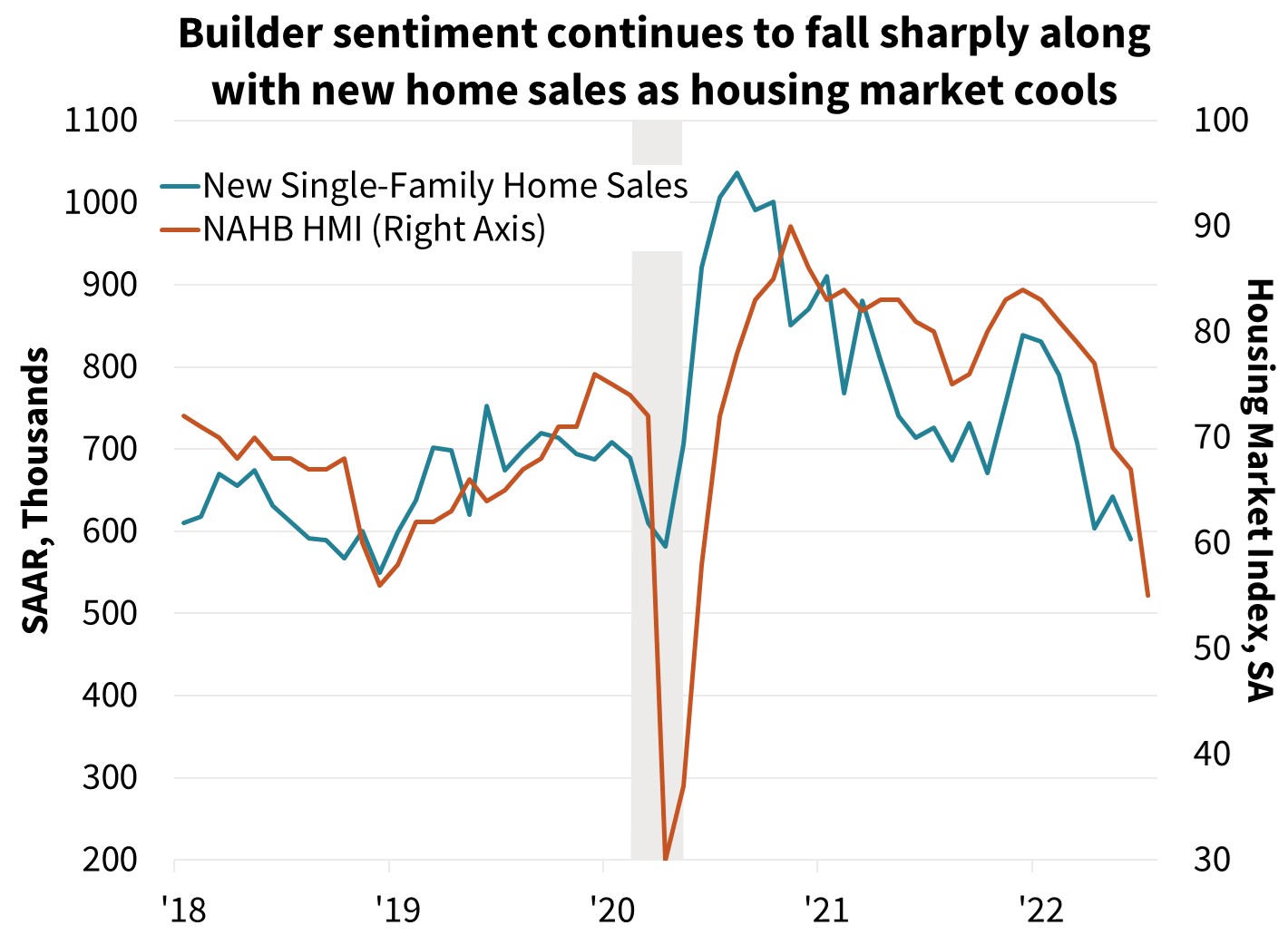

New homes sales came in weaker in June than we had anticipated, falling 8.1% to an annualized pace of 590,000 units. This was the lowest sales pace since the recovery following the initial COVID outbreak. Fannie Mae also revised downward their new home sales outlook for 2022 to 632,000 units, down from 668,000 previously.

Homebuilders are increasingly building up an inventory of homes for sale: As a ratio of the current sales pace, the months’ supply of homes for sale rose to 9.3 in June, the highest since 2010. Many of these homes are empty lots for sale. However, even limiting this measure to homes either under construction or completed points to a rising trend. The months’ supply of homes for sale that have already been started rose to 7.1, also the highest since 2010. It's believed that this growing inventory of new homes for sale will reduce single-family housing starts as home builders slow their construction plans due to growing inventories. The National Association of Home Builders survey recently fell below 50 for the first time since spring 2020, indicating respondents, on net, believe market conditions are poor.

For-sale home inventories are growing, up 28% from a year ago according to realtor.com, but remain low by historical standards. The months’ supply of existing home inventory was still 3.0 months in June according to the National Association of Realtors. This is up from a recent low of 1.6 months in January but remains historically low. Therefore, it's expected overall for-sale inventories to remain tight for the foreseeable future, with some relief coming from the eventual completion of new homes as move-up buyers will vacate their existing units. The future completion of new homes is projected to contribute to slowing house price growth and help with affordability.

Multifamily housing construction continues to be strong. Fannie Mae has recently upgraded their forecast for multifamily construction starts for the remainder of the year and into 2023. Activity is projected to slow in 2023 along with a slowing economy, but demand for rental units remains strong, and if affordability for single-family home purchases remains stressed, many households will likely turn to rental units.

Mortgage Market

Project total mortgage originations are projected to be $2.47 trillion in 2022, a downward revision of $61 billion from July’s forecast. In 2023, total originations are expected to fall further to $2.29 trillion. However, this represents an upgrade of $66 billion from last month’s forecast.

In the purchase market, forecasts have downgraded origination expectation for 2022 by $74 billion to just over $1.7 trillion, given the downward revision to the housing forecast and lower incoming home sales price data for Q2. The forecast for 2023 purchase volumes have been largely unchanged at just under $1.7 trillion.

In the refinance market, Fannie Mae now expects 2022 volumes to total $769 billion, $13 billion higher than last month’s forecast, driven by lower anticipated mortgage rates. Additionally, 2023 volume is expected to be $592 billion, up $74 billion from last month, reflecting the downward revision to interest rates this month.

To read the full report, including more charts and methodology, click here.