The slowdown in home sales transactions that began as mortgage rates surged in 2022 is expected to continue, leading to a moderation in home price growth and tipping housing market balance away from sellers. Additionally, moderation in home price growth will not be enough for the housing market to be a buyer’s market. Instead, homebuyers will enjoy advantages such as a growing number of homes for sale, but costs will remain high, challenging affordability at a time when overall budgets continue to be constrained.

Homebuyers looking for affordability in 2023 will find that prices aren't coming down, according to the Realtor.com 2023 Housing Forecast. With the housing market beginning a gradual adjustment that could last through 2025, what next year will offer buyers is less competition for a growing number of for-sale homes.

In 2023, Realtor.com forecasts that buyers and sellers can expect:

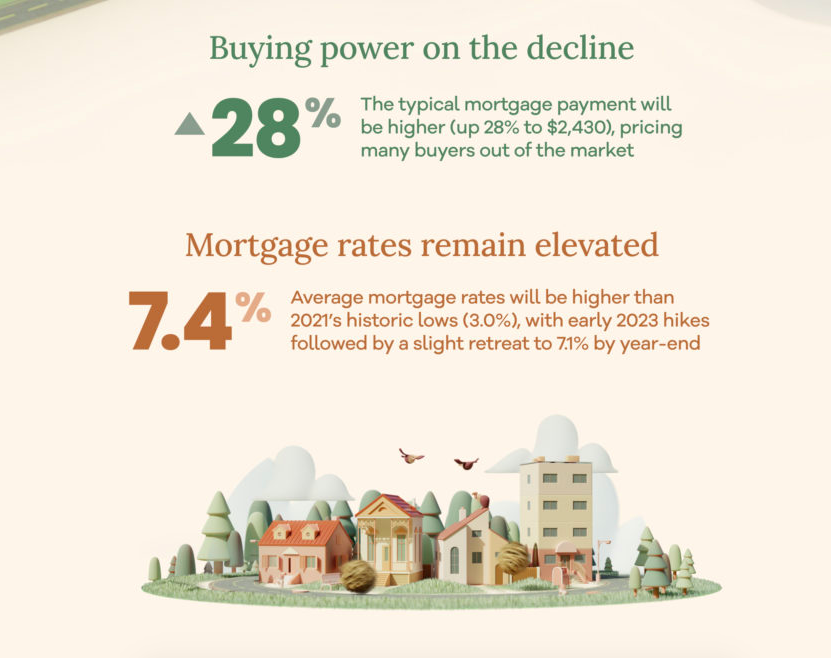

- Average mortgage rates of 7.4%, with early 2023 hikes followed by a slight retreat to 7.1% by year-end.

- Home sales prices won't come down, but growth will moderate to a single-digit yearly pace (+5.4%) for the first time since 2020.

- Rents (+6.3% year-over-year) will outpace home prices and likely hit new highs, further adding to budget pressures – especially for first-time buyers.

- An increase in existing homes for sale (+22.8% year-over-year), as the inventory refresh that began last summer accelerates.

- Home sales will decline 14.1% year-over-year to 4.53 million, the lowest level since 2012.

"Compared to the wild ride of the past two years, 2023 will be a slower-paced housing market, which means drastic shifts like price declines may not happen as quickly as some have anticipated. It will be a challenging year for both buyers and sellers, but an important one in setting the stage for home sales to return to a sustainable pace over the next two to three years," said Danielle Hale, Chief Economist for Realtor.com. "With mortgage rates continuing to climb as the Fed navigates the economy to a soft-ish landing, higher costs will lead to fewer closings, but that doesn't mean homebuying will stop entirely in 2023. Americans who are determined to make a move will find that staying up-to-date on the market, flexibility, creativity and a healthy dose of patience will go a long way toward success in the year ahead."

Key 2023 housing trends:

- A second wind in the second half. Although home sales are expected to slow overall in 2023, Realtor.com's forecast points to the possibility of a second wind in buying activity in the second half of the year. With mortgage rate hikes projected to continue through March, the Spring season will likely be less busy than in a typical year as buyers and sellers recalibrate their expectations around smaller budgets. This break could provide space for demand to renew as mortgage rates dip later in the year, when home shoppers will also have more options and bargaining power.

- A trifecta of budget barriers awat against buyers. In 2023, incomes are expected to grow (+3.9%), but not enough to offset higher mortgage rates (7.4%) and home prices (+5.4%), creating a trifecta of budget barriers. The typical monthly mortgage payment will be $2,430, 28% higher than in 2022, which will likely price many home shoppers out of the market. This will especially be a concern for first-time buyers. As rents will likely reach new highs, it will leave less room for saving towards a down payment. At the same time, some home shoppers may consider exploring new financial options like adjustable rate mortgages (ARMs), a trend that has already begun to take shape in 2022.

- It isn't 2008. During the mid-2000s housing boom, home sales were elevated for more than five years, and it took another five years for home sales to recover from the economic aftermath. Comparatively, mortgage rate hikes have brought a quicker but less dramatic end to the recent frenzy, during which buyers have been better qualified than in '08. Moving forward, home price growth will slow and may even decline periodically as prices largely stabilize over the next two-to-three years. The homeownership rate is predicted to hold in 2023.

- Some homeowners could still make money.SIn 2023, the typical homeowner is projected to gain $25,650 in equity as prices keep rising. With real estate wealth already much higher than pre-COVID, these trends offer a positive reality check for sellers who have been increasingly pessimistic about entering the market as listing prices have pulled back from last year's peak. While bidding wars won't be the norm in 2023, sellers who have owned their home for a longer period of time are still likely to make a profit. And those living in relatively affordable areas may still command offers above asking, driven by continued homebuyer interest in relocating to lower-priced markets.

- 2023 will be a wildcard. Political and economic events can always shake up the housing outlook, as was the case with major financial shifts in 2022. Along with factors including supply chain disruptions and the conflict in Ukraine, markets have largely begun to adjust for these changes, such as with the Fed's efforts to combat inflation with rate hikes. As such, forecasted 2023 housing trends don't anticipate a major shakeup like a recession, but it's still a possibility. Buyers and sellers should keep an eye out for risk signs like a substantial weakening in the jobs market, beyond the mild uptick in unemployment that is projected, as businesses are potentially disrupted by shifting geopolitical, financial and economic conditions. Although a potential recession may lead to lower mortgage rates, ultimately buyers' purchasing power would suffer. And for sellers, this would likely mean less demand and potential price drops.

Growth softens, but prices continue to advance

The major question on the minds of homeowners and aspiring buyers alike is what will happen to home prices. In the second quarter, the value of owner-occupied household real estate was a record-high $41.2 trillion or an average $489,185 for each of the 84.2 million households who own their primary homes. Put another way, every 1% change in the price of homes is a swing of more than $400 billion dollars. Record-high real estate wealth is in large part due to the more than decade-long increase in the price of homes which are expected to notch double-digit gains for a second year in 2022. Soaring prices were propelled by all-time low mortgage rates which are a thing of the past. As a result, home price growth is expected to continue slowing, dipping below its pre-pandemic average to 5.4% for 2023, as a whole. As higher mortgage rates cut into homebuyer purchasing power, the monthly cost of financing the typical for-sale home will average more than $2,430 in 2023. This would be a nearly 28% increase over the mortgage payment in 2022, and roughly double the typical payment for buyers in 2021.

Fore-sale inventory expected to increase:

In October 2022, the total inventory of homes for sale increased by 0.5% compared to the previous year. Excluding listings that were in various stages of the selling process but not yet sold (pending listings), however, the inventory of active listings had grown by 33.5% compared to the previous year, as homes spent almost one week longer on the market than the same time in 2021. As mortgage rates are expected to remain elevated through to the end of 2022 and into 2023, we expect slower market conditions to persist and we expect inventory levels to continue to grow gradually as the turnover of homes slows. Our forecast predicts total inventory to grow by 4.0% in 2022 overall, and by 22.8% in 2023. Given the roller-coaster ride inventory has been on lately, it’s important to keep historical context in mind. The level of inventory in 2023 is expected to fall roughly 15% short of the 2019 average.

"Of the many factors that are expected to affect the housing market in 2023, affordability tops the list of issues most likely to make or break buyers' plans. Still, our forecast does offer promise for home shoppers who are well-prepared. Tools like Realtor.com's Buying Power can help you understand how various rate changes and options impact your budget, and seamlessly integrate into the home search experience to help you stay on track financially," said Hale.

To read the full report, including more data, charts, and methodology, click here.