Although interest rates have been at historical lows, they are significantly up from 2012 lows. Not only has this caused many eligible refinancers to shy away from the market, but originators' profits are also suffering.

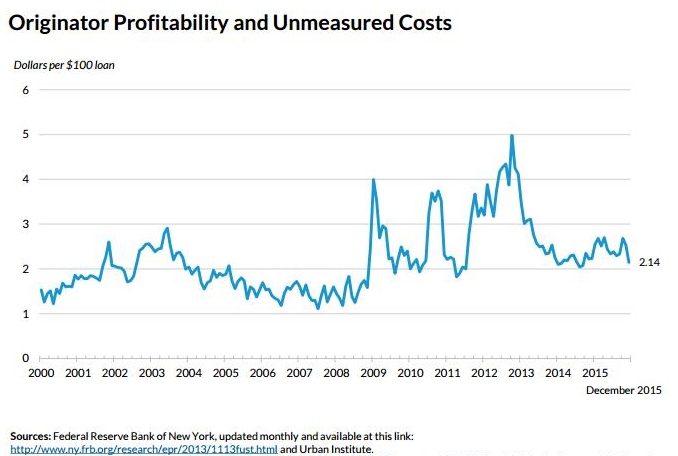

A report from Urban Institute found that originator profitability, which is a calculation from the Federal Reserve Bank of New York of the price at which the originator actually sells the mortgage into the secondary market and adds the value of retained servicing as well as points paid by the borrower, stood at 2.14 in December 2015. This number was in the narrow range of 2.04 to 2.70 since 2014.

A report from Urban Institute found that originator profitability, which is a calculation from the Federal Reserve Bank of New York of the price at which the originator actually sells the mortgage into the secondary market and adds the value of retained servicing as well as points paid by the borrower, stood at 2.14 in December 2015. This number was in the narrow range of 2.04 to 2.70 since 2014.

"As interest rates have risen from the lows in 2012, and fewer borrowers find it economical to refinance, originator profitability is lower," Urban Institute said.

The report continued, "When originator profitability is high, mortgage rates tend to be less responsive to the general level of interest rates, as originators are capacity-constrained. When originator profitability is low, mortgage rates are far more responsive to the general level of interest rates."

Urban Institute also reported that first lien originations in first three quarters of 2015 totaled approximately $1,350 billion.

Portfolio originations made up 31 percent of this total, the data showed. Meanwhile, the GSE share fell 1 percentage point year-over-year point to 46 percent, showing the decrease in FHA market share due to the FHA premium cut. FHA and VA and private label originations account for 23 percent and 0.8 percent, respectively.

Of all new originations, adjustable-rate mortgages (ARMs) accounted for only 5.1 percent of total originations in October 2015. AD popular refinance product, the 15-year fixed-rate mortgages (FRMs), comprised 16.1 percent of new originations.

Urban Institute said that both the GSEs and the Mortgage Bankers Association have predicted a decrease in mortgage originations for 2016, mostly because interest rates could increase.

Mortgage originations are expected to decrease by 30 percent in 2014, due to a decline in refinance activity, according to estimates from CoreLogic in September.

CoreLogic predicts that the number of mortgage originations fell by 30 percent from 2013 to 2014, while the mortgage origination dollar volume decreased by 27 percent.

On average, the CoreLogic estimate of mortgage origination volume is 1 percent below the Home Mortgage Disclosure Act (HMDA) estimate. Thus, the $1.28 trillion in mortgage origination dollar volume that CoreLogic forecast for the HMDA report is a minimum level. Most analysts estimate that lenders reporting under HMDA cover about 95 percent of the mortgage market, so CoreLogic estimates that total market originations accounting for under coverage is closer to $1.36 trillion.

Click here to view the full report.