Millennials make up the largest share of homebuyers in the U.S., according to a new report from LendingTree, surpassing older — and richer — generations. In fact, new data shows millennials have dominated the housing market for the past decade.

To highlight where millennials are looking to buy, LendingTree analyzed mortgage offers for users of the LendingTree platform across the nation’s 50 largest metros from Jan. 1 through Dec. 31, 2022.

Key findings:

- Across the nation’s 50 largest metros, an average of 52.88% of mortgage offers went to millennials. Millennials make up the majority of buyers in 37 of the nation’s 50 largest metros. Even in the metros where a majority of purchase requests don’t come from millennials, the generation still makes up the largest group of buyers.

- Millennials make up the largest share of potential homebuyers in San Jose, Calif., Denver, and Boston. In San Jose, 63.57% of mortgages were offered to millennials. In Denver and Boston, the figures were 61.35% and 60.59%, respectively.

- Millennials in Las Vegas, Birmingham, Ala., and Phoenix make up the lowest share of potential buyers — though still substantial. Across these metros, an average of 44.66% of mortgages were offered to millennials.

- Among millennials, potential homebuyers are oldest in San Francisco, New Orleans, and Miami. The average age among potential homebuyers in these three metros was 33.31 years old, more than a year older than the average of 32.16 in the metros with the youngest potential millennial homebuyers — Birmingham, Ala., Salt Lake City, and Denver.

- Potential millennial homebuyers have the highest average credit scores in San Jose, San Francisco, and Boston. The average credit score for these three metros was 748. By comparison, the average credit score for millennial homebuyers in the metros where millennials had the lowest credit scores — Memphis, Tenn., Birmingham and Las Vegas — was 713.

- Expensive California metros San Jose, San Francisco and Los Angeles were the areas that required millennials to put down the largest down payments on their homes. The average down payment across these three areas was $129,965. For comparison, that figure was more than three times higher than the average down payment of $39,209 across St. Louis, Virginia Beach, Va., and Oklahoma City — the metros where down payments were the smallest.

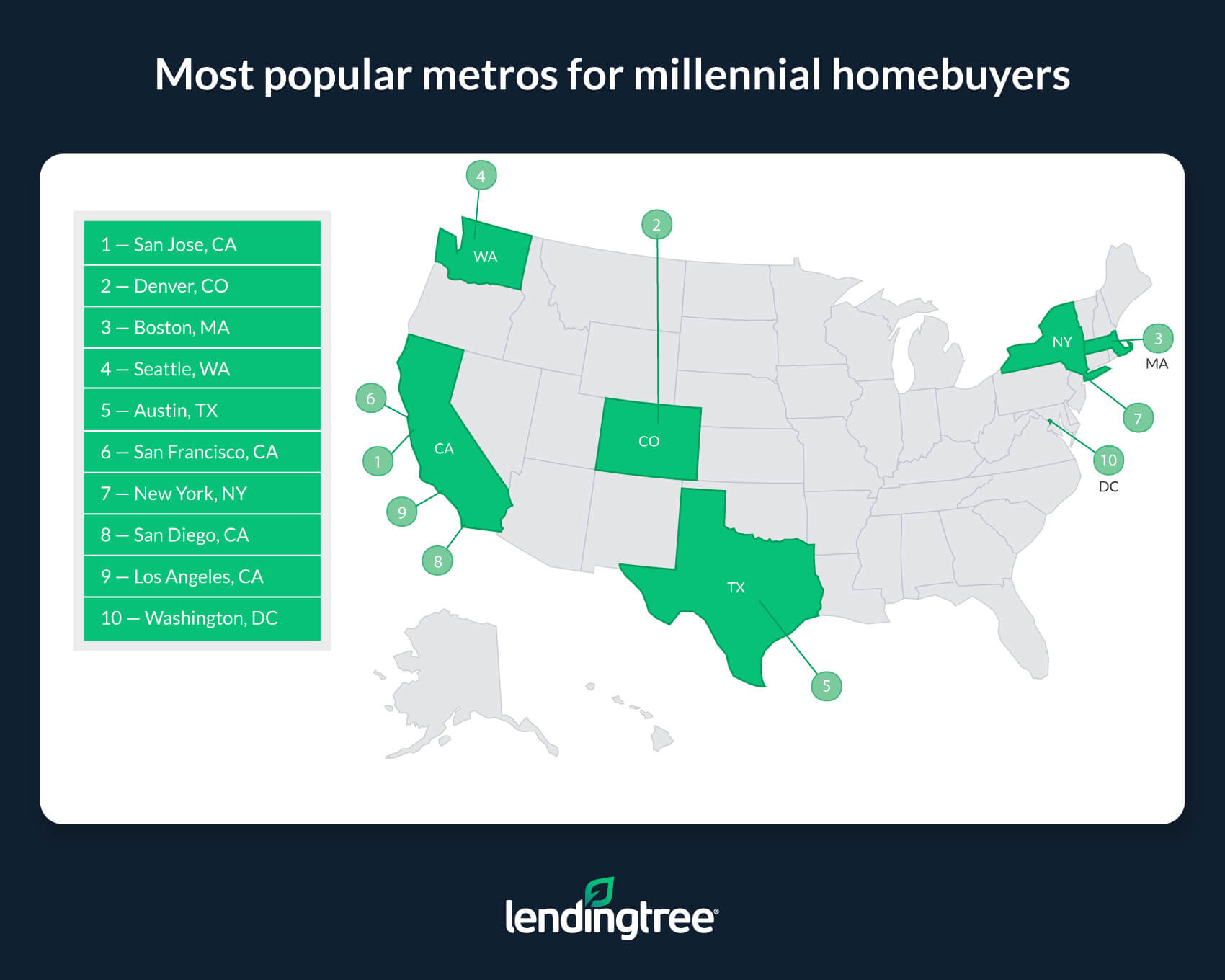

Most popular metros for millennial homebuyers

No. 1: San Jose, Calif.

- Share of mortgages offered to millennials: 63.57%

- Average millennial age: 33.01

- Average credit score among millennials: 751

- Average down payment amount among millennials: $144,942

No. 2: Denver

- Share of mortgages offered to millennials: 61.35%

- Average millennial age: 32.23

- Average credit score among millennials: 735

- Average down payment amount among millennials: $74,477

No. 3: Boston

- Share of mortgages offered to millennials: 60.59%

- Average millennial age: 32.38

- Average credit score among millennials: 741

- Average down payment amount among millennials: $84,259

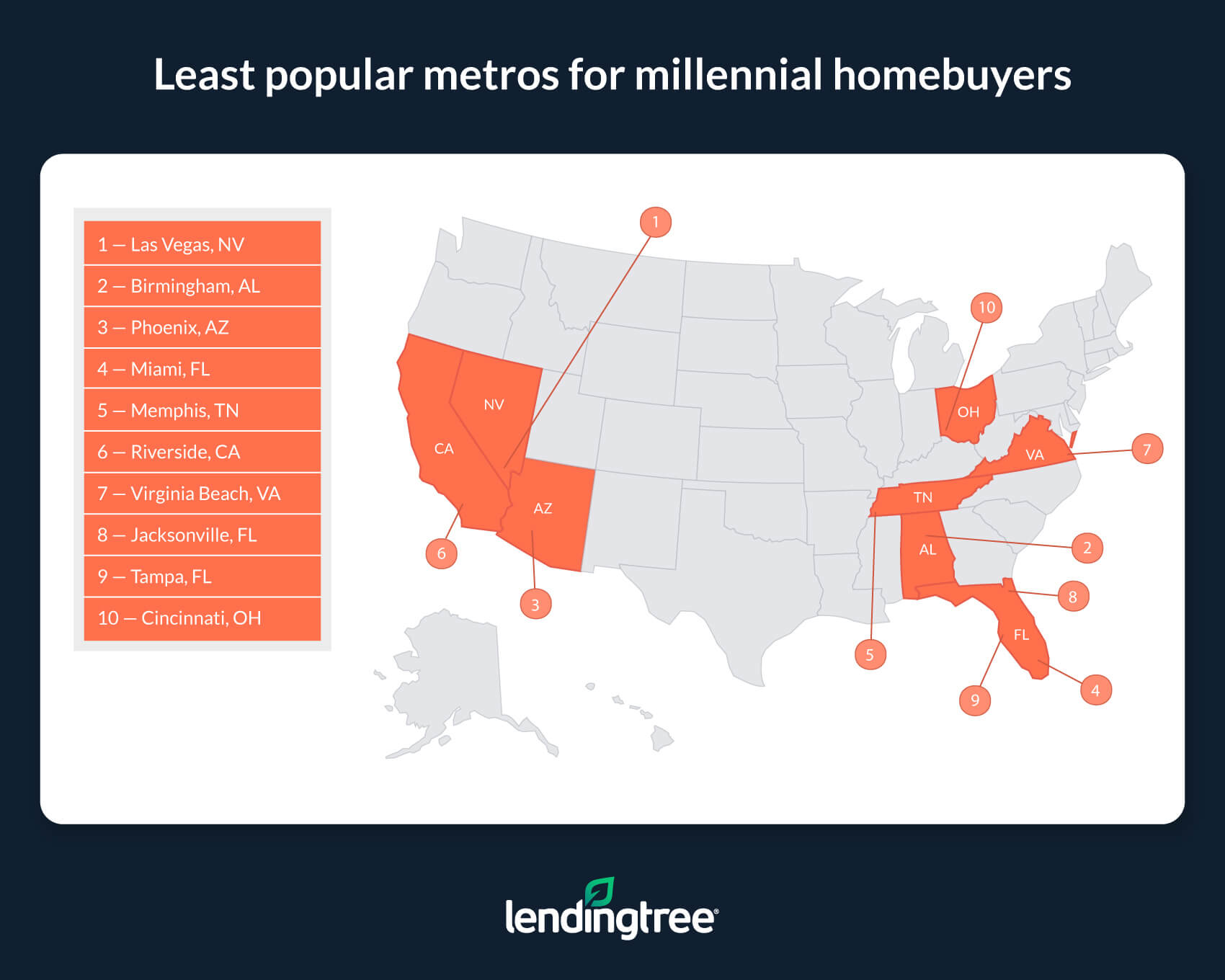

Least popular metros for millennial homebuyers

No. 1: Las Vegas

- Share of mortgages offered to millennials: 41.92%

- Average millennial age: 32.89

- Average credit score among millennials: 715

- Average down payment amount among millennials: $49,604

No. 2: Birmingham, Ala.

- Share of mortgages offered to millennials: 45.95%

- Average millennial age: 32.10

- Average millennial credit score among millennials: 713

- Average down payment amount among millennials: $46,998

No. 3: Phoenix

- Share of mortgages offered to millennials: 46.11%

- Average millennial age: 32.52

- Average credit score among millennials: 718

- Average down payment amount among millennials: $65,395

Why millennials dominate the housing market

For example, many millennials are at an age where they’re starting families and earning more money. This means they not only have more of a financial ability to become homeowners, but they’re incentivized by reasons like needing to provide for their loved ones in a way they may not have been when more of them were in their 20s.

In that same vein, while buying a new home might make more sense when you’re younger and starting a family or becoming established in your career, it often starts to make less sense as you age — especially if you’re planning to finance your purchase with a loan. After all, it’s one thing to take out a six-figure mortgage in your 30s when you likely have plenty of time to work and pay it off, but it’s another thing to take out a mortgage when your retirement is fast approaching.

Put simply, though millennials are certainly not as financially well-off as older generations, they’re at a place where buying often makes the most sense. And as millennials age, younger generations will likely supplant them as the largest share of homebuyers on the market — even if those younger generations might also have to deal with increased financial hardships related to buying.

To read the full report, including more data, charts, homebuyer tips and methodology, click here.