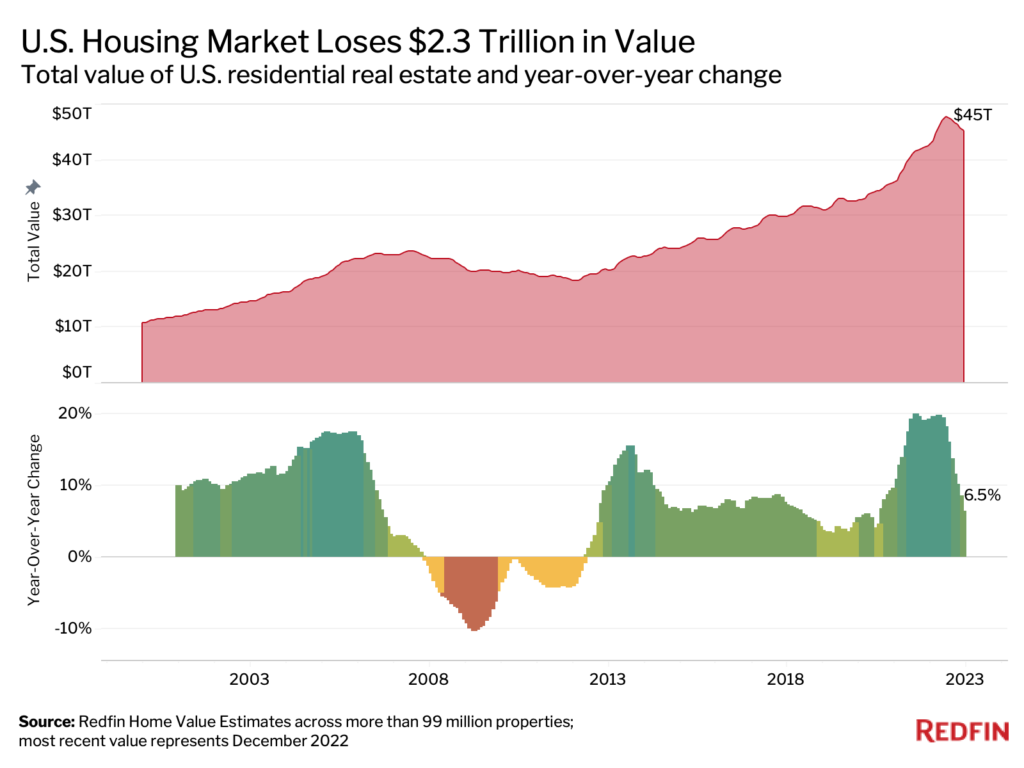

The total value of U.S. homes was $45.3 trillion at the end of 2022, down 4.9% ($2.3 trillion) from a record high of $47.7 trillion in June, according to a new report from Redfin. That’s the largest June-to-December drop in percentage terms since 2008.

While the total value of U.S. homes was up 6.5% from a year earlier in December, that’s the smallest year-over-year increase during any month since August 2020. This is according to an analysis of Redfin Estimates on more than 99 million U.S. residential properties.

Key Findings:

- The Bay Area housing market has lost more value in percentage terms than anywhere else in the country amid sluggish demand. Florida continues to see large gains.

- Home values are holding up better in the suburbs than in cities, which have seen an exodus of residents due to remote work.

- Millennials, who are now in their prime homebuying years, have experienced larger value gains than other generations.

- Asian homeowners have been disproportionately affected by home-value declines.

- Values in areas with high flood and/or heat risk have held up better than values in areas with low risk, indicating that climate dangers aren’t priced in.

The housing market has been shedding value because homebuyer demand has waned, which has also caused home prices to fall from their peak. The median U.S. home sale price was $383,249 in January, down 11.5% from a peak of $433,133 in May, and up just 1.5% from January 2022.

Homebuyer demand slowed in large part because rising mortgage rates—a consequence of the Federal Reserve’s effort to curb inflation—made purchasing a home more expensive. The average 30-year fixed mortgage rate was 6.36% in December. While that’s down from the 20-year high of 7.08% in November, it’s roughly double the level from the start of 2022. Rates fell at the beginning of February, giving buyers some hope, but have since crept back up to December levels.

“The housing market has shed some of its value, but most homeowners will still reap big rewards from the pandemic housing boom,” said Redfin Economics Research Lead Chen Zhao. “The total value of U.S. homes remains roughly $13 trillion higher than it was in February 2020, the month before the coronavirus was declared a pandemic. Unfortunately, a lot of people were left behind. Many Americans couldn’t afford to buy homes even when mortgage rates hit rock bottom in 2021, which means they missed out on a significant wealth building opportunity.”

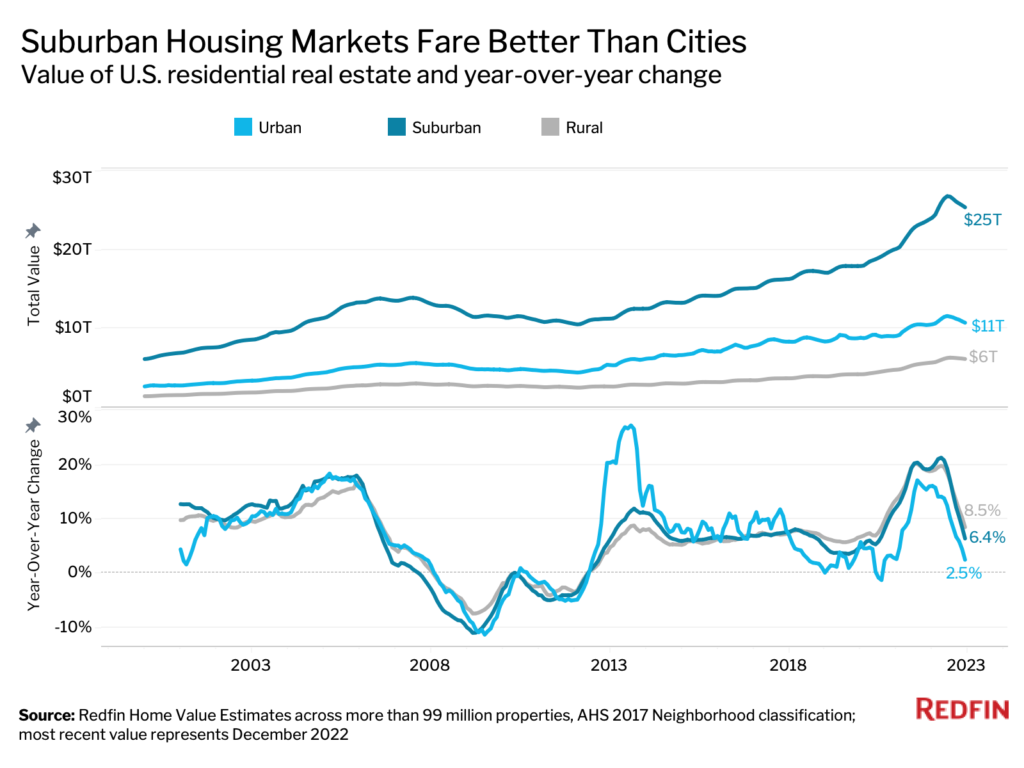

Suburbs Faring Better Than Cities

The total value of homes in American suburbs rose 6.4% year over year to $25.4 trillion in December. By comparison, the value of urban homes climbed 2.5% to $10.8 trillion. Rural homes—which make up a relatively small portion of the housing market—also fared better than cities, with total home value increasing 8.5% to $6.2 trillion.

The suburbs came back into vogue during the pandemic while cities fell out of favor—largely due to the shift to remote work and the housing affordability crisis.

The Bay Area’s Housing Market Has Taken the Biggest Hit

The total value of San Francisco homes fell 6.7% year over year to $517.5 billion in December (a $37.3 billion decline)—a larger drop in percentage terms than any other major U.S. metropolitan area. Next came two other Bay Area markets: Oakland (-4.5%) and San Jose (-3.2%). Only three other metros saw year-over-year declines: New York (-1%), Seattle (-0.4%) and Boise, ID (-0.3%). This analysis includes the 100 most populous metro areas, with the exception of Albuquerque, NM, which had insufficient data.

Pricey coastal tech hubs have experienced outsized declines in home values for a few reasons:

- They are among the most expensive markets in the country, which means home values had more room to fall.

- They have seen an exodus of residents during the pandemic because people prioritized space and affordability over proximity to the workplace.

- They were hit hard by tech layoffs and are home to many residents with significant investments in the stock market, which just had its worst year since 2008.

The good news for Bay Area buyers is that home prices are down and competition remains far lower than it was during the pandemic homebuying boom. San Francisco’s median home sale price dropped 9.4% year over year to $1.3 million in January—the second biggest decline in the country. The good news for sellers is that the steep decline in prices has lured some buyers back.

“Three of my listings recently went under contract after sitting on the market for more than a month,” said Ali Mafi, a Redfin real estate agent in San Francisco. “They all had a few showings here and there in the fall, but no buyer wanted to pull the trigger. And then suddenly in the new year, we had 10 or 15 people touring each property.”

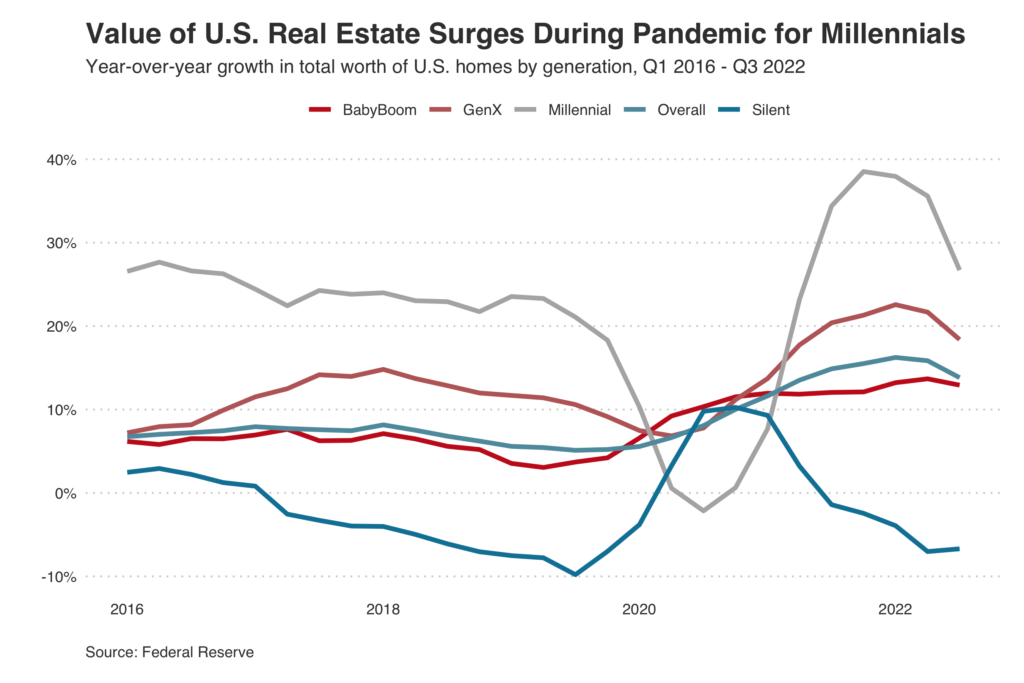

Millennials, in Prime Homebuying Age, Are Reaping Large Value Gains

The total value of U.S. homes owned by millennials rose 26.7% year over year to $5.6 trillion in the third quarter of 2022—the most recent period for which data is available. Generation X saw the second largest increase (+18.4% to $13.9 trillion), followed by Baby Boomers (+12.9% to $18.1 trillion). The Silent Generation experienced a decrease (-6.7% to $4.4 trillion), as many of its members have passed away or moved into retirement homes.

Millennials are gaining more value largely because they’re in prime homebuying age, which means they’re purchasing substantially more homes than they were in recent years.

To read the full report, including more data, charts and methodology, click here.