Mortgage rates have surpassed 5% lately, due in large part to increases to the federal interest rate by the Federal Reserve who in addition to raising the rate twice this year, is expected to have further increases for the foreseeable future. So, what does that mean for the average buyer? It means money is more expensive, and those costs add up quickly as rates continue to climb.

Mortgage rates have surpassed 5% lately, due in large part to increases to the federal interest rate by the Federal Reserve who in addition to raising the rate twice this year, is expected to have further increases for the foreseeable future. So, what does that mean for the average buyer? It means money is more expensive, and those costs add up quickly as rates continue to climb.

With that in mind, LendingTree conducted new research and did the math on the differences between a 30-year, fixed-rate mortgage in taken out in January and April in every state to pinpoint the exact cost a higher rate will cost you over the lifetime of the loan.

As a whole, LendingTree found rising rates are costing borrowers hundreds of dollars a month equating to up to $100,000 over the lifetime of the loan.

Data showed that in January 2022, the average APR across the country was 3.79%—this number rose to 5.25% nationally by April 2022.

To put that in simpler terms, rising APRs added an average of $258.57 to each month's payment. That is an extra $3,102.82 in extra interest payments per year equaling $93,084.60 in additional interest over the life of the loan.

But mortgage rates are not static and vary across the country. Mortgage payments increased the least in Ohio, West Virginia, and Kentucky where the average loan increased by $199.55, $200.81, and $202.28, respectively. This averages about $72,300 over the life of the loan.

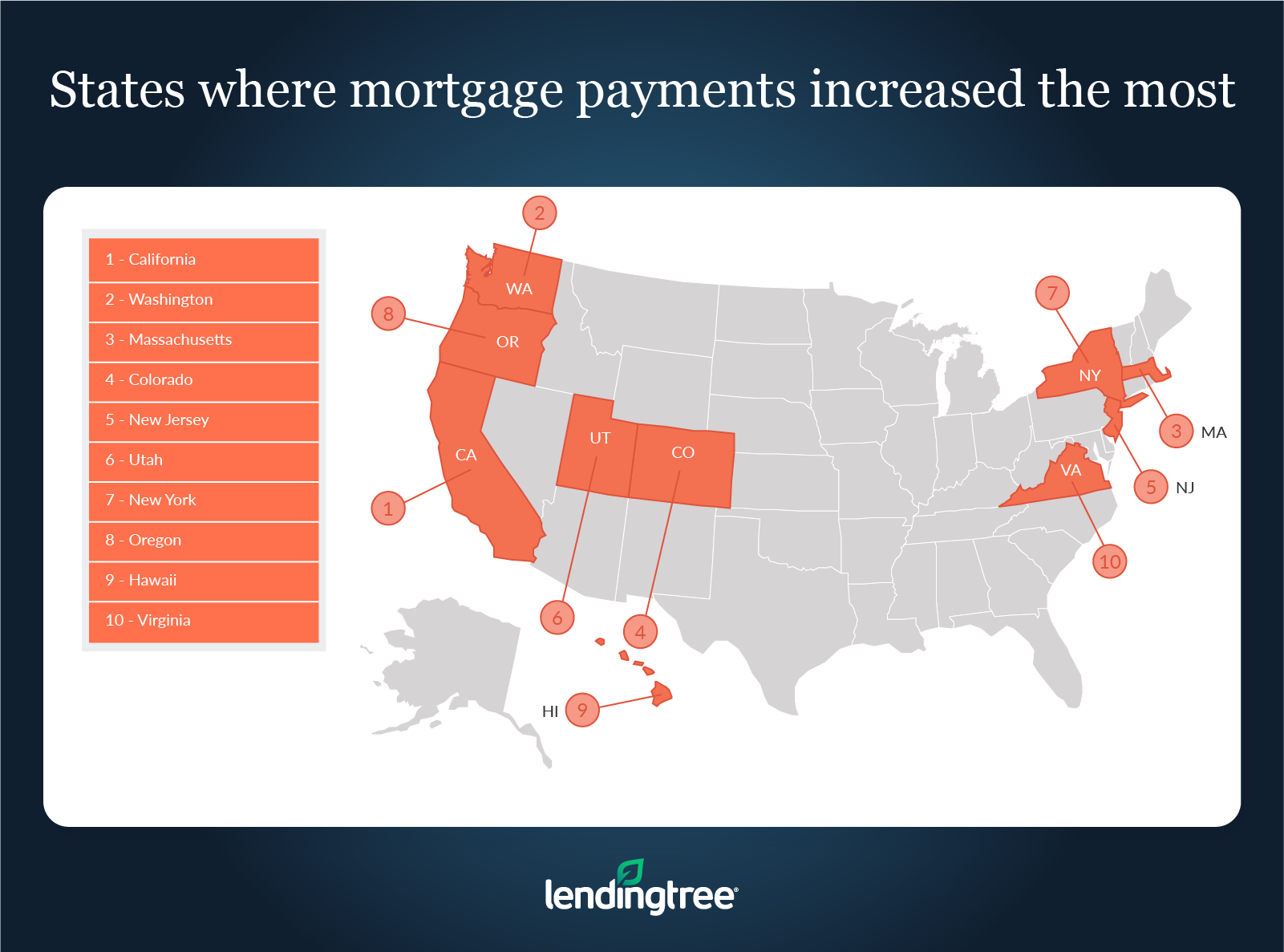

The states that saw the most dramatic increases were California, Washington, and Massachusetts. Mortgage payments increased in these states by $406.78, $357.38 and $337.23, respectively. This averages about $132,100 over the life of the loan.

LendingTree warns that potential borrowers should expect rates to continue to rise through 2023 due to the Federal Reserve’s comments on raising rates multiple times this year. This will put more pressure on mortgage rates causing them to rise.

While nothing is set in stone and rates are not guaranteed to rise, higher rates are not always bad news. Raising rates should demand less demand from homebuyers—and according to LendingTree—may possibly reduce bidding wars and free up inventory.

Data for this report was gleaned through 570,000 users who received an offer for a 30-year, fixed-rate mortgage from LendingTree between Jan 1 and April 22, 2022. The full report can be found here.