U.S. home prices are high and are still rising, but the price picture looks a bit different when consumer buying power is brought into the equation.

U.S. home prices are high and are still rising, but the price picture looks a bit different when consumer buying power is brought into the equation.

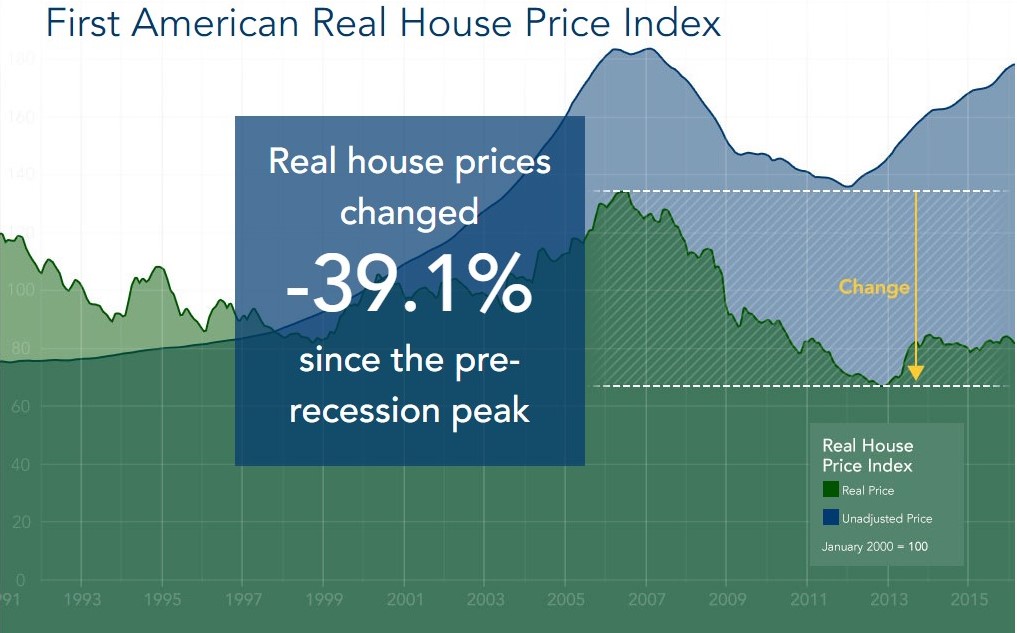

First American Financial Corporation's inaugural Real House Price Index (RHPI), provides a new take on the way the industry view home prices.

The index measures the price changes of single-family properties throughout the U.S. adjusted for the impact of income and interest rate changes on consumer house-buying power over time and across the U.S. at national, state, and metropolitan area levels. In addition, the index also measures of housing affordability.

"House prices are typically reported nominally," the report said. "In other words, without adjusting for any inflation. Just like other goods and services, the price of a house today is not directly comparable to the price of that same house 30 years ago because of the long-run influence of inflation in the economy."

"Simply looking at house price changes without considering the changes in consumer house-buying power misrepresents the real change in prices." -First American Chief Economist Mark Fleming.

The report said that real house prices are significantly lower than they were prior to the housing boom. After adjusting for increased consumer house-buying power, real house prices are 39.1 percent under their housing-boom peak in July 2006 and 18 percent below the level of prices in January 2000.

The report found that unadjusted house prices are expected to increase by 5.1 percent in March on a year-over-year basis, but real house prices increased by 2.1 percent over the same period. The unadjusted national price level is less than 2.9 percent away from the housing-boom peak in 2007.

The report found that unadjusted house prices are expected to increase by 5.1 percent in March on a year-over-year basis, but real house prices increased by 2.1 percent over the same period. The unadjusted national price level is less than 2.9 percent away from the housing-boom peak in 2007.

According to First American, the RHPI was unchanged in March and increased 2.1 percent year-over-year. "Low rates have fueled increases in consumer house-buying power, keeping real house prices low by historic standards," Fleming noted.

“Many potential homebuyers this spring may experience sticker shock when house hunting, as unadjusted prices are consistently outpacing income growth,” said Fleming. “Yet, the real price level is much lower than even in the years before the housing boom, largely because consumer house-buying power is significantly higher today due to the current environment of historically low mortgage rates.”

First American's 5 states with the highest year-over-year increase in the RHPI are:

- North Dakota (+16.0 percent)

- Wyoming (+14.7 percent)

- Rhode Island (+12.2 percent)

- Delaware (+6.0 percent)

- Missouri (+5.6 percent).

First American's 5 states with the highest year-over-year decrease in the RHPI are:

- District of Columbia (-5.5 percent)

- Alaska (-5.2 percent)

- Maryland (-5.0 percent)

- Pennsylvania (-4.4 percent)

- West Virginia (-4.2 percent)

First American questioned if the rapid pace of home price appreciation impacted affordability for consumers. Although recent home price and household income data shows that affordability has declined, First American determined that a consumer's ability to afford a house is not just a function of their income.

"Location matters in real estate, but incomes and interest rates matter more when considering house price changes. Simply looking at house price changes without considering the changes in consumer house-buying power misrepresents the real change in prices," Fleming stated. "Taking the real, consumer house-buying power adjusted perspective on measuring house prices yields a very different perspective on affordability."