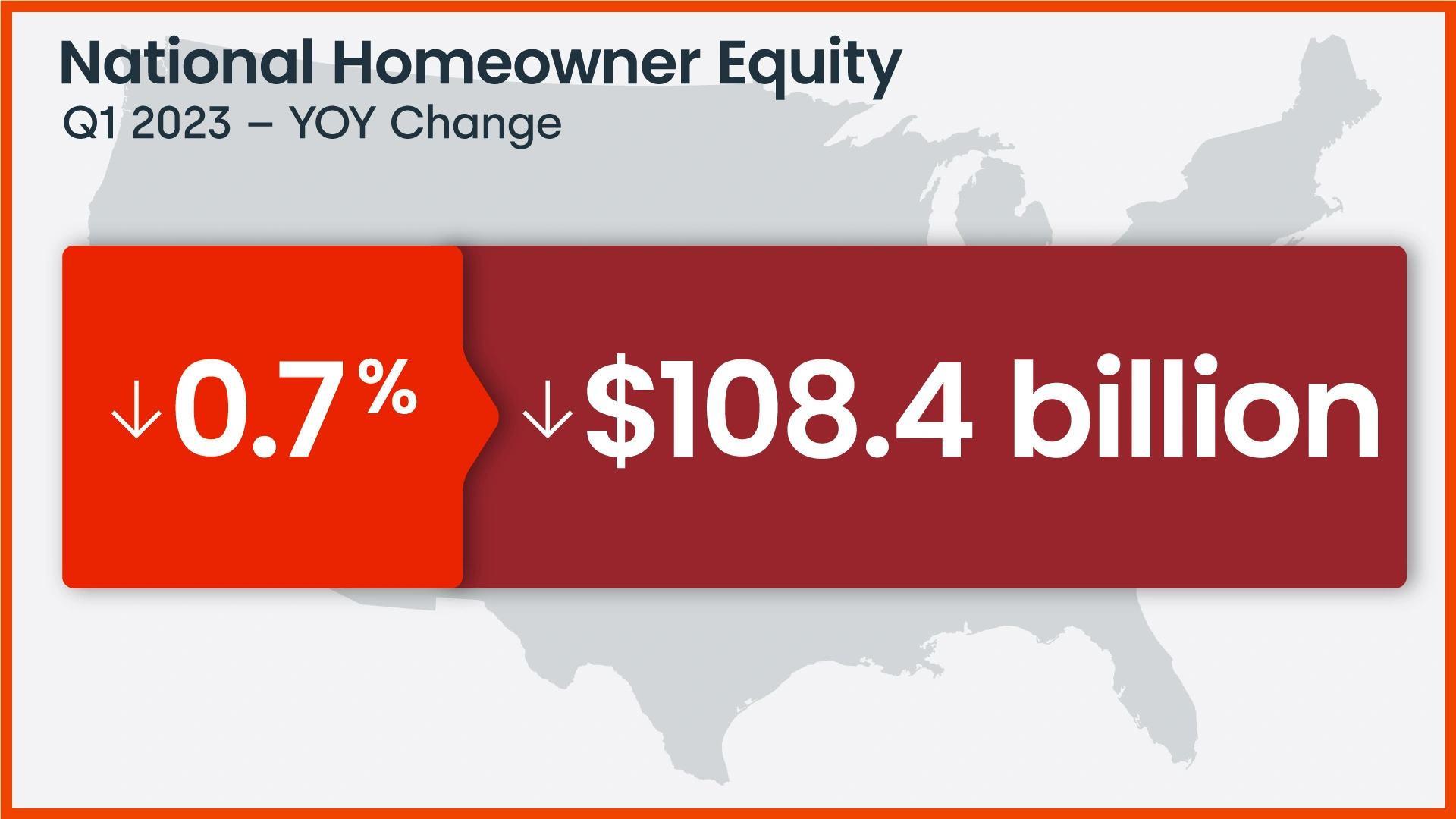

CoreLogic [1] reported some unfortunate news for homeowners in their Homeowner Equity Report [2] (HER) covering the first quarter of 2023 showed that U.S. homeowners with a mortgage (about 63% of all properties) saw their home equity decrease by 0.7% year-over-year.

CoreLogic [1] reported some unfortunate news for homeowners in their Homeowner Equity Report [2] (HER) covering the first quarter of 2023 showed that U.S. homeowners with a mortgage (about 63% of all properties) saw their home equity decrease by 0.7% year-over-year.

This number represents a collective loss of $108.4 billion or an average loss of $5,400 per borrower since the first quarter of 2022.

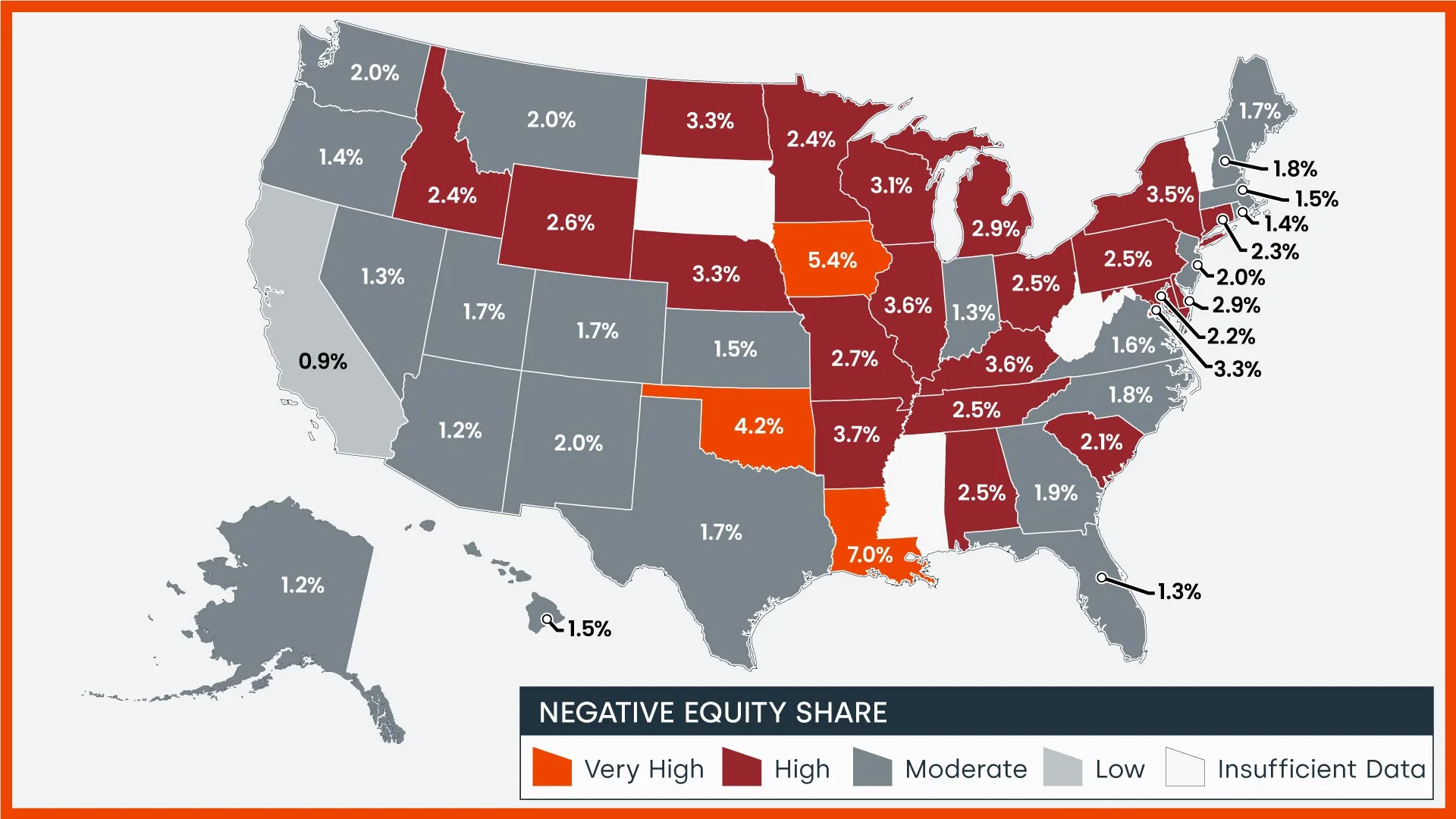

According to CoreLogic in the first quarter of 2023, mortgaged homeowners lost a small amount of equity for the first time since the beginning of 2012, while national combined equity followed behind. Aligning itself with numbers from the fourth quarter of 2022, Western states posted the largest annual home equity losses: Washington (-$74,300), California (-$59,600) and Utah (-$37,700). The equity losses in those states reflect decelerating home prices, with all three posting annual declines in February and March, according to CoreLogic’s Home Price Index.

While home equity did decline on average, it remains solid, with the number of properties underwater remaining unchanged since the previous quarter.

“Home equity trends closely follow home price changes,” said CoreLogic Chief Economist Selma Hepp [3]. “As a result, while the average amount of equity declined from a year ago, it increased from the fourth quarter of 2022, as monthly home prices growth accelerated in early 2023.”

“The average U.S. homeowner now has more than $274,000 in equity—up significantly from $182,000 before the pandemic,” Hepp continued. “Also, while homeowners in some areas of the country who bought a property last spring have no equity as a result of price losses, forecasted home price appreciation over the next year should help many borrowers regain some of that lost equity.”

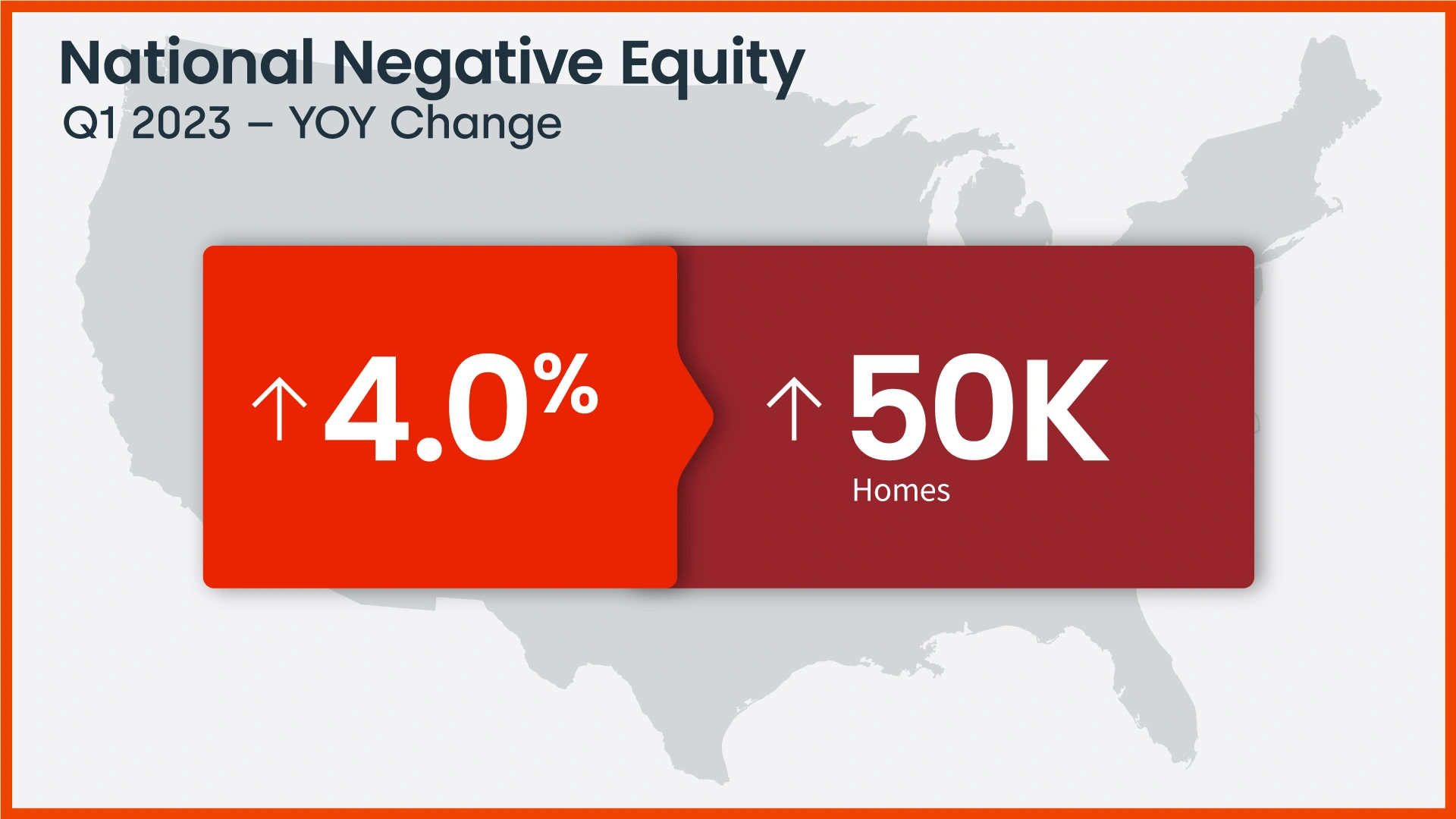

As of the first quarter of 2023, the quarterly and annual changes in negative equity were:

- Quarterly change: From the fourth quarter of 2022 to the first quarter of 2023, the total number of mortgaged homes in negative equity was unchanged, remaining at 1.2 million homes or 2.1% of all mortgaged properties.

- Annual change: From the first quarter of 2022 to the first quarter of 2023, the total number of homes in negative equity increased by 4% from 1.1 million homes or 2% of all mortgaged properties.

Because home equity is affected by home price changes, borrowers with equity positions near (+/- 5%), the negative equity cutoff, are most likely to move out of or into negative equity as prices change, respectively. Looking at the first quarter of 2023 book of mortgages, if home prices increase by 5%, 145,000 homes would regain equity; if home prices decline by 5%, 213,000 properties would fall underwater.

Click here [4] to view the report in its entirety.