Competition among homebuyers over shrinking supply has made this home shopping season unusually hot, according to Zillow's May 2023 Market Report [1]. Meanwhile, high mortgage rates are continuing to deter homeowners from listing their homes, pushing inventory down to record lows.

Key Findings:

- Monthly home value growth of 1.4% is the highest recorded since June 2022.

- Homebuyers are motivated despite few options and rising mortgage rates—sales rose nearly 10% from April to May.

- Inventory reached a record low for May as high mortgage rates deter home sellers.

Typical U.S. home values grew by 1.4% from April to May, the strongest monthly appreciation since last June. That's cooler than the previous two springs, but remains hotter than in 2018 or 2019. The typical home value is $346,856—up 0.9% over last May and up 3.4% from a recent low in January.

A new loan on a home priced at the typical value in the U.S. would feature monthly mortgage payments just shy of $1,800. That monthly payment is 22% higher than last year, double that of May 2019, and the second highest on record after October 2022.

"Many homeowners are still opting not to sell and give up historically low mortgage rates. But those who do have been rewarded with bidding wars as buyers compete for limited options," said Zillow senior economist Jeff Tucker. "Spring is traditionally the hottest time of year in the housing market, and 2023 has been no exception. Time will tell if seasonal price slowdowns arrive on time this year, later in summer."

Regional appreciation trends

Home values are now down from year-ago levels in just over half (27) of the 50 largest metro areas, most significantly in Austin (-11.2%), San Francisco (-9.3%), San Jose (-8.4%), Phoenix (-7.0%), and Las Vegas (-6.9%). Meanwhile, annual price gains are highest in Richmond (5.8%), Miami (5.4%), Oklahoma City (4.9%), Kansas City (4.1%), and Cincinnati (4.0%).

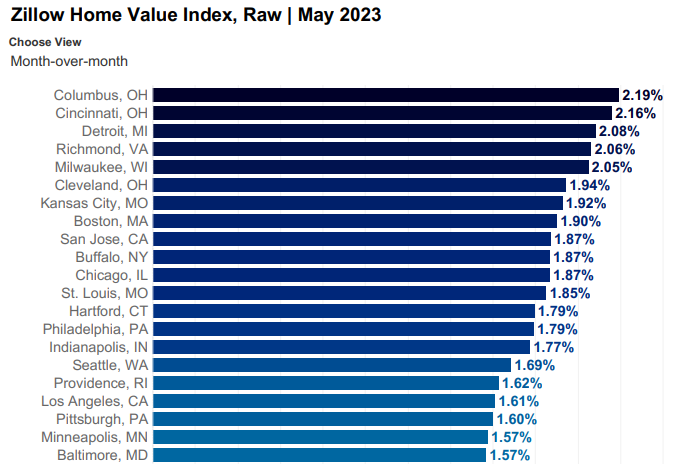

Affordability is still the key driver of demand, and that's reflected in the markets that are appreciating fastest. The largest monthly home value gains are in the Midwest—home to six of the seven metros with the biggest gains in May. Columbus, Ohio, led the way (2.2% monthly gain), followed closely by Cincinnati, Detroit, Richmond, VA, and Milwaukee.

Price growth also jumped back in West Coast tech hubs after prices fell significantly there late in 2022. Home values rose faster than the national average for the second straight month in San Jose (1.9%), Seattle (1.7%), and San Francisco (1.4%).

Inventory shortage drags on, driven by high rates

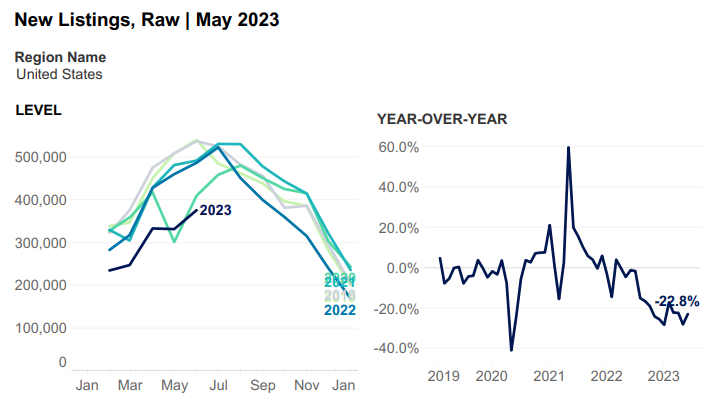

A shortage of new listings has affected the housing market for almost a year. The flow of new listings was down 23% year-over-year in May—a more moderate drop than in April but nearly equal to that of March.

The primary driver is still higher mortgage rates, which make a new loan unattractive when the majority of mortgaged homes are financed for less than 4%. Even without intentions to buy again, anyone with a mortgage at a rate under 4% might be loath to sell when there's a possibility to rent out the home for more than their carrying costs.

The lack of new listings, paired with resolute demand from homebuyers, has driven prices up and total inventory down to record lows for this time of year. The number of homes for sale on Zillow in May was 3.1% lower than last year and a massive 46% below that of May 2019.

Homebuyers are still motivated, despite costly market conditions

Sales measured by newly pending listings climbed 9.5% from April, shrinking the year-over-year decline to 18% in May and marking steady improvement since March. While this looks low in comparison to the hot pandemic era, sales figures are close to pre-pandemic standards.

Pending sales peaked in May in 2018, 2019 and 2022; the weeks ahead will reveal if that seasonal pattern repeats itself, or if the buying season stretches into summer, as it did in 2020 and 2021.

To read the full report, including more data, charts, and methodology, click here [1].