HouseCanary, Inc. [1] has released its latest Market Pulse report, [2] showing that amidst a looming mild recession and increasing rates from the Federal Reserve [3], the housing market continues to grapple with challenges, including a year-over-year decline in inventory and a rise in removals.

Additionally, although price cuts have been observed, they remain well below the peak levels witnessed in September and October of 2022.

However, both listed and closed prices experienced positive year-over-year growth in June. While list prices appear to have reached their peak during that month, closed prices continue to climb at a rapid pace. Heading into Q3 2023, it can be expected that market activity remains at relatively low levels, with the Federal Reserve continuing to increase rates at a slow pace.

Key Takeaways:

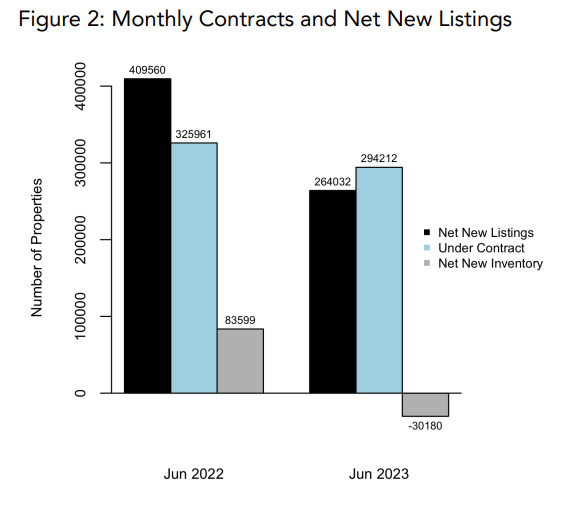

- For the month of June 2023, 264,032 net new listings were placed on the market, and 294,212 properties went under contract. This represents a decrease of 35.5% and 9.7%, respectively, versus June 2022.

- The decrease in net new listings was driven by a 31.1% decrease in new listing volume as well as a 1.4% increase in removals compared to June 2022.

- Median days on market stood at 34, up 9.7% from the prior year at 31 days on market.

- The sale-to-list-price ratio stands at 99.5%, which is well above the lowest value observed in January 2023 and trending further upward.

- Price cuts are down 18.6% year-over-year, and are down nearly 45% from their recent peaks occurring in September and October 2022.

- Total single-family rental inventory is up 73.7% from the same period in 2022, and up 176.8% from 2021.

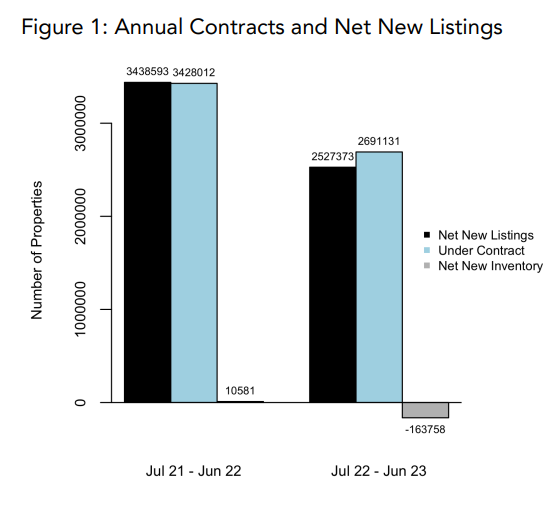

Contract Volume and Net New Listing Volume:

Over the last 52 weeks, 2,527,373 net new listings were placed on the market, and 2,691,131 properties went under contract. This represents a decrease of 26.5% and 21.5%, respectively.

For the month of June 2023, 264,032 net new listings were placed on the market, and 294,212 properties went under contract. This represents a decrease of 35.5% and 9.7%, respectively, versus June 2022. The decrease in net new listings was driven by a 31.1% decrease in new listing volume as well as a 1.4% increase in removals compared to June 2022.

“In the face of a challenging economic landscape with declining inventory and rising removals, the housing market has shown remarkable resilience, as evidenced by the upward trajectory of listed and closed prices," said Jeremy Sicklick, Co-Founder and CEO of HouseCanary. "Price cuts remain well below their peak levels from 2022, and it is promising to witness positive year-over-year growth in June. Looking ahead to the second half of the year and Q3, we anticipate continued subdued market activity and a slow pace of rate hikes by the Federal Reserve.”

The Market Pulse report covers 22 listing-derived metrics and comparing data between June 2022 and June 2023.

To read the full report, including more data, charts, and methodology, click here [4].