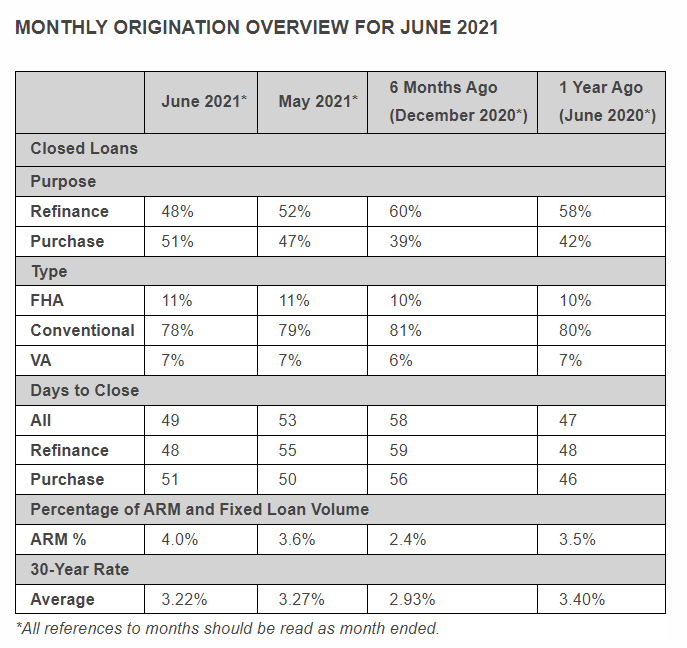

ICE Mortgage Technology’s latest Origination Insight Report (OIR) has found that, of the total number of closed mortgage loans in June 2021, new home purchases represented a higher percentage than refinances. This is the first time since December 2019 that home purchases eclipsed refinances in the OIR. According to the report, purchases rose to 51% of closed mortgage loans in June, up from 47% in the month prior. Conversely, refinances represented 48% of closed loans, down from 52% the month prior. The remaining 1% of closed loans were for other purposes.

ICE Mortgage Technology’s latest Origination Insight Report (OIR) has found that, of the total number of closed mortgage loans in June 2021, new home purchases represented a higher percentage than refinances. This is the first time since December 2019 that home purchases eclipsed refinances in the OIR. According to the report, purchases rose to 51% of closed mortgage loans in June, up from 47% in the month prior. Conversely, refinances represented 48% of closed loans, down from 52% the month prior. The remaining 1% of closed loans were for other purposes.

“While we are still seeing a strong refinance market, including the continued growth of cash-out refinances, the traditional summer purchase market is clearly evident in the data,” said Joe Tyrrell, President of ICE Mortgage Technology.

Rates have been below the 3% mark for the better part of six weeks now, with the latest Freddie Mac Primary Mortgage Market Survey (PMMS) finding the 30-year fixed-rate mortgage (FRM) averaging 2.77% for the week ending August 5, 2021.

Despite low rates, a low supply and high demand remains factors for prospective buyers as affordability issues linger. A recent National Association of Homebuilders (NAHB) report found that prospective borrowers might be discouraged by the state of today's market, which includes high prices, intense competition, and a shortage of available, affordable inventory, however, some 17% of Americans plan to purchase a home within the year. NAHB noted that the last, and only, other time the share of prospective buyers stood at 17% was in the first quarter of 2018, the researchers noted.

First American Financial Corporation’s latest Real House Price Index (RHPI), a measure of the price changes of single-family properties throughout the U.S. in May found that housing affordability continued to decline. The three key drivers of First American’s RHPI are incomes, mortgage rates, and an unadjusted house price index. Incomes and mortgage rates are used to inflate or deflate unadjusted house prices in order to better reflect consumers' purchasing power and capture the true cost of housing.

"Housing affordability declined on a year-over-year basis for the third month in a row in May, following a two-year streak of rising affordability,” said Mark Fleming, Chief Economist at First American.

ICE’s OIR also found that in June, the average time to close all loans decreased to 49 days, down from 53 days in May. The average time to close a refinance decreased to 48 days, down from 55 days the month prior. However, the average time to close a purchase was 51 days, up from 50 the month prior.

Closing rates for all loans decreased slightly, to 75.3% in June, down from 76.9% in May. Closing rates on refinances decreased to 74.6% in June, down from 77% in May. Closing rates on purchase loans dropped to 76.3% in June, a slight decrease from 77.0% in May.