Non-conventional forms of financing have been gaining traction in the single-family housing market, accounting for more than a third of the market in 2015, according to the most recent Census Bureau Survey of Construction data.

Non-conventional forms of financing have been gaining traction in the single-family housing market, accounting for more than a third of the market in 2015, according to the most recent Census Bureau Survey of Construction data.

In all, 34.5 percent of new single-family homes were purchased with non-conventional financing in 2015, up by half a percentage point from 2015 (34 percent), according to the National Association of Home Builders (NAHB).

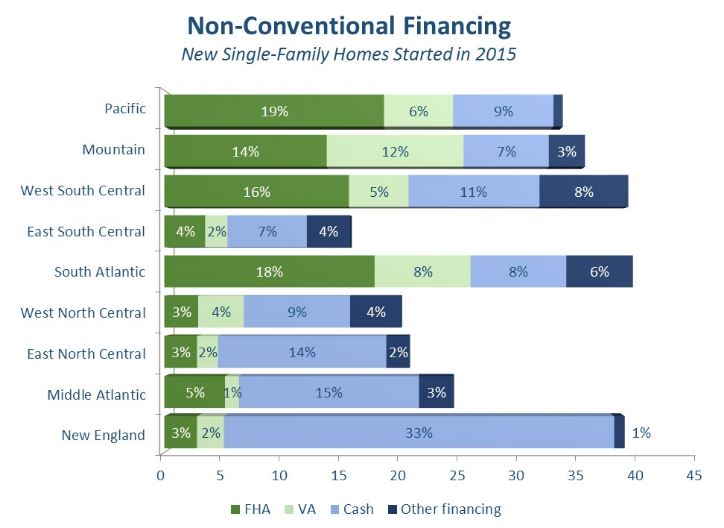

Non-conventional financing, which includes cash purchases, loans insured by the Federal Housing Administration (FHA), loans insured by the Department of Veterans Affairs (VA), the Rural Housing Service, Habitat for Humanity, loans from individuals, state or local government mortgage-backed bonds were most popular in the West South Central region of the U.S. (Texas, Oklahoma, Arkansas, Louisiana) and in the South Atlantic region (Florida, Georgia, the Carolinas, Virginia, West Virginia, Delaware), where they accounted for 40 percent of single-family home purchases in 2015. New England was right behind with 39 percent.

The East South Central region (Mississippi, Alabama, Tennessee, and Kentucky) was the least dependent region on non-conventional financing n the single-family housing market in 2015, with only 16 percent of the market—less than half the national average for the year.

According to the NAHB, while the West South Central and New England regions posted similar high shares of single-family homes purchased with non-conventional financing in 2015, the breakdowns in the types of non-conventional financing they used were different. In the South Atlantic and West South Central, VA and FHA-backed loans accounted for 26 percent and 21 percent of the market, respectively, while in New England, only 3 percent of the market was comprised of FHA-insured loans; the most popular form of non-conventional financing in New England in 2015 was cash, with more than a third of homes started in 2015.

Overall in 2015, the share of FHA-insured mortgages for homes started increased from 2014, according to NAHB. The Pacific and South Atlantic divisions has the highest share of FHA-insured mortgages for new single-family homes in 2015 with 19 percent and 18 percent, respectively.

Overall in 2015, the share of FHA-insured mortgages for homes started increased from 2014, according to NAHB. The Pacific and South Atlantic divisions has the highest share of FHA-insured mortgages for new single-family homes in 2015 with 19 percent and 18 percent, respectively.

“This was largely due to a reduction in FHA mortgage insurance premiums implemented at the start of 2015.,” wrote Natalia Siniavskaia, Ph.D., NAHB Assistant Vice President for Housing Policy Research. “As a result, FHA-backed loans regained their status as the most prevalent form of non-conventional financing of new home purchases—the status they temporarily lost to cash purchases a year earlier following the implemented decline in the 2014 FHA loan limits.”

The share of new single-family homes financed through VA-backed loans remained relatively stable from 2014 to 2015 at 6 percent, while the cash share declined from 13 percent in 2014 down to 10 percent in 2015. The 13 percent share in 2013 marked the first time since 2007 that cash purchases were the most popular form of non-conventional financing for new single-family home purchases.