In a recent First American [1] blog post [2], Mark Fleming [3], First American’s Chief Economist and leader of the Data Sciences team extrapolated what buyers and investors should expect through year-end in terms of Housing Market Potential.

In a recent First American [1] blog post [2], Mark Fleming [3], First American’s Chief Economist and leader of the Data Sciences team extrapolated what buyers and investors should expect through year-end in terms of Housing Market Potential.

Overall, housing market potential sagged to its lowest point since May 2020 in September—when the pandemic brought the country to a near standstill—falling 3.6% from August 2022 to an estimated 5.38 million units at a seasonally adjusted annualized rate (SAAR). On a year-over-year basis, the market potential for existing-home sales is now down 16.7%.

“Market dynamics and the broader economic outlook have changed dramatically in the last 12 months, and that has strongly influenced the fundamentals that drive buyer and seller behavior and the potential for existing-home sales compared with a year ago,” Fleming said. "The higher the mortgage rate, the more sellers will go on strike and the more potential buyers will feel the impact of reduced house-buying power, but price appreciation will further slow and potential buyers can use adjustable-rate mortgages to regain some of that lost house-buying power."

Then vs Now

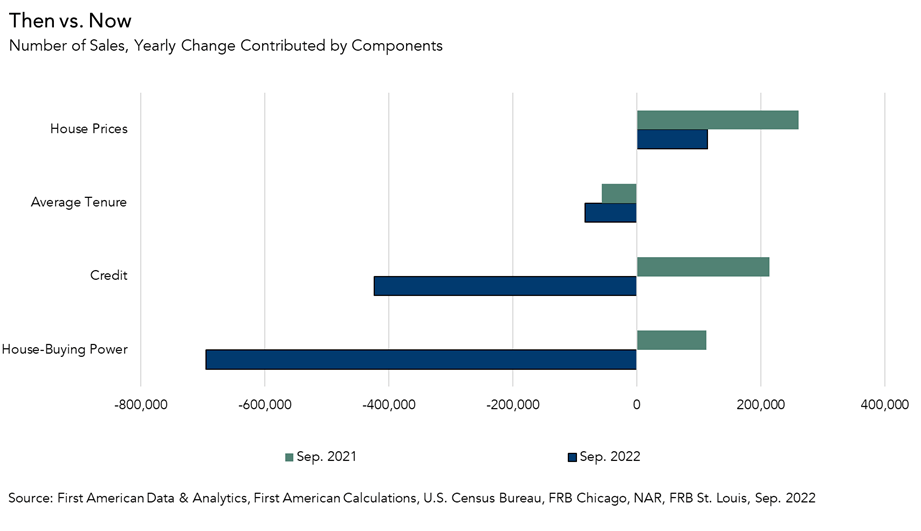

September 2021 marked the highest market potential level recorded since 2007 mainly due to the fact that the average 30-year fixed mortgage rate was 2.9%. Since then, the market has endured constantly rising interest rates which are now toeing the 7% mark. These higher rates have dual effect on the housing market. Firstly, rising rates reduce home-buying power, all things being equal, which in turn dampens home-buying demand and decreases the market potential for existing-home sales.

Compared to September 2021, house-buying power is now down 29%, equivalent to a loss of 695,000 home sales. Ninety-three percent of outstanding mortgages now have a rate under 6% as of the second quarter of 2022.

“As mortgage rates approach 7 percent and the gap between most homeowners current mortgage rate and the prevailing market rate grows, the financial disincentive for homeowners to sell their homes and buy a new home at the higher prevailing mortgage rate increases,” Fleming wrote. “The rate lock-in effect prevents more new supply from reaching the market and reduces the number of home sales. Homeowners staying put reduced housing market potential by 84,000 sales in September compared with one year ago.”

When lending standards are tight, fewer people can qualify for a mortgage to buy a home. Tighter credit conditions resulted in 424,000 fewer potential home sales compared to one year ago.

So, What’s Next?

While in hindsight, it is clear that the ultra-low mortgage rates lenders were offering during the pandemic “super-charged” housing market potential, but what is in store for potential home sales now that rates are slated to keep rising?

“As long as inflation remains high, there will be upward pressure on mortgage rates as the Federal Reserve continues to aggressively tighten monetary policy,” Fleming said. “The higher the mortgage rate, the more sellers will go on strike and the more potential buyers will feel the impact of reduced house-buying power, but price appreciation will further slow and potential buyers can use adjustable-rate mortgages to regain some of that lost house-buying power.”

“While not the frenzy of 2021, the largest living generation, the millennials, will continue to age into their prime home-buying years, creating a demographic tailwind for the housing market,” Fleming concluded.

Click here [2] to read Mark Fleming’s blog post in its entirety.