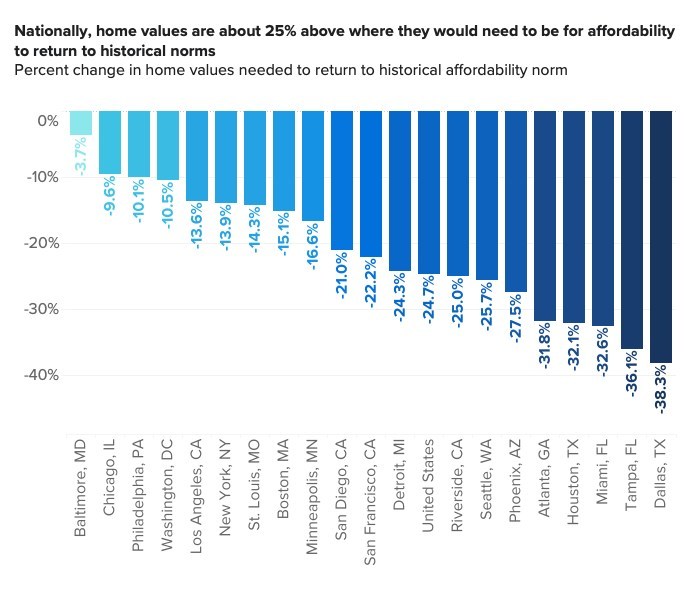

Housing affordability is now the worst its been in several years according to a new analysis by Zillow, [1] showing home values are nearly 25% above where they would need to be for affordability to return to recent norms. Nationally, home values are roughly 25% above where they would need to be for affordability to return to historical norms. Meanwhile, Zillow experts say a substantial home value correction is highly unlikely, causing many homebuyers to pull back.

The monthly mortgage payment on a typical U.S. home is an estimated $1850—about 75.5%, or roughly $800, higher than it was a year ago. Home values have fallen a bit since the peak in June, but rising mortgage rates have overwhelmed those small affordability gains. Mortgage affordability—the share of income a median household would need to spend on a typical mortgage payment—has risen to 30.2% nationally, even before including the cost of taxes and insurance.

Key Findings:

- The share of income required to afford a mortgage has risen to 30.2%, well above the norm of 22.8%.

- Nationally, home values are about 25% above where they would need to be for affordability to return to normal. It is extremely unlikely home values will fall to this degree. Zillow forecasts home value growth will be nearly flat over the next 12 months.

- A sharp inventory increase would be needed for home values to fall dramatically. However, there have been roughly 11% fewer new listings on the market so far this year compared to 2019.

"The next several years appear set up for affordability to be a major challenge for home buyers," said Zillow Senior Economist Nicole Bachaud. "Inventory remains tight, real income growth is dismal, mortgage rates show no signs of dropping, and there is plenty of pent-up demand ready to bid prices back up if they reach a level would-be buyers can once again afford. Filling the housing deficit continues to be the key to long-term affordability, but the recent slowdown in single-family construction is not a good sign that the market is getting closer to building enough to meet demand."

For mortgage affordability to return to the 22.8% norm nationally, U.S. home values would need to fall 24.7%. Some markets are much closer to their historical affordability norms—for example, Hartford home values are only 2.4% higher than where they would need to be, and in Baltimore, they are 3.7% higher — but others have seen affordability deteriorate much more. Salt Lake City, Nashville, Dallas, and Las Vegas are furthest away from their historical affordability, at least 37% above where they would need to be to once again reach that level.

Far from a significant drop, Zillow's home value forecast [2] calls for home values to remain nearly flat in the 12 months ending September 2023. It would take a sharp increase in inventory for home values to fall dramatically. That is simply not the case right now. Overall inventory is ticking up, but it remains nearly 40% below pre-pandemic levels and is nowhere near a glut that would put the market in a position for significant price drops.

New listings are coming onto the market at a slower pace, down 16% in September compared to a year prior. In 2022 to date, there have been about 11% fewer homes listed than at this point in 2019. Many homeowners have mortgages with low rates from purchasing or refinancing earlier in the pandemic, and have very little financial incentive to sell while mortgage rates are this high. Most also have significant equity in their homes, which makes it unlikely that a large number of properties will be forced into distressed sales, like many were during the Great Recession.

The housing market slowdown is being driven by discouraged buyers pulling back as their budgets are stretched. Some buyers simply have been priced out of today's market, but those who are waiting for affordability to improve will likely have a long waiting period ahead. If home values continue to fall, buyers will likely reenter the market and drive values back up. And while mortgage rates are nearly impossible to predict, inflation pressures remain strong, and it's perhaps a better bet that rates will rise further than come back down.

Affordability is projected to be a major challenge for homebuyers going forward, with the unlikelihood of affordability improving and/or return to pre-pandemic norms anytime soon.

To read the full report, including more data, charts and methodology, click here [3].