After two years of unprecedented growth, home values fell slightly from June to July, according to the latest market report from Zillow. The market is quickly rebalancing, gradually returning back to pre-pandemic norms with buyers' purchasing power being diminished by nearly two years of double-digit price growth and higher mortgage rates —resulting in competition for homes dropping off.

The typical U.S. home value declined by 0.1% —or $366— month-over-month in July and now stands at $357,107, as measured by the raw Zillow Home Value Index (ZHVI). Monthly growth in this metric has relaxed since reaching a recent peak of 1.9% in April, slowing to 1.2% growth in May and 0.8% growth in June. It's not unusual for home price growth to decelerate this time of year, but the small decline is the first monthly dip since 2012. The nation's typical home value is up 16% year-over-year and 44.5% since July 2019.

"Home values flattening so quickly after recent record growth might surprise, but it's a badly needed rebalancing that gives home buyers more options, more time to shop and more negotiating power," said Zillow Chief Economist Skylar Olsen. "This slowdown is about discouraged buyers pulling back after the affordability shock from higher rates. As prices soften, many will renew their interest, and we will continue our progress back to 'normal.' With buyers ready in the wings once confidence returns, homeowners can expect to keep the majority of the equity gains they've seen in the last two years."

Home values measured by raw ZHVI fell from June to July in 30 of the 50 largest metro areas, an increase from 13 the previous month.

The largest monthly home value declines were in: San Jose (-4.5%) and San Francisco (-2.8%) — the nation's most expensive major markets — followed by Phoenix (-2.8%) and Austin (-2.7%), which saw the most extreme growth over the pandemic. Values rose the most since June in Miami (1.5%), Richmond (1%), and Memphis (0.9%), although monthly growth has decelerated in these markets.

Home shoppers still on the hunt have more time to find and consider their options, and have a better chance of seeing price cuts. Listings' median days to pending jumped by two days in July to 10 — still nearly two weeks less than in July 2019. Among major metros, typical time on market is rising fastest in Austin, Phoenix and San Jose. A wide swath of sellers are adjusting pricing to meet buyers' expectations, as the share of listings with a price cut grew to 18.6% in July, a few percentage points higher than in July 2019.

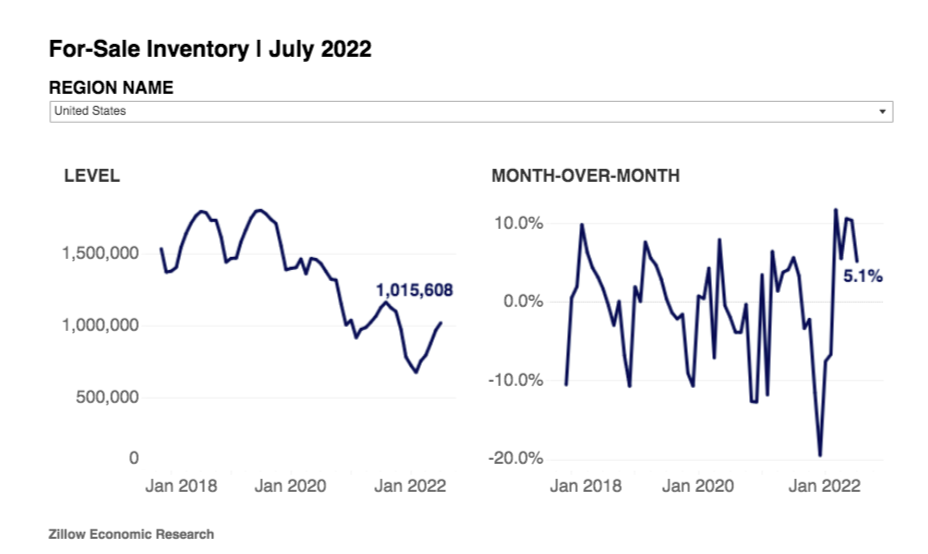

Homes lingering on the market are driving for-sale inventory up at a fast clip. Inventory is up 5.1% on a monthly basis, yet new inventory fell 13.6% month-over-month in July. Compared to July 2019, 15.5% fewer new listings came on the market. This new inventory figure does not include new construction, so it represents current homeowners deciding not to list their homes.

While total inventory is rising quickly, it still stands 43.5% below July 2019. Low inventory is a key reason Zillow economists do not expect home prices to fall significantly.

Among major metros, the most significant slowdowns in monthly rent growth since July of last year occurred in:

- Las Vegas (from 3.6% to -0.2%)

- Phoenix (3.5% to -0.3%)

- Tampa (3.9% to 0.3%)

- Austin (3.8% to 0.7%)

"Inventory, the pool of homes available during a given window, is very responsive to easing demand and slowing sales, this year posting the largest month-over-month seasonal increases for any May, June or July ever recorded," said Olsen. "The flow of homes into the market, however, is slowing. High interest rates are likely keeping current homeowners from deciding to list, as they compare their current rate —and home— against what can be found on the market, keeping inventory far below pre-pandemic norms despite the slowdown in sales."

Typical monthly rent in the U.S. is now $2,031. After a rapid run-up that peaked in February, rent hikes appear to be stabilizing, easing to 0.6% month-over-month growth in July after seeing higher volatility through much of 2021. Although growth is decelerating, the annual growth rate is still more than three times that of July 2019.

To read the full report, including more charts and methodology, click here.