Editor's Note: This feature originally appeared in the August issue of MReport, out now.

There’s a reason why fintech is often called the savior of the mortgage industry. Though most lenders, servicers, and structured finance issuers have some idea of how to optimize their processes, they generally don’t have the team—nor the time and resources to dedicate—to build the necessary tools to do it. These organizations are more focused on growing their core businesses and their staff, and in many cases, they live in an insulated, siloed area of the business, making it harder to see the overall impact a tool could have on the larger mortgage lifecycle.

Thus, the opportunity for fintech firms to swoop in and save the day is created—and save the day they will. Not only are carefully chosen fintech tools going to help traditional mortgage lenders make more money, but they also have the power to increase consistency across business lines, insulate fraud, and make regulation easier to comply with, all while providing a better borrower experience in the process. (And happy borrowers mean happy returns and repeat business.)

The key to all this lies in finding the right fintech tools for the right point in the mortgage process.

Finding the Right Fit

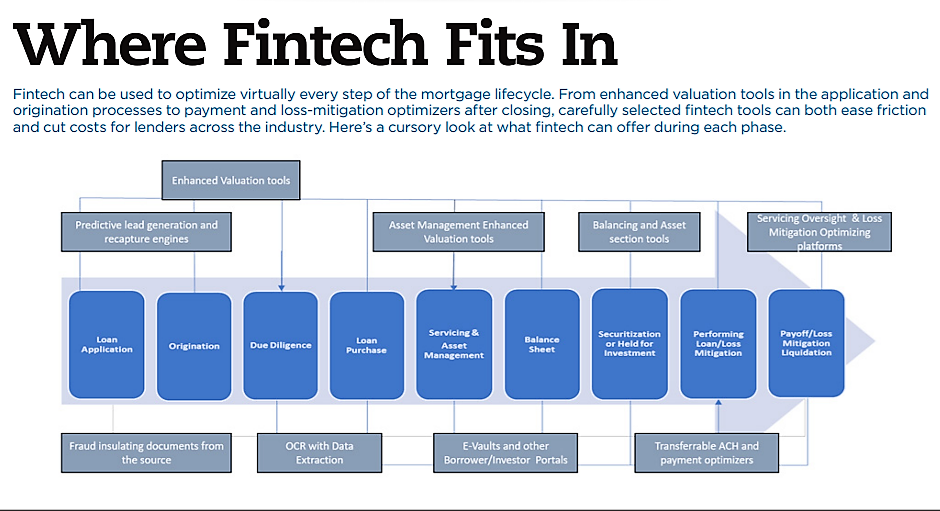

With increased regulation and the vast array of other challenges today’s market poses, mortgage lenders need fintech partners who have real knowledge in their area of business (origination, servicing, structured finance, etc.)—or who have partnered with industry veterans in those areas. This allows them to truly understand the challenges a lender faces today, as well as provide tools and tech that can streamline, enhance, and improve what the lender is already doing. Here’s an example of what fintech can offer in each unique line of the mortgage business:

NEW ORIGINATION

Point of Sale and Documents-From-the-Source: On average, it takes between five to 10 business days to collect the full array of underwriting documents from a prospective borrower, significantly adding to a borrower’s time-to-close. But with the proper use of fintech, that timeframe could shrink to five minutes or less. By using a fintech point of sale system with documents-from-the-source integrations, you can have underwriting documents (i.e., pay stubs, W2s, bank and asset account statements, tax returns, a 4506T with e-sign, ID checks, etc.) in only a few minutes. You could also easily prequalify the borrower, automatically populate their loan application with known data, and start pulling credit and pricing information immediately. In the end, this shortens the time to close, on average, by approximately 10 days and saves anywhere from $270 to $400 in operational costs per loan. It also frees up team members to create more loans—and more profits—in any given month.

Document Recognition, OCR, and Data Extraction: Fintech has the power to significantly improve QC processes, both by cutting costs and adding more convenience. Optical character recognition (OCR) tools can extract data from documents and reconcile any corrections needed. In addition, it can be used to identify documents which could prevent team members from stacking a physical delivery file ever again. By implementing these tools, you can insulate risks, deliver cleaner files, and also streamline both the quality control and due-diligence processes, cutting costs and speeding up the timeline in which a loan can be funded and also be purchased. This could allow originators to close and fund 1.5 to two times the amount of loans in the same time.

ASSET MANAGEMENT/SERVICING

Transferrable ACH and Enhanced Budgeting Tools: By integrating an independent payment platform as an opt-in at origination or modification, the mortgage loans you are originating or making reperform will transfer seamlessly (without losing their ACH), and the payments will be sent to the new servicer without issue. These fintech platforms will also allow the borrowers to manage all of their debt in one place, giving them a resource to budget more efficiently, as well as more effectively, to make their mortgage payments on time. As these platforms become more prevalent, we believe that they will be priced into the trade versus other nontransferable ACH programs, as they provide not only better payment performance but also a borrower benefit. This can increase the value of the mortgage loans significantly.

Valuation Products with Asset Management Dashboards: The bulk ordering of broker price opinions (BPOs) equate to hours upon hours of manual work. With fintech valuation and asset-management products, you can instead identify risk and opportunity-based assets immediately. In addition, these tools deliver enhanced valuations with things like accurate repair estimates, property features, and overall marketability—even offering insights into nearby vandalism, freeway noise, railroads, and more. These are all things that impact the value of the property upon sale or rental, and sadly, they’re often missed on today’s manual BPO world.

Fintech tools do all of this at generally the same price as a standard BPO. And even better, they allow you to track the valuation change over time, predict forward-looking valuations in the market through the use of analytics, and also better track foreclosure timelines versus agency standards (where relevant). All in all, it means a smaller team headcount, lower operational costs, and better-valued assets.

STRUCTURED FINANCE

Balancing and Asset Selection Tools: In an ever-changing origination environment (and considering all rating agencies have differentiating criteria for the same products), it’s difficult to be confident when aggregating and pricing loans. Fortunately, balancing and asset selection tools can help. When used as overlays to your pipeline, they allow you to factor in nuances of the assets, regulation, and rating criteria simultaneously, making “balancing” your loans and structuring your securitized pools easier and more efficient.

These tools also allow the aggregator to price more effectively to the exit and ensure the lenders are receiving an additional benefit for loans that offer better characteristics. When used effectively, they can even ensure that you’re not receiving surprise large loan adjustments, geographical hits or drift-related adjustments, and they can also track refreshes. This generally could lead to a better understanding of what subordination levels will be across the agencies, thus optimizing execution.

Not All Fintech is Created Equal

It is clear that fintech can be a significant driver in building our businesses and in increasing our returns, but it’s important to be careful when selecting your partners. Remember: not all fintech is created equal. It takes time and effort to find the proper fintech partners and solutions for your business, but don’t be afraid of it. Dive in, and it will pay off significantly.