As average home prices nationwide skyrocket, California is emblematic of a U.S. market whose prices are being pushed to new limits by a demand that is outpacing available stock.

As average home prices nationwide skyrocket, California is emblematic of a U.S. market whose prices are being pushed to new limits by a demand that is outpacing available stock.

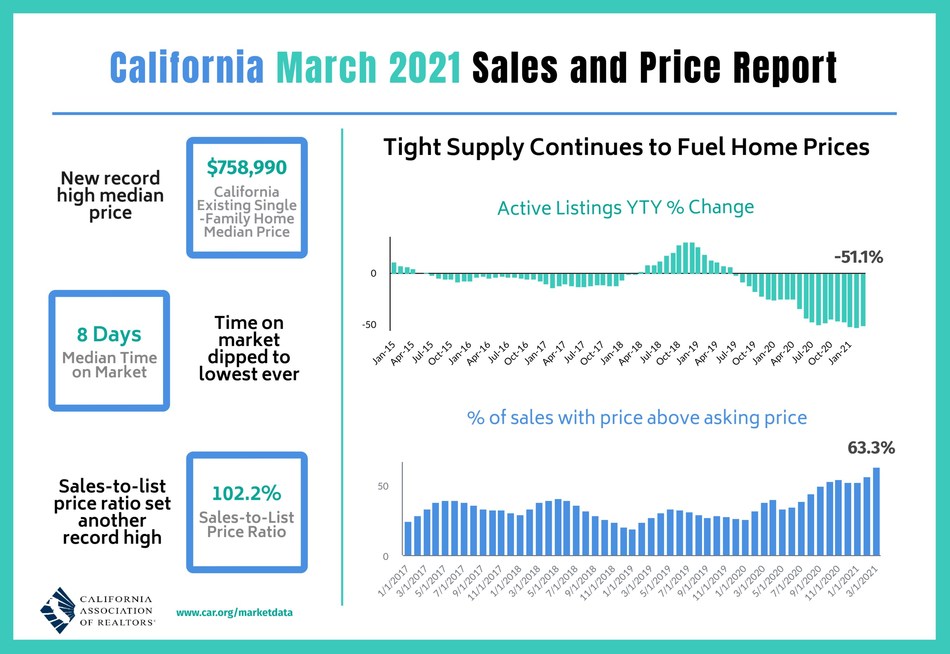

California's median home price reached an all-time high in March, according to the California Association of Realtors (CAR) — that price surged nearly 24% from a year ago. The statewide median home price rose 8.6% on a month-to-month basis to $758,990 in March, up from February's $699,000 and up 23.9% from the $612,440 recorded last March. The year-over-year gain was the highest since October 2013 and it was the eighth straight month that California's median price registered a double-digit gain.

Barring Hawaii, California is the most expensive locale for aspiring homeowners. The brokerage-service franchisor RE/MAX this week released national estimates, showing the median sales price of $303,000 rose 4.5% above its previous report record of $290,050.

Just as other researchers have said, the researchers for CAR remarked that their year-to-year comparisons—like a near-20% annual sales gain, which we touch on momentarily—are skewed by pandemic-spurred restrictions during March 2020 that effectively halted the real estate market and economy.

"The market sentiment is drastically different today compared to a year ago at the onset of the pandemic," said C.A.R. VP and Chief Economist Jordan Levine. "With the U.S. economy positioned to grow at the fastest pace since the early 1980s and mortgage rates trending down again in the past week, consumer confidence will improve further, so in the coming months, we should continue to see a solid bounceback from last year as the market maintains its momentum."

California median home price reaches new all-time high in March as nearly two-thirds of homes sell above asking price.

Closed escrow sales of existing, single-family detached homes in California totaled a seasonally adjusted annualized rate of 446,410 in March, according to information collected by CAR from more than 90 local agents, associations, and MLSs across the Golden State.

Statewide annualized sales figures represent what would be the total number of homes sold during 2021 if sales maintained the March pace throughout the year. It is adjusted to account for seasonal factors that typically influence home sales.

California home sales in March dipped 3.5% from 462,720 in February and were up 19.7% from one year ago when 373,070 homes were sold on an annualized basis.

"While intense homebuying interest is the engine that continues to drive housing demand, a shortage of homes for sales is the rocket fuel pushing prices higher across the state. A lack of homes for sale is creating unprecedented market competition, leading to a record share of homes selling above asking price in March," said C.A.R. President Dave Walsh, vice president and manager of the Compass San Jose office. "With more of the state's COVID-19 restrictions being lifted in the coming months as we move into the spring homebuying season, we should see home sales improve as more prospective home sellers feel comfortable listing their homes for sale."

The full CAR report is available at CAR.org.