As 2023 brought with it mortgage rates bordering the 8%-mark, the final two months of the year saw a steady decline from that high point, as 2024 kicked off with a slight rise in the 30-year fixed-rate mortgage (FRM) according to Freddie Mac.

As 2023 brought with it mortgage rates bordering the 8%-mark, the final two months of the year saw a steady decline from that high point, as 2024 kicked off with a slight rise in the 30-year fixed-rate mortgage (FRM) according to Freddie Mac.

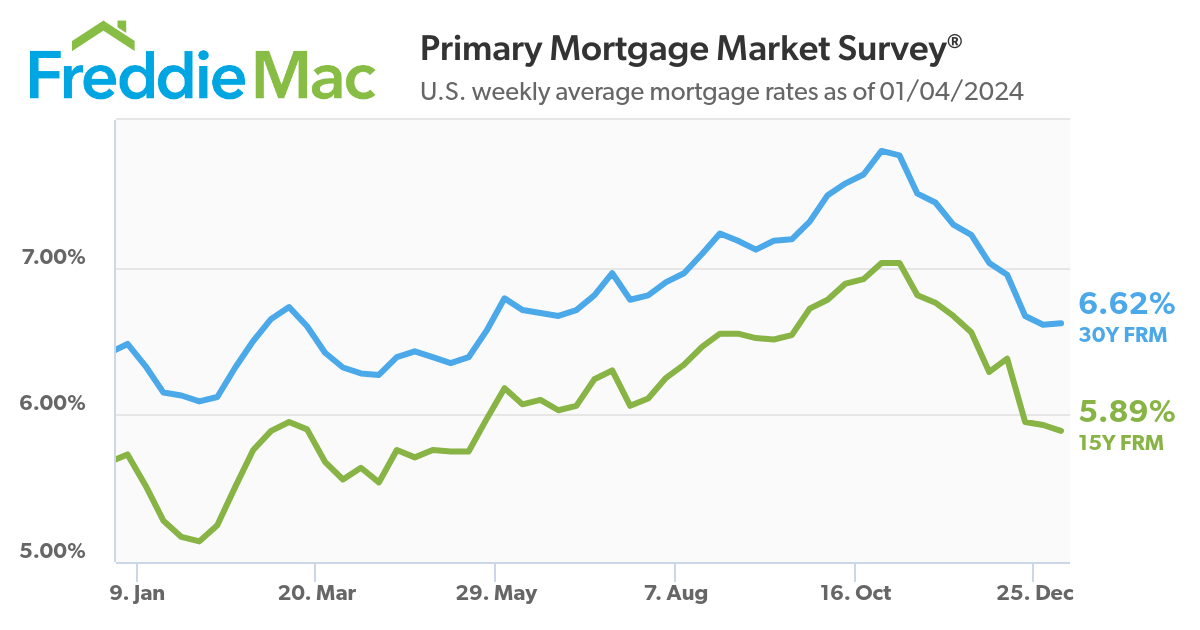

The latest Primary Mortgage Market Survey (PMMS) from Freddie Mac as of January 4, 2024, found the the 30-year FRM averaging 6.62%, up slightly from last week’s reading of 6.61%. A year ago at this time, the 30-year FRM averaged 6.48%.

Also this week, the 15-year FRM averaged 5.89%, down from last week when it averaged 5.93%. A year ago at this time, the 15-year FRM averaged 5.73%.

“Between late October and mid-December, the 30-year fixed-rate mortgage plummeted more than a percentage point. However, since then, rates have moved sideways as the market digests incoming economic data,” said Sam Khater, Freddie Mac’s Chief Economist. “Given the expectation of rate cuts this year from the Federal Reserve, as well as receding inflationary pressures, we expect mortgage rates will continue to drift downward as the year unfolds. While lower mortgage rates are welcome news, potential homebuyers are still dealing with the dual challenges of low inventory and high home prices that continue to rise.”

Freddie Mac’s PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

“The Freddie Mac fixed rate for a 30-year loan leveled off this week, increasing just one basis point to 6.62% as the new year began and markets adjusted to incoming economic data,” added Realtor.com Senior Economic Research Analyst Hannah Jones. “The recent mortgage rate plummet past 7% is likely to bring some buyers into the market. Per a recent Realtor.com survey, 11% of prospective buyers say rates would need to dip below this threshold to make it feasible for them to purchase their next home. Though the recent decline in rates has inspired optimism, 12% of prospective homebuyers say rates would need to dip below 6% and more than one-quarter (28%) say rates would need to dip below 4% to bring them into the market. The typical outstanding mortgage has a rate of less than 4%, more than 2.5 percentage points below today’s rate. This gap is likely to keep many sellers on the sidelines, waiting for mortgage rates to come down further.”

And despite the recent slide in mortgage rates, the Mortgage Bankers Association (MBA) reported that conditions during the 2023 holiday season were not exactly ideal for potential home buyers, as the MBA’s Weekly Mortgage Applications Survey for the week ending December 29, 2023 saw mortgage application volume dropping 9.4% from two weeks earlier (note that the MBA’s results included adjustments to account for the holiday season).

“Mortgage rates finished 2023 more than a percentage point lower than their peak in October, but applications to refinance, and buy a home both declined in the final two weeks of the year,” said MBA President and CEO Robert D. Broeksmit, CMB. “MBA expects mortgage rates to continue to decline slowly, which along with more new and existing housing inventory should boost homebuying activity in the months ahead.”

Optimism in the home building sector may alleviate the nation’s housing supply issue, as the latest National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI), having found that the recent slide in mortgage rates has helped end a four-month decline in builder confidence, along with recent economic data signal improving housing conditions heading into the new year. The Index found builder confidence in the market for newly built single-family homes rose three points to 37 in December, reversing the trend of the previous four months.

“With mortgage rates down roughly 50 basis points over the past month, builders are reporting an uptick in traffic as some prospective buyers who previously felt priced out of the market are taking a second look,” said NAHB Chairman Alicia Huey. “With the nation facing a considerable housing shortage, boosting new home production is the best way to ease the affordability crisis, expand housing inventory, and lower inflation.”

Jones added, “Pending home sales leveled off in November, matching the previous month’s record-low level. Mortgage rates fell each week in November, but remained above 7% throughout the month, which kept contract signings stable at a low level. Moving forward, the continued decline in mortgage rates will be contingent on cooling inflation and employment data. This week’s Job Openings and Labor Turnover data showed slowing hires and separations, suggesting that Friday’s employment data may follow suit and continue to slow. The current path of falling inflation and employment activity suggests that the Fed’s goal of a ‘soft landing’ may be within reach. Though 2% inflation has not yet been achieved, progress towards this level is good news for the housing market.”