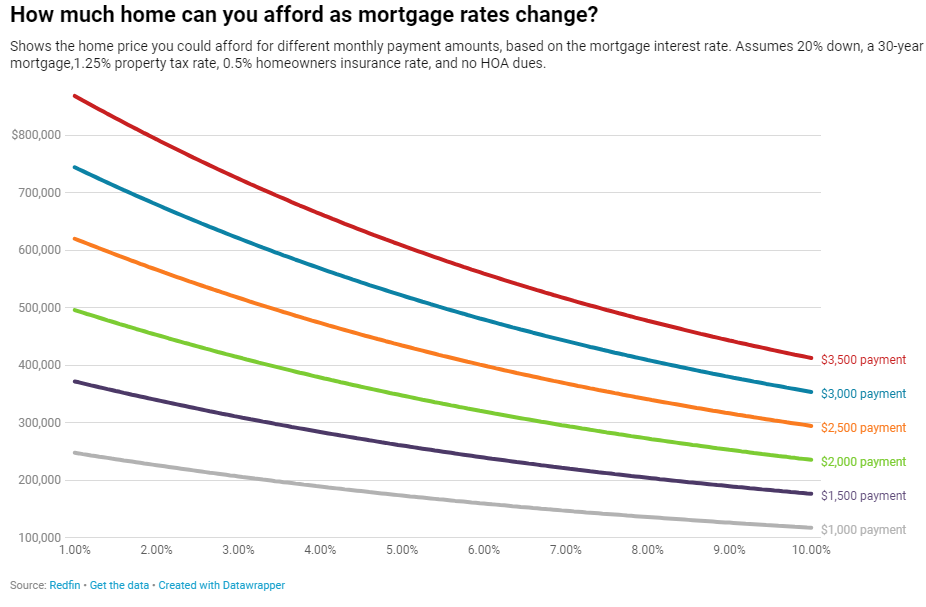

According to new Redfin report, a homebuyer on a $3,000 monthly budget has gained nearly $40,000 in purchasing power since mortgage rates peaked this past fall. Redfin estimates that a $3,000 monthly budget will buy a $453,000 home with a 6.7% mortgage rate, roughly this week's average. That total is compared to the $416,000 home the same buyer could have purchased in October 2023 with an average rate of 7.8%.

According to new Redfin report, a homebuyer on a $3,000 monthly budget has gained nearly $40,000 in purchasing power since mortgage rates peaked this past fall. Redfin estimates that a $3,000 monthly budget will buy a $453,000 home with a 6.7% mortgage rate, roughly this week's average. That total is compared to the $416,000 home the same buyer could have purchased in October 2023 with an average rate of 7.8%.

Analyzing affordability from another perspective, the monthly mortgage payment on the typical U.S. home, which currently costs roughly $363,000, is $2,545 with a 6.7% rate. The monthly payment was nearly $200 higher—$2,713—when rates were at 7.8%.

Recently, homebuyers have found some relief in as mortgage rates have slipped from their two-decade high hit this past October. Weekly average rates dipped into the 6.5% range by the end of 2023, and ticked up slightly to 6.7% this week. While that’s double the record-low 3% rates buyers experienced during the pandemic, Redfin agents report that buyers have come to terms with a 30-year, fixed-rate mortgage (FRM) in the 6% range—but they were more hesitant when they were approaching the 8% mark.

“Bidding wars are picking up as mortgage rates decline and inventory stays low. I’ve seen a few homes get 15-plus offers recently, and one got more than 30,” said Shoshana Godwin, a Redfin Premier agent in Seattle. “Late last year, many listings sat on the market as buyers sat on the sidelines, hoping for rates to drop. Now, buyers are snapping up homes because even though rates haven’t plummeted, people are realizing that the longer they wait to buy a home, the more competition they’re likely to face.”

Many Redfin economists forecast mortgage rates will end the year lower than they started, but the path is likely to be bumpy. Redfin is keeping an eye on this week’s Federal Open Market Committee (FOMC) meeting, set for January 30-31, to provide more clues on how soon they will cut interest rates: It could be as soon as March, but it’s likely to be later. Mortgage rates should come down a little—but not a lot—when interest rates are cut.

For the third meeting in a row in mid-December, the FOMC made the call that their best course of action was to do nothing with interest rates, a developing trend as the Committee also chose to hold rates steady at 5.50% at their last two meetings.

The most aggressive series of rate hikes in history ended in June when the FOMC held off on raising rates due to a number of positive factors which forced 11 straight rate hikes over 15 months. Since the post-pandemic rate hikes began, the FOMC raised rates in March 2022 (+25 points), May 2022 (+50 points), June 2022 (+75 points), August 2022 (+75 points), September (+75 points), November 2022 (+75 points), December 2022 (+50 points), February 2023 (+50 points), March 2023 (+25 points), May 2023 (+25 points), June 2023 (+0 points), July (+25 points), September (+0 points), November (+0 points), and December (+0 points). This is equivalent to a rise of 5.00 percentage points in under two years.

“My advice to serious house hunters: Trying to time the market around mortgage rates is probably a waste of energy, as affordability is unlikely to change meaningfully in the next several months,” said Redfin Chief Economist Daryl Fairweather. “Instead, buyers should consider their own personal and financial circumstances: What matters most is whether the home meets your needs long term and whether you can afford it. Timing the market mattered in 2021, when we were in a golden window of record-low rates—but that window is closed.”

According to the National Association of Realtors (NAR) Pending Home Sales Index (PHSI)—a forward-looking indicator of home sales based on contract signings—increased in December to an Index level of 77.3, a 1.3% increase. The Index was benchmarked to 100 based on the level of contract signings in the year 2001.

"The housing market is off to a good start this year, as consumers benefit from falling mortgage rates and stable home prices," said Lawrence Yun, NAR Chief Economist. "Job additions and income growth will further help with housing affordability, but increased supply will be essential to satisfying all potential demand."