Pending home sales are trending up according to the National Association of Realtors (NAR) most recent report the Pending Home Sales Index, which tracks home sales based on contract signings—a forward-looking statistic of home sales.

Pending home sales are trending up according to the National Association of Realtors (NAR) most recent report the Pending Home Sales Index, which tracks home sales based on contract signings—a forward-looking statistic of home sales.

According to the index, pending home sales improved 8.1% to an index of 82.5 in January 2023. However, year-over-year, this number is down by 24.1%. The index was benchmarked to 100 using housing data from 2001.

“Buyers responded to better affordability from falling mortgage rates in December and January,” said NAR Chief Economist Lawrence Yun.

The NAR anticipates the economy will continue to add jobs throughout 2023 and 2024, with the 30-year fixed-rate mortgage rate steadily dropping to an average of 6.1% in 2023 and 5.4% in 2024.

Yun still expects that the improving job market combined with improving interest rates will help out pending home sales numbers—however—he is predicting an 11.1% drop in existing-home sales to an annual rate of 4.47 million units in 2023 and a jump of 17.7% in 2024 to a rate of 5.26 million units. NAR projects new-home sales will fall 3.7% year-over-year in 2023 before growing 19.4% in 2024.

“Home sales activity looks to be bottoming out in the first quarter of this year, before incremental improvements will occur,” Yun said. “But an annual gain in home sales will not occur until 2024. Meanwhile, home prices will be steady in most parts of the country with a minor change in the national median home price.”

Further, Yun predicts the national median home price will decrease by 1.6% in 2023 to $380,100 but will increase in 2024 by 3.1% to $391,800. New home prices are expected to increase by 1.3% in 2023 to $461,000 and increase another 2.8% in 2024 to $474,000, mainly due to the increasing cost of land and raw building materials.

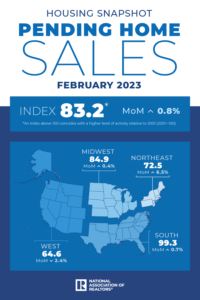

By region, the Northeast PHSI rose 6.0% from last month to 68.7, a decline of 19.8% from January 2022. The Midwest index grew 7.9% to 83.3 in January, a drop of 21.1% from one year ago.

The South PHSI increased 8.3% to 99.2 in January, dipping 24.7% from the prior year. The West index elevated 10.1% in January to 66.2, diminishing 29.3% from January 2022. “An extra bump occurred in the West region because of lower home prices, while gains in the South were due to stronger job growth in that region,” Yun added.

Realtor.com Chief Economist Danielle Hale also commented on the report:

“Data on contract signings show that home shoppers took advantage of lower mortgage rates, with pending home sales tallying roughly the same during February’s swell as during January’s swoon,” Hale said. “Because contract signings precede home sales, today’s data suggest that February’s pick-up in home sales may not be a one-off, especially as home sales prices have begun to ease in response to the affordability hurdles the combo of high rates and home prices presents.”

“Today’s pickup in activity signals that it is possible for buyers and sellers to come to an agreement on the terms of sale, but other market data point to the importance of having reasonable, data-based expectations of today’s housing market in order to find success,” Hale continued. “For sellers, this means understanding that even as home prices remain relatively high, homes are not selling as quickly and that buyers may have more options when compared to last year.”

“Sellers who make improvements before listing can help keep buyers focused on the best features of a home instead of being distracted by issues that are easily fixed,” Hale concluded. “Sellers will need to allocate the time to make these repairs and soon if they’re hoping to take advantage of mid-April’s best time to sell. For more than half of recent sellers, it took longer than expected to prep their home for sale."

Bright MLS Chief Economist Dr. Lisa Sturtevant had the following comments on the Pending Home Sales data:

“New pending sales rose for the third month in a row in February, but the 0.8% uptick over January was more modest than what we would see in a typical runup to the spring housing market,” Sturtevant said. “Homebuyers have been closely watching mortgage rates, which have been volatile during the first few months of the year. Even though rates ticked up in February, some buyers took the plunge anyway, anxious that mortgage rates would be moving even higher this spring.”

“Pending sales activity might have been higher if there had been more homes available on the market. It seems inconceivable that even as mortgage rates are double what they were a year ago, we are still talking about how low inventory is making buying a home a competitive sport,” Sturtevant continued. “Supply has increased from last year, but the number of homes available for sale is still just half of what it was three years ago.”

“This spring, the housing market will be much calmer than the fast-paced environment of 2021 or even 2022,” Sturtevant concluded. “At the same time, buyers will still face competition in the market and will need to be prepared to make an offer when they find a home they love. Sellers will find ready buyers if they set their list price realistically and are open to negotiations.”