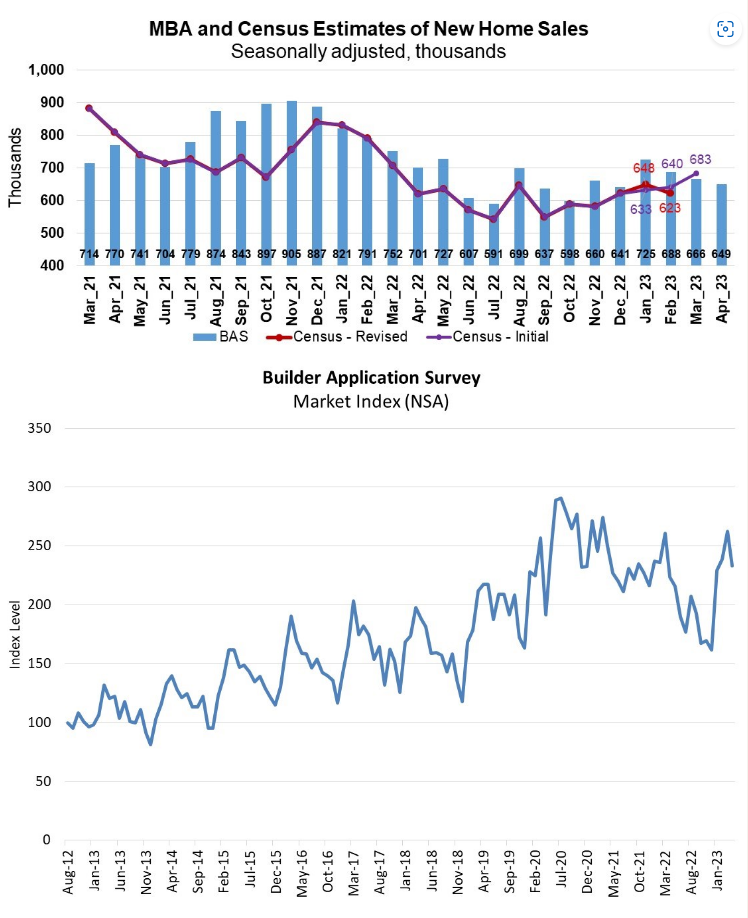

The Mortgage Bankers Association (MBA) Builder Application Survey (BAS) data for April 2023 shows mortgage applications for new home purchases increased 4.1% year-over-year, and compared to March 2023’s totals, applications decreased by 11%.

The Mortgage Bankers Association (MBA) Builder Application Survey (BAS) data for April 2023 shows mortgage applications for new home purchases increased 4.1% year-over-year, and compared to March 2023’s totals, applications decreased by 11%.

“Purchase applications for newly constructed homes declined in April but were up 4% compared to a year ago,” said Joel Kan, MBA’s VP and Deputy Chief Economist. “This was the third straight month of year-over-year growth in applications, which signals improving housing demand for newly built homes at a time when the broader housing market is leaning more on new construction to boost for-sale inventory levels. Mortgage rates have settled in the 6.5% range lately and remain over a percentage point higher than last year. The higher mortgage rate environment continues to factor into homebuying and selling decisions.”

MBA estimates new single-family home sales, which has consistently been a leading indicator of the U.S. Census Bureau’s New Residential Sales report, is that new single-family home sales were running at a seasonally adjusted annual rate of 649,000 units in April 2023, based on data from the BAS. The new home sales estimate is derived using mortgage application information from the BAS, as well as assumptions regarding market coverage and other factors.

The seasonally adjusted estimate for April is a decrease of 2.6% from the March 2023 pace of 666,000 units. On an unadjusted basis, MBA estimates that there were 58,000 new home sales in April 2023, a decrease of 10.8% from 65,000 new home sales in March.

“Since the brief pick-up in new home sales in January when mortgage rates dipped, the pace of new home sales has declined for the three consecutive months,” noted Kan. “With the recently released Census data showing single-family permitting activity on the upswing and housing starts also rising, we expect that to translate to growth in new home sales activity in the second half of the year.”

By product type, the MBA reported that conventional loans composed 66.2% of loan applications, FHA loans composed 23.4%, RHS/USDA loans composed 0.4%, and VA loans composed 10%. The average loan size of new homes decreased from $407,015 in March 2023 to $401,756 in April 2023.

In its latest report, the National Association of Home Builders (NAHB) found that the lack of existing inventory has boosted builder confidence. Builder confidence in the market for newly-built single-family homes in May rose five points to 50, according to the NAHB/Wells Fargo Housing Market Index (HMI)—marking the fifth consecutive month that builder confidence has increased, and is the first time that sentiment levels have reached the midpoint mark of 50 since July of 2022.

“Lack of existing inventory continues to drive buyers to new construction,” said NAHB Chief Economist and SVP of Economics and Housing Policy Robert Dietz. “In March, 33% of homes listed for sale were new homes in various stages of construction. That share from 2000-2019 was a 12.7% average. With limited available housing inventory, new construction will continue to be a significant part of prospective buyers’ search in the quarters ahead.”