It may be a hard pill to swallow, but the U.S. economy is stalling as higher interest rates are weighing on rate-sensitive sectors like housing and credit. But, the economy remains resilient, and the broader economy has weathered several adverse shocks since the COVID-19 pandemic and has yet to reach recession conditions.

It may be a hard pill to swallow, but the U.S. economy is stalling as higher interest rates are weighing on rate-sensitive sectors like housing and credit. But, the economy remains resilient, and the broader economy has weathered several adverse shocks since the COVID-19 pandemic and has yet to reach recession conditions.

Housing activity has slowed, to be clear, but favorable demographic tailwinds from first-time home buyers have bolstered the housing market and led to surprising news: the total homeownership rate can be attributed to the strong growth in the below-median income homeownership rate, which has increased from 48% to 53.4% since 2016.

Looking at the economy as a whole, the U.S. Bureau of Economic Analysis reported that the Gross Domestic Product (GDP) up by 0.2% to an annualized rate of 1.3% during the first quarter of 2023. This marks the third consecutive quarter of positive GDP growth, but the pace is slowing. This number is also influenced by Gross Domestic Income (GDI), which decreased 2.3% during the first quarter of 2023.

According to Freddie Mac, in theory, GDP and GDI should be identical as aggregate expenditures always equals income. However, research has shown that the GDI measure can be more predictive of future output growth than GDP.

Despite the potential contraction in activity indicated by GDI, the labor market remains resilient. The unemployment rate did increase in May by 0.3 percentage points to 3.7%; the largest month-over-month increase since the onset of the COVID-19 pandemic. However, an increase in job openings caused the ratio of job openings to unemployed persons to jump up to 1.79 in April 2023 from 1.67 the month before. Despite the rise in the unemployment rate reported in the household survey, the establishment survey reported that nonfarm payrolls increased by 339,000 in May. In addition, average hourly wages increased 0.3% over-the-month, and 4.3% year-over-year, to $33.44/hr.

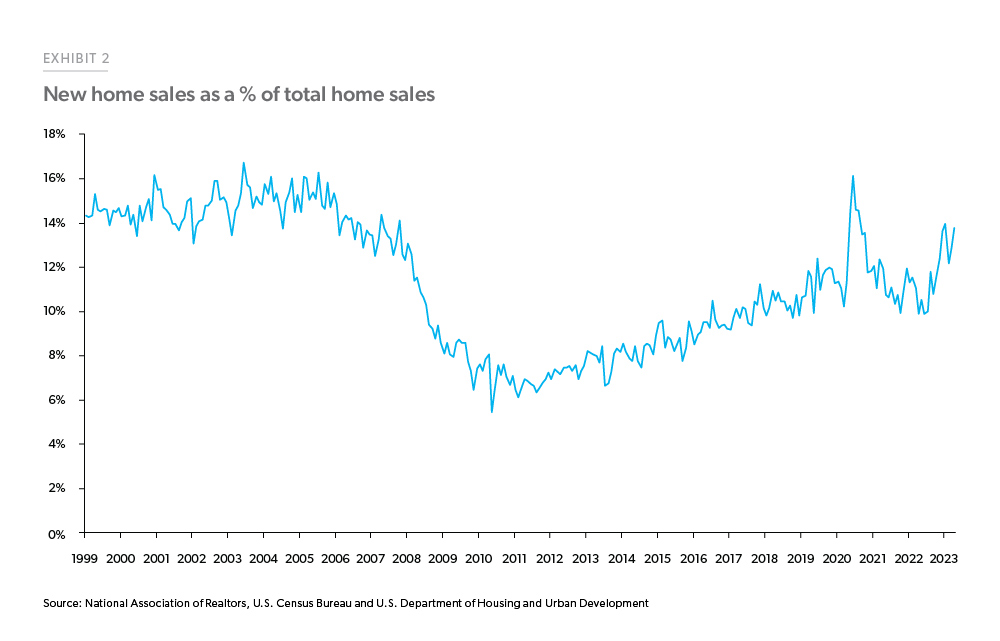

Looking specifically at the housing market, per the National Association of Realtors (NAR), existing home sales pulled back by 3.4% in April to a seasonally adjusted annual rate of 4.28 million. In addition, a separate report from the U.S. Census Bureau and the Department of Housing and Urban Development found that new home sales increased 4.1% in April. Since the beginning of the year, existing home sales have averaged a seasonally adjusted 655,000 sales, a 2% increase year-over-year. The simultaneous decline of existing home sales and increase of new home sales has shifted the composition of the home sales market toward new home sales.

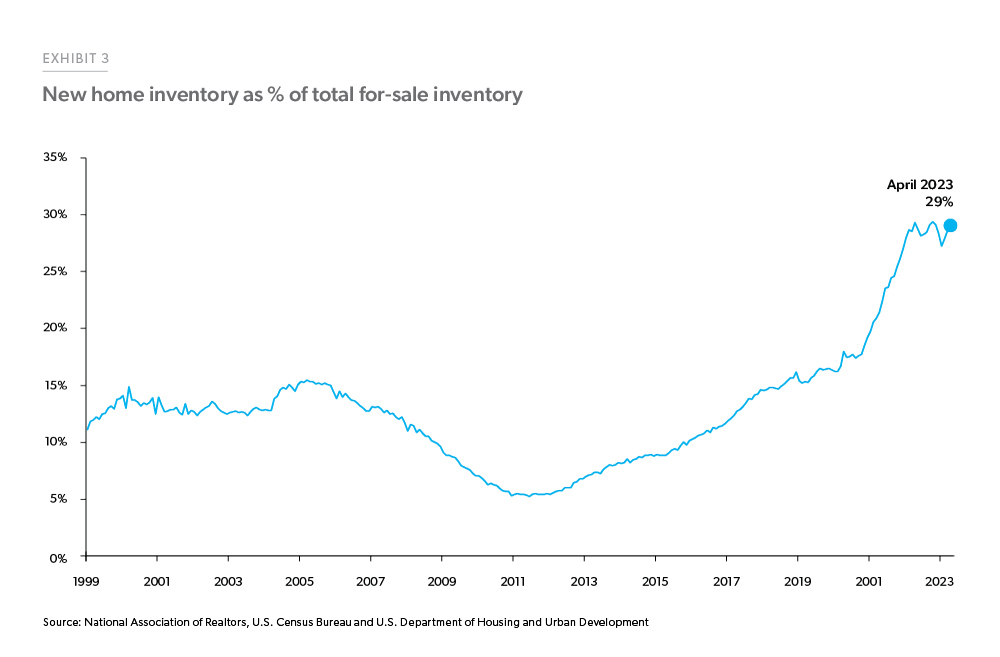

Citing an NAR report, Freddie Mac reported that as of April, there is 2.9 months’ supply of existing homes based on the current rate of sales. Existing homes typically sold in 22 days in April. Looking at new homes, there is a 7.6 months’ supply according to the Census Bureau. Overall, the total number of single-family homes available for sale remains low at 1.3 million units, only 8.1% above its all-time low in February 2022. Furthermore, as the number of existing homes available for sale has dwindled while available new homes are relatively higher, the share of active for-sale inventory of new homes has reached near 30%.

Freddie Mac says the divergence between the new and existing home sales markets are suggestive of the lock-in effect because homeowners with lower rates on their mortgages have a lower propensity to list their home due to today’s elevated interest rates.

Among recent developments in the mortgage market, the standard 30-year fixed-rate mortgage have begun to increase, recently coming in at 6.79%, the highest reading since November 2022.

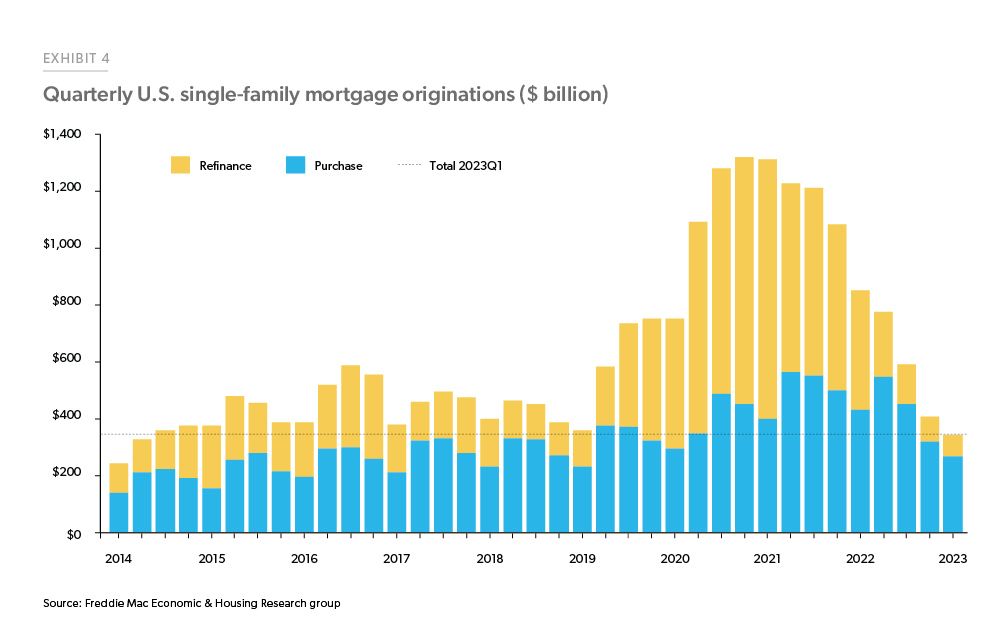

Originations in the first quarter of 2023 totaled $344 billion, the lowest quarterly total since the second quarter of 2014, as higher mortgage rates are dampening mortgage application activity. Purchase applications were down 6.9% during the last week of May, while refinance applications dropped 11% after seasonal adjustment. Due to seasonality in the housing market, mortgage originations will likely increase in the second quarter, but full-year 2023 originations will almost certainly be below 2022 levels.

Still, mortgage performance remains strong, especially when compared to other types of credit. According to data from Transunion, the share of loans 60 days or more past due fell 0.01 percentage points from Q1 2021 to Q1 2023 for mortgages, while it increased by 0.36 percentage points for autos, 0.80 percentage points for Bankcards and 1.1 percentage points for unsecured personal loans over the same period.

“Overall credit performance remains solid for higher credit quality borrowers, but that is in an economy with unemployment rates below 4%,” Freddie Mac said in their report. “If the labor market outlook darkens, mortgage performance could weaken, and rising delinquency rates spread to higher credit quality borrowers.”

Looking ahead, Freddie Mac says the future of the housing and mortgage markets remain uncertain; while Freddie Mac is not forecasting a recession in their baseline outlook rather a slowdown in growth and an uptick in unemployment as the most likely scenario.

Click here to view the report in its entirety.