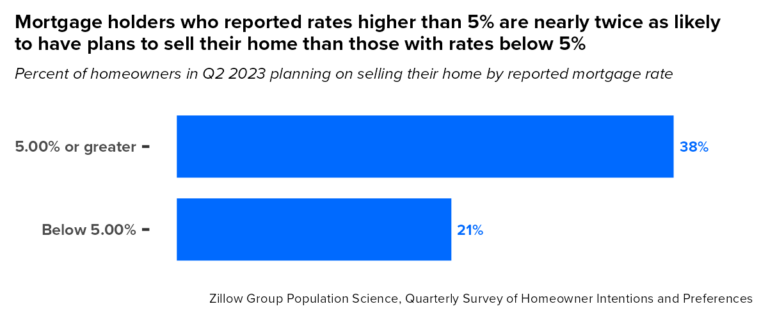

A new survey from Zillow has identified the mortgage rate tipping point that makes homeowners more likely to move is a rate above 5%, as homeowners with a mortgage rate above 5% are nearly twice as likely to say that they plan to sell their home than those paying a rate below 5%.

A new survey from Zillow has identified the mortgage rate tipping point that makes homeowners more likely to move is a rate above 5%, as homeowners with a mortgage rate above 5% are nearly twice as likely to say that they plan to sell their home than those paying a rate below 5%.

Zillow's survey found that approximately 80% of mortgage holders reported having a rate of less than 5%, and nearly 90% currently have a rate less than 6%. Nearly one-third of those surveyed reported a rate of less than 3%.

As today's mortgage rates near 7%, a majority of homeowners would need to finance a new home at a higher rate than the rate they currently hold, adding hundreds of dollars a month to their mortgage payment and creating an incentive to hold on to their home rather than move. This helps explain why Zillow data finds that 28% fewer new for-sale listings hit the market in June 2023 than a year ago.

"We expect mortgage rates may notch down slightly as inflation comes under control, but they are unlikely to return to 5% in the near future," said Orphe Divounguy, a Senior Economist at Zillow Home Loans. "That means many homeowners will move only for major life events, like a new baby or retirement. Over time, homeowners will likely accept higher rates as the new normal, but until then, the market could remain challenging for home shoppers, who will see fewer options and higher prices."

Last week, the Federal Reserve raised rates by 25 basis points after not taking action at their last meeting, as the target rate now stands at 5.25-5.50%.

The most aggressive series of rate hikes in history ended in June when the committee held off on raising rates due to a litany of positive factors which consisted of 10 straight rate hikes over 15 months. Since the post-pandemic rate hikes began, the FOMC raised rates in March 2022 (+25 points), May 2022 (+50 points), June 2022 (+75 points), August 2022 (+75 points), September (+75 points), November 2022 (+75 points), December 2022 (+50 points), February 2023 (+50 points), March 2023 (+25 points), May 2023 (+25 points) and June (+0 points)—equivalent to a rise of five percentage points over the last year.

LendingTree's Senior Economist Jacob Channel explained, “Some may be wondering if mortgage rates will trend even higher owing to the Fed’s decision this week to hike its target funds rate by 25 basis points. While this does mean that the target funds rate is now at its highest level in more than two decades, it’s important to keep in mind that while the Fed influences them, it doesn’t directly set mortgage rates. Instead, mortgage rates are more closely tied to the 10-year treasury yield. Owing to this, mortgage rates could rise or fall over the coming weeks, and, even if they do go up, there’s no guarantee that they’ll increase by exactly 25 basis points.”

Zillow's survey found that nearly 25% of homeowners surveyed are considering selling their home in the next three years, or currently have their home listed for sale (23%), a total significantly higher than the 15% of homeowners who said the same just one year ago. The share is even greater among mortgage holders who have a rate above 5%, as 38% of those homeowners say they would consider selling their home in the next three years.

In the meantime, the shortage of for-sale homes is pushing up home prices. Zillow's latest monthly market report finds that home values hit a record high in June, topping $350,000 for the first time nationally. Home values climbed in all of the 50 largest metro areas for a second consecutive month. These higher home prices are compounding affordability challenges for buyers who are also dealing with mortgage rates bordering the 7%-mark. A typical monthly mortgage payment is more than twice as much as it was in 2020 and 13% higher than a year ago.

And as these challenges have tempered buyer demand, buyers are persisting and are getting creative to achieve their dream of homeownership. Zillow Home Loans recently reported that 45% of all buyers are buying points to lower their interest rate and reduce their monthly mortgage payment. Mortgage points give buyers an option to pay an upfront fee to buy down the interest rate on a loan. Buyers are also making compromises on their wish lists, and are competing for smaller, more affordable homes.

The National Association of Home Builders (NAHB) reports that low existing inventory is keeping demand solid for new homes, which helped push builder confidence up in July. Builder confidence in the market for newly built single-family homes in July posted a one-point gain to 56, according to the latest NAHB/Wells Fargo Housing Market Index (HMI)—the seventh straight month that builder confidence has increased, marking the highest level recorded since June of last year.

“Although builders continue to remain cautiously optimistic about market conditions, the quarter-point rise in mortgage rates over the past month is a stark reminder of the stop and start process the market will experience as the Federal Reserve nears the end of the ongoing tightening cycle,” said NAHB Chief Economist Robert Dietz.