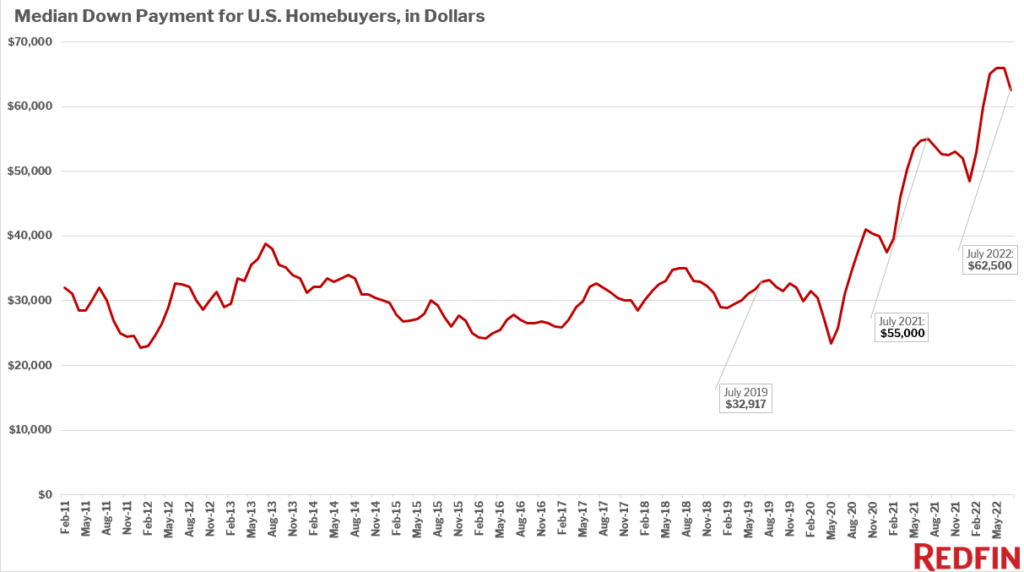

According to a new report from Redfin, the typical U.S. homebuyer who took out a mortgage in July made a whopping $62,500 down payment, up 13.6% from a year earlier, and almost twice the median $32,917 down payment in July 2019, before the pandemic. The combination of increased down payments and monthly mortgage payments nearing all-time highs made it more difficult for prospective buyers to afford homes.

The combination of skyrocketing home prices and intense competition prompted many buyers to up their down payments during the pandemic. However, as the housing market cools amid high mortgage rates and economic uncertainty, –and buyers can no longer afford as much as they used to– down payments are falling from their peak.

However, down payments have declined slightly in recent months after peaking at $66,000 in May and June. The slip is partly because the housing market is cooling amid high mortgage rates, inflation, stumbling stocks, and widespread economic uncertainty. Higher monthly mortgage payments and the rising cost of other goods and services cut into buyers’ budgets, making it harder to come up with huge down payments. A slower housing market also means less competition for homes, which means buyers don’t necessarily need to offer large down payments to win a home.

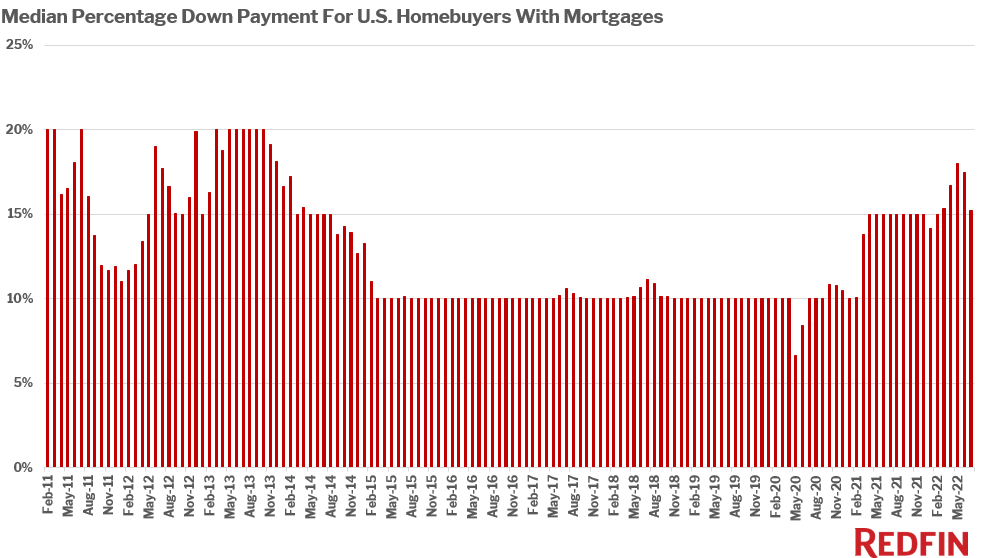

The typical buyer’s down payment in July was equal to 15.2% of the purchase price, essentially unchanged from 15% a year earlier but up from 10% before the pandemic. The typical down-payment percentage hit a nine-year high in May, reaching 18% of a home’s purchase price, before the housing market cooled considerably during the late spring and early summer. Roughly six in 10 —or 58.7% of— buyers who used a mortgage had a 10%-plus down payment, up slightly from 57.5% a year earlier and up from the 50% range before the pandemic.

The amount of money homebuyers are putting into down payments —and the percentage they’re putting down— has skyrocketed over the last two years amid the pandemic-driven homebuying boom. Remote work and record-low mortgage rates drove scores of Americans to buy homes during the pandemic, and soaring demand pushed up prices and competition to all-time highs. Although prices are falling from their peak, they’re still near record highs.

Higher home prices are one factor in higher down payments. A 10% down payment, for example, is equal to $40,000 on a $400,000 home and $45,000 on a $450,000 home. Competition is another major factor, with buyers increasing their down-payment dollar amounts and percentages to attract sellers’ attention and communicate that they have plentiful finances to close the deal. If a home receives 10 offers, a common scenario over the last two years before the market slowed, prospective buyers may up their down payment to stand out from the competition.

“Homebuyers don’t need to make enormous down payments anymore because they’re much less likely to encounter bidding wars now that so many Americans have bowed out of the market,” said Redfin Senior Economist Sheharyar Bokhari. “And many buyers can no longer afford to put down 15% or 20% of the purchase prices. Between higher mortgage rates creating higher monthly housing payments and inflation pushing up the prices of everything from food to fuel, buyers need to set aside more money for everyday expenses. That, along with the slumping stock market, is cutting into down-payment budgets. While down payments will likely remain elevated above pre-pandemic levels, they’ll probably fall a bit in the short term.”

Down-payment dollar amounts have increased most in Nashville

Three of the five metros where down payments increased most in July from a year earlier are in New York or New Jersey. The typical down payment was $64,250 in Nashville, Tennessee in July, up nearly 40% from a year earlier —the biggest increase of the metros in Redfin’s analysis. It’s followed by Newark, New jersey ($90,000, up 36.4% year over year), New York City ($197,875, up 34.8%), New Brunswick, New Jersey ($90,000, up 34.3%), and Charlotte, North Carolina ($48,200, up 32.6%).

Down payments fell from 2021 or stayed the same in seven of the 40 metros in Redfin’s analysis, mostly in California. The typical down payment was $55,000 in Riverside, California, down 15.4% year-over-year —the biggest decline of the metros in the analysis. Next comes San Francisco, where the typical down payment of $364,000 was down 7.8% year-over-year. It’s followed by Oakland ($208,775, down 7.7% year-over-year), Warren, Michigan ($25,500, down 7.3%), Detroit, Michigan ($14,250, down 5.2%), and Seattle, Washington ($157,500, down 2.4%). The typical down payment in San Jose, California was $330,000, unchanged from a year earlier.

Down payments likely fell from a year earlier or stayed the same in expensive places like San Francisco and Seattle because they are cooling quicker than other U.S. housing markets, with sale prices starting to decline in the Bay Area.

Denver has seen the biggest uptick in down-payment percentages

In percentage terms, down payments increased most in Denver. The typical Denver homebuyer made a 20% down payment in July, up from 15% a year earlier. It’s followed by Baltimore, where the typical buyer put 8.4% down, up from 5% a year earlier. Charlotte, North Carolina (13%, up from 10.1%), Nashville, Tennessee (15%, up from 12.1%) and Newark, New Jersey (20%, up almost 18%) round out the top five.

Down-payment percentages declined year over year in five of the metros in the analysis. The median down payment percentage dropped to 10% from 15% in Riverside, California. Next comes Detroit, Michigan, where the median down payment percentage dropped to 5% from about 7% a year earlier. It also declined in Las Vegas, San Jose, California, and Milwaukee.

To read the full report, including more charts, metro-level data and methodology, click here.