Ginnie Mae has announced revisions to its definition of High Balance Loans, more closely aligning with the increased conforming loan limits recently announced by the Federal Housing Finance Agency (FHFA).

Ginnie Mae has announced revisions to its definition of High Balance Loans, more closely aligning with the increased conforming loan limits recently announced by the Federal Housing Finance Agency (FHFA).

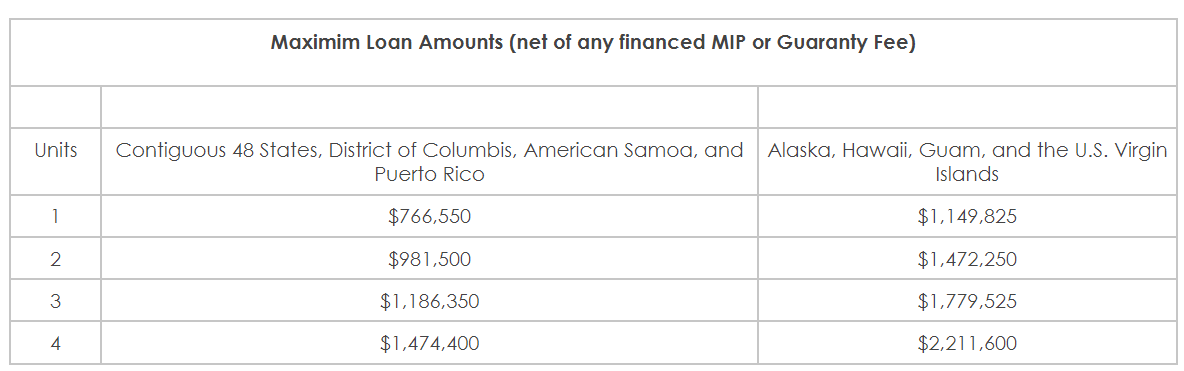

Under Ginnie Mae’s All Participants Memorandum (APM) 23-13, effective for pools or loan packages submitted on or after January 1, 2024, a “High Balance Loan” is defined as a single-family forward mortgage loan with an original principal balance (minus the amount of any up-front mortgage insurance premium) that exceeds the following limits:

High Balance Loans are eligible for Ginnie Mae mortgage-backed securities (MBS), subject to the restrictions detailed in Chapter 9, Part 2, § B and Ch. 24 Part 2, § A(1) of the Mortgage-Backed Securities Guide 5500.3, Rev-1.

Just yesterday, the FHFA announced the conforming loan limit values (CLLs) for mortgages that Fannie Mae and Freddie Mac will acquire in 2024. In most of the United States, the 2024 CLL value for one-unit properties will be $766,550, an increase of $40,350 from 2023.

The Housing and Economic Recovery Act of 2008 (HERA) requires that the FHFA to adjust the GSEs’ baseline CLL value each year to reflect the change in the average U.S. home price.

Under a series of laws enacted in past years, including the Economic Stimulus Act of 2008, the American Recovery and Reinvestment Act of 2009, Public Law 111-88, and Public Law 111-242, higher loan limit values have applied to GSE acquisitions of certain seasoned mortgages. Acquired loans originated between July 1, 2007, and September 30, 2011 are subject to previously announced limit values determined under those laws. The applicable CLL value for such seasoned loans is as high as $729,750 for one-unit properties in the contiguous U.S. In 2024, the baseline loan limit value will surpass the limit set for these seasoned loans, and the GSEs will no longer be required to select the higher of the two limit values to determine eligibility.

In October, Ginnie Mae announced that their MBS outstanding balance grew to $2.492 trillion, a number that includes $33.8 billion of total MBS issuance which has led to Ginnie Mae picking up $15 billion of net portfolio growth in a single month. October’s MBS supported the financing of nearly 110,000 households, of which 53,000 were first-time buyers. Nearly 75% of the October MBS issuance reflects new mortgages that support home purchases, as refi activity remained low due to higher interest rates.