The Federal Reserve’s plan to tame the housing frenzy with higher interest rates has a major blind spot: More than 40% of all U.S. mortgages—most of which are fixed-rate—were obtained in 2020 or 2021 when rates were at rock bottom.

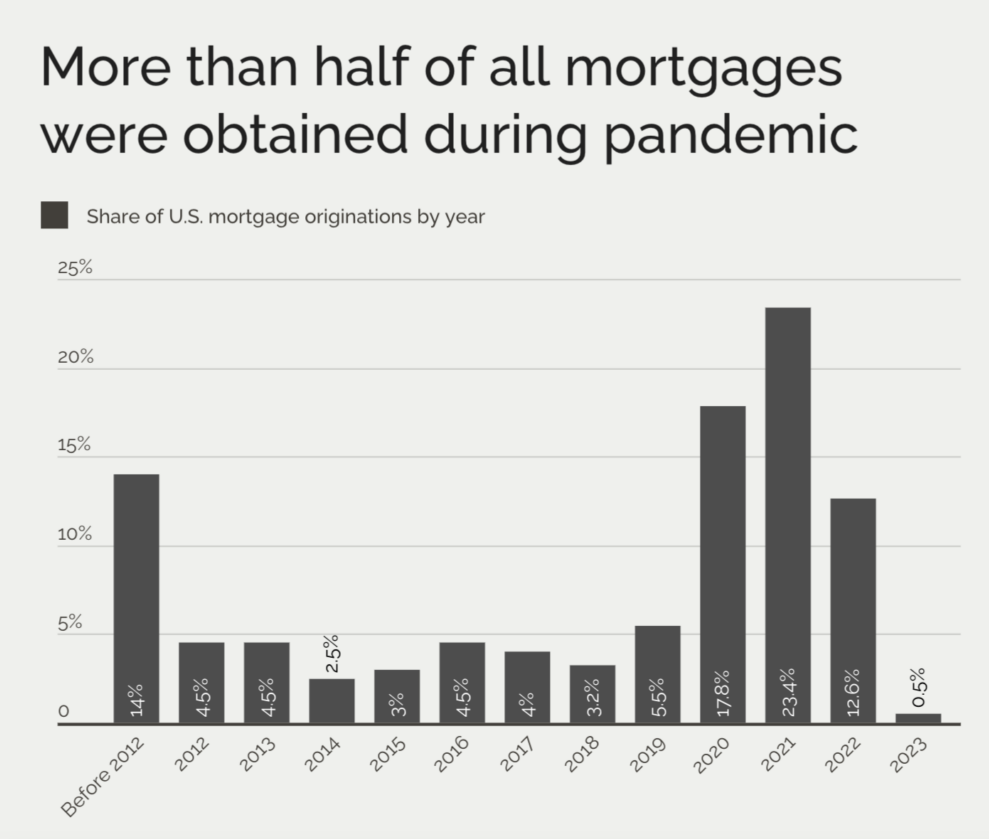

According to Creditnews research, about one-quarter (23.4%) of mortgages were originated in 2021 when the 30-year mortgage rate fell below 3%. Another 17.8% were originated in 2020—the year the Fed slashed interest rates to zero.

Nearly two-thirds (64.5%) of U.S. mortgages have rates below 4%, roughly half the current 30-year fixed rate.

Assuming a 10% down payment, the difference between financing an average home with a 30-year mortgage at 7.79% (mortgage rate peak as of Oct 26) and 3.6% (effective mortgage rate) is an extra $1,223 a month.

This discrepancy has created a feedback loop of limited inventory and growing prices, locking would-be buyers out of homeownership—especially those in the Millennial and Gen Z generations.

In 2023, Millennials made up only 28% of homebuyers despite being in the prime home-buying age. That’s just over half as much as it was in 2022 before rates took off. And at just 4%, Gen Zers made up the tiniest fraction of homebuyers.

Although Millennials are the largest adult generation in the United States, they still own a mere 10% of U.S. real estate wealth. They also accumulated the least real estate wealth during the pandemic housing boom.

“The Fed’s aggressive rate-hike campaign has worsened the generational homeownership divide. Unlike Baby Boomers who can afford to buy in cash, Millennials and Gen-Z buyers need financing. That’s been harder to get with mortgage rates at 22-year highs. Homebuyers aren’t getting any help from the market, either. Homeowners refuse to sell because they don’t want to trade their low mortgage rate for a much higher one. So, whatever housing supply makes it to market comes at disproportionally higher prices.” - Sam Bourgi, Senior Analyst at Creditnews.

Key Takeaways:

- More than 40% of all U.S. mortgages were obtained in 2020 or 2021 when rates were at rock bottom—and over half after 2020

- Mortgage originations during the pandemic eclipsed the previous peaks of the post-dot-com boom and the subprime mortgage bubble

- The 30-year fixed mortgage rate is now more than double the effective mortgage rate—the largest gap since 1976

- Meanwhile, 64.5% of U.S. homeowners are locked in with mortgages below 4%—these homeowners aren’t affected by rising interest rates unless they choose to refinance

- The monthly mortgage payment on an average home has spiked 54% between 2021 and 2023, leaving younger buyers unable to afford a home

- The majority of Millennials and Gen Zers missed the low-rate bandwagon, with buyers from these generations owning just a mere 10% of real estate wealth in the United States and accumulating the least wealth during the pandemic

Mortgage Rates and Originations

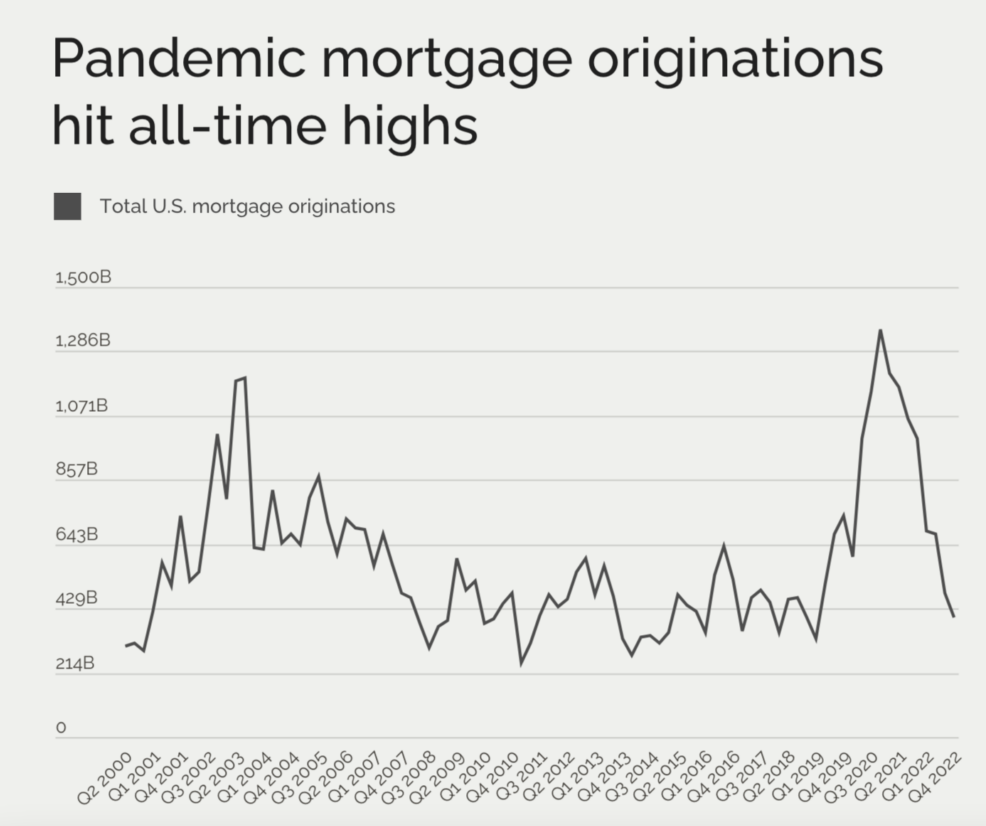

During the pandemic housing frenzy, mortgage origination hit levels never seen on record.

In 2021, the value of mortgage origination surpassed $4.4 trillion, a new all-time high. Originations fell to roughly half that level in 2022 but were still considerably higher than in the decade before the pandemic.

Among existing mortgages, over half of originations occurred between 2020 and 2022. This includes 17.8% in 2020, 23.4% in 2021, and 12.6% in 2022.

The data shows that mortgage originations accelerated in 2020 when the Fed reduced interest rates to zero in March of that year. They began to taper off in 2022 after the Fed began raising rates, also in March.

By comparison, the share of outstanding mortgages originated in 2019 was only 5.5%. In 2018, it was just 3.2%.

Mortgage originations during the pandemic eclipsed the previous peaks of the post dot-com boom and the subprime mortgage bubble.

Nearly two-thirds (64.5%) of existing mortgages have 30-year rates below 4%. The breakdown is as follows: 38.2% of mortgages have interest rates between 3%-3.99%, 25.8% have rates between 2%-2.99%, and 0.5% have rates below 2%.

Somewhat surprisingly, only 2.4% of existing mortgages have interest rates at 7% or higher —the current mortgage rate.

At current levels, the discrepancy between the current 30-year fixed mortgage rate (7.79%) and the effective mortgage rate (3.6%) is the widest since 1976.

Younger Generations Impacted the Most

Record-low mortgage rates between 2020 and early 2022 made home-buying more affordable for younger generations. In 2022, roughly 43% of new homebuyers were Millennials and 2% were Gen Zers.

However, as rates began to rise, Millennials’ share of new purchases fell to 28% as of August 2023. Gen Zers’ share of purchases doubled to 4% but remained relatively scant given the cohort’s size (70 million people).

Younger demographics also own a much smaller share of the real estate wealth, given the size of their respective generations. They also accumulated the least real estate wealth during the pandemic housing boom despite being in the prime home-buying age.

The total U.S. housing stock was worth a record $46.8 trillion in June 2023. However, Millennials’ share of that wealth was only $5 trillion, compared to $18 trillion for baby boomers and $13.4 trillion for Gen X.

Millennials’ housing wealth exceeded that of the Silent Generation, which owned $4.7 trillion worth of residential real estate. Gen Zs’ share of the housing wealth is likely much smaller than Millennials, given their share of purchases and mortgage originations.

Younger Generations Bear the Brunt of Record Mortgage Rates

“Tons of homeowners scored an incredible deal during the pandemic: a 3% mortgage rate for the remainder of their 30-year loan," said Chen Zhao, Redfin Economics Research Head. "Now they’re staying put because moving would mean taking on a rate that’s twice as high [...] The winners are homeowners who bought before mortgage rates started rising; they continue to build equity even though homebuyer demand has slowed. The losers, sadly, tend to be first-time buyers.”

To read the full report, including more data, charts, and methodology, click here.