As Americans continue to settle into the New Year, mortgage rates remain on many consumers' minds. While it's uncertain to know which direction the economy and housing market will sway in 2024, the Fannie Mae Home Purchase Sentiment Index (HPSI) increased 2.9 points in December to 67.2.

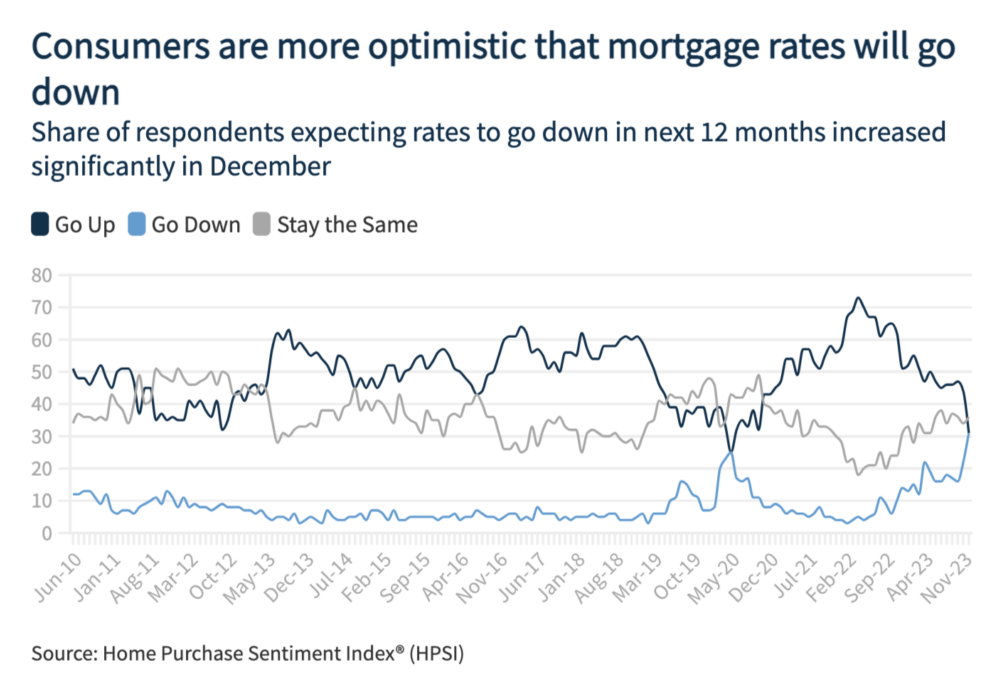

This was primarily due to a significant jump in the share of consumers that are expecting mortgage rates to go down over the next 12 months.

The report found that in December, a survey-high 31% of consumers indicated that they expect mortgage rates to go down, while an estimated 31% expect them to go up, and 36% expect rates to remain the same.

While consumer sentiment surrounding homebuying conditions remain "overwhelmingly pessimistic", the HPSI ticked up slightly month-over-month (MoM), with 17% of consumers now indicating it's a good time to buy a home, compared to 14% last month—a survey low.

The report revealed that overall, the full index is up 6.2 points year-over-year.

"Mortgage rate optimism increased dramatically this month, with a survey-high share of consumers anticipating mortgage rate declines over the next year," said Mark Palim, VP and Deputy Chief Economist at Fannie Mae. "This significant shift in consumer expectations comes on the heels of the recent bond market rally and an already-significant downtick in 30-year mortgage rates, from their high of nearly 8% in early November to 6.62% as of this past week. Notably, homeowners and higher-income groups reported greater rate optimism than renters; in fact, for the first time in our National Housing Survey's history, more homeowners, on net, believe mortgage rates will go down than go up."

Fannie Mae's Home Purchase Sentiment Index (HPSI) increased in December by 2.9 points to 67.2. The HPSI is up 6.2 points compared to the same time last year.

Home Purchase Sentiment Index: Component Highlights Per the Fannie Mae HSPI

- Good/Bad Time to Buy: The percentage of respondents who say it is a good time to buy a home increased from 14% to 17%, while the percentage who say it is a bad time to buy decreased from 85% to 83%. As a result, the net share of those who say it is a good time to buy increased by 5 percentage points MoM.

- Good/Bad Time to Sell: The percentage of respondents who say it is a good time to sell a home decreased from 60% to 57%, while the percentage who say it's a bad time to sell increased from 40% to 42%. As a result, the net share of those who say it is a good time to sell decreased by 5 percentage points MoM.

- Home Price Expectations: The percentage of respondents who said home prices would rise in the next 12 months decreased from 41% to 39%, while the percentage who said home prices would go down remained unchanged at 24%. The share of people who think home prices will stay the same increased from 35% to 36%. As a result, the net share of those who say home prices will go up in the next 12 months decreased by 2 percentage points MoM.

- Mortgage Rate Expectations: The percentage of respondents who say mortgage rates will go down in the next 12 months increased from 22% to 31%, while the percentage who expect mortgage rates to go up decreased from 44% to 31%. The share of people who think mortgage rates will stay the same increased from 34% to 36%. As a result, the net share of those who say mortgage rates will go down over the next 12 months increased by 22 percentage points MoM.

- Job Loss Concern: The percentage of respondents who say they are not concerned about losing their job in the next 12 months decreased from 76% to 75%, while the percentage who say they are concerned increased from 23% to 24%. As a result, the net share of those who say they are not concerned about losing their job decreased by 3 percentage points MoM.

- Household Income: The percentage of respondents who say their household income is significantly higher than it was 12 months ago increased from 19% to 20%, while the percentage of respondents who say their household income is significantly lower increased from 12% to 13%. The percentage of people who say their household income is about the same decreased from 68% to 67%. As a result, the net share of those who say their household income is significantly higher than it was 12 months ago remained unchanged MoM.

"A more optimistic rate outlook among consumers may signal an expectation that home affordability pressures will ease in 2024," said Palim. "Homeowners have told us repeatedly of late that high mortgage rates are the top reason why it's both a bad time to buy and sell a home, and so a more positive mortgage rate outlook may incent some to list their homes for sale, helping increase the supply of existing homes in the new year. Of course, that's likely dependent on the extent to which mortgage rate expectations are met with actual mortgage rate declines. Like many others, even if rates fall further, we continue to believe that affordability will be tempered in part by elevated home prices, especially for first-time homebuyers, and we expect the pace of home sales improvement to be modest in 2024."

To read the full release, click here.