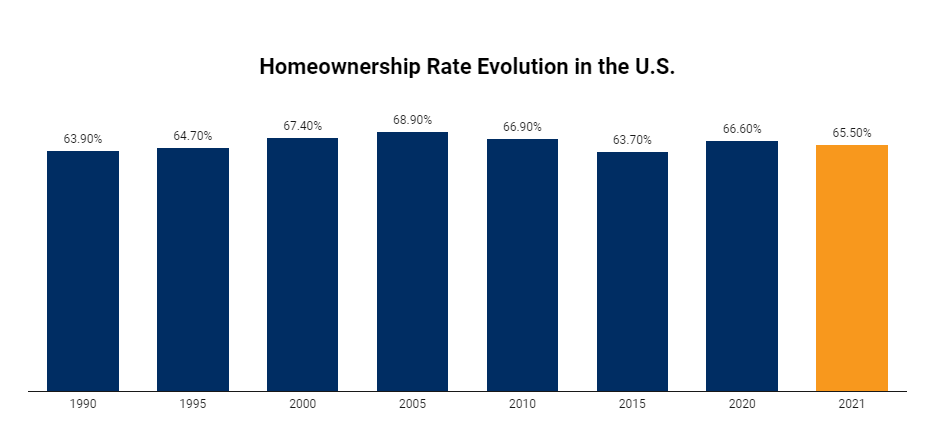

According to a new study from PropertyShark, the U.S. homeownership rate currently rests at 65.5%, while renter-occupied housing units make up 34.5% of the national stock. The U.S. homeownership rate represents the percentage of occupied housing units where the resident is also the owner. Economic factors, wage evolution, increasing home prices, lifestyle choices and generational preferences are all significant contributors to the changing landscape of housing.

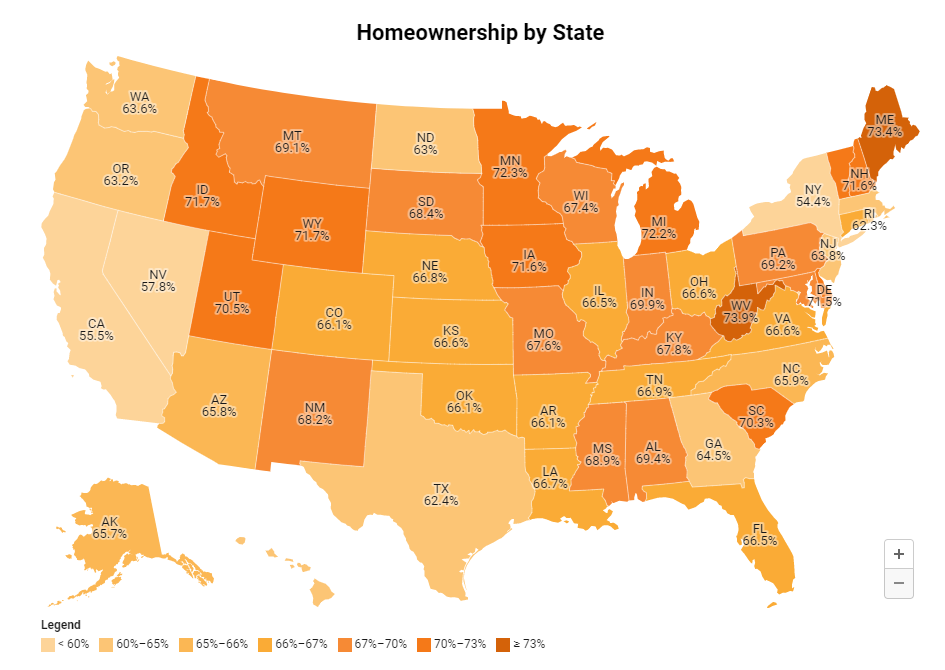

Homeownership stats can vary significantly from state to state, influenced by domestic migration trends, population density, stock, as well the economies, education opportunities and lifestyle trends of specific states. Drilling down to an even more detailed background, figures also noticeably vary when it comes to homeownership rates by city, with many of the most vibrant large urban centers experiencing declining homeownership stats.

Analyzing homeownership percentages in the U.S., coastal and southern states have seen a sharper decline compared to landlocked states over the past years, especially in states like New York or California, where the local population tends to be concentrated into urban centers. Conversely, states with lower population densities and home prices averaging below the national median tend to have higher homeownership rates.

Homeownership rates by city can widely vary even when located in close geographic proximity, depending on a wealth of factors from economic, employment and education opportunities to population density and migration, home prices and development pipelines among many others.

A wealth of factors influences the percentage of homeownership in the U.S., and at the state and city level, beyond the economy and home price trends. Education and employment opportunities, the climate; safety; population density; domestic migration trends; available housing stock; residential development pipeline; and generational preferences all influence the U.S. homeownership percentage.

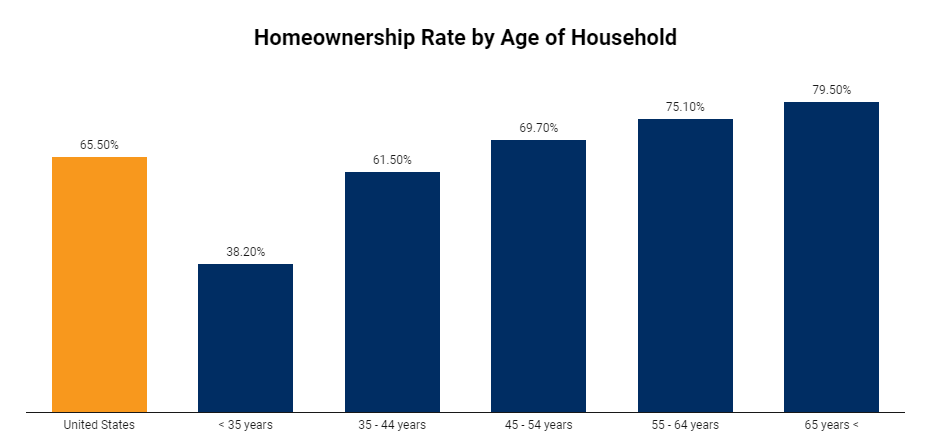

Homeownership by age and generation

It’s expected that the percentage of homeowners will increase by age and that older, more financially established generations would have higher homeownership rates than young adults just entering the job market.

Specifically, baby boomers make up the largest percentage of homeowners by generation and age, representing about two-thirds of owners. At the same time, only a third of millennials are owners, despite making up the bulk of would-be homebuyers, held back by rent costs, supply shortages – especially when it comes to starter homes – as well as disparities between wage growth trends and housing price increases.

Homeownership rate and home pricing

Population density and domestic migration trends are also major influencers of homeownership rates by state. Major influencers of noticeably lower homeownership rates in densely populated cities are high demand that often outpaces supply, higher land and development costs, and higher rent expenses, all of which contribute to higher home prices and lower homeownership rates.

Homeownership rate and property taxes

One factor that does not directly influence the U.S. homeownership percentage is property tax rates. Although some states with low property taxes do have a significantly higher rate of homeownership than those with high levels of taxation, there is no clear correlation between a state's level of property taxation and its homeownership rates.

For example, West Virginia features one of the lowest property tax rates in the U.S. at 0.58%, as well as the highest rate of homeownership of any state, with 73% of its residential real estate being owner-occupied. Alternatively, Vermont's 1.9% average rate is the fifth highest effective property tax rate in the U.S., but the state still has the fifth-highest homeownership rate in the country with 72% of its housing owner-occupied.

Although most non-institutional homeowners will occupy their home as a primary residence, some homeowners rent their properties out for an additional source of income. Additionally, some owners possess multiple properties that they use only sporadically or not at all. As a result, homes can be categorized as owner-occupied and owner-vacant.

Considering the abundance of factors that impact the U.S. rate of homeownership, figures have dipped and grown throughout the years, while economic factors continue to change landscape of housing.

To read the full report, including more data, charts and methodology, click here.