According to the first quarter Credit Industry Insights Report (CIRR) published by TransUnion, consumers are increasingly turning to credit to manage their budgets, leading to record- or near-record high balances in credit cards and unsecured loans.

According to the first quarter Credit Industry Insights Report (CIRR) published by TransUnion, consumers are increasingly turning to credit to manage their budgets, leading to record- or near-record high balances in credit cards and unsecured loans.

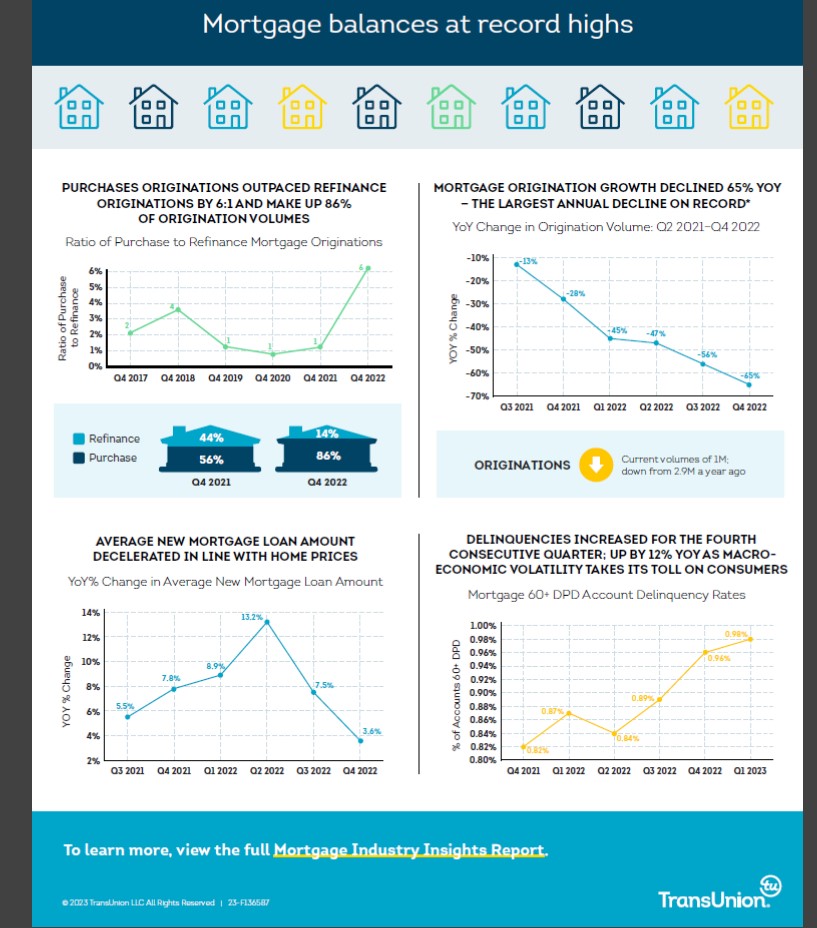

Mortgage balances reached a record level of $11.8 trillion during the first quarter of 2023; while a slowdown in mortgage activity continues to accelerate, down $2.9 million, representing a 65% year-over-year drop—the largest decline reported since TransUnion began tracking the statistic.

Within originations, purchases made up 86% of the volume in fourth quarter of 2022 with 900,000 originations (down by 45% year-over-year from 1.6M in the fourth quarter of 2021). Refinance originations fell by 89% year-over-year from 1.3M to 143,000, the lowest level to date.

This was driven by the dramatic decrease of rate and term refinances, which were down by 96% year-over-year from 588,000 in Q4 2021 to 24 000 in Q4 2022, and cash-out refinance originations, which were down by 83% year-over-year from 716,000 to 120,000. Conversely, Home equity line of credit originations were up 7% year-over-year to reach 299,000 in the fourth quarter of 2022, while home equity loan originations grew 31% year-over-year to 264,000.

Mortgage delinquencies ticked up year-over-year, with account-level delinquency (60+ days past due) growing 12% to 0.98% this quarter, though still remaining at very low levels historically.

“The relatively higher interest rate environment has depressed mortgage refinancing in particular. Interestingly, cash-out refinance hasn’t been as impacted as rate and term refinance,” according to Joe Mellman, SVP and Mortgage Business Leader at TransUnion. “This, coupled with the increases observed in HELOC and home equity loan originations, indicates that homeowners are still interested in tapping their home equity, even at higher interest rates. It is also encouraging that purchase originations remain near the lower end of the normal activity range, indicating that consumers are continuing to purchase homes even in this higher-rate environment.”

“While delinquency levels remain below historical norms, this marks the fourth consecutive quarter of increase– a trend worthy of continued monitoring in 2023 as macroeconomic volatility and increased cost-of-living may be starting to affect delinquencies,” Mellman concluded.

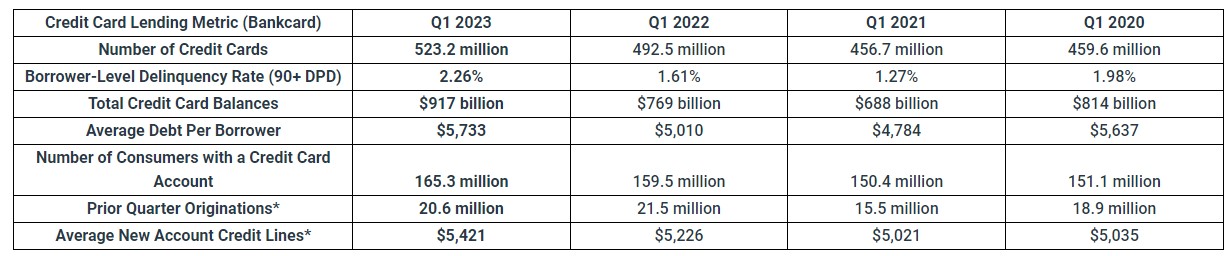

According to the report, credit card balances remained near record highs during the first quarter of 2023, coming in at $917 billion which represents a growth of 19.2% year-over-year. However, balances were down 1.5% quarter-over-quarter, a statistic that it typical this time of year, as many use their previous years’ tax returns to pay down debts.

The subprime share of consumers with outstanding balances declined to 10.2%, down from 10.9% from the fourth quarter of 2022, ending a trend of seven consecutive quarters of growth for the subprime market. On the other hand, “super prime tier” consumers increased their balances to 41.8% up form 40.6% from the last quarter.

In particular, millennials continued to see their share of balances grow to 28.6% compared to 26.5% year-over-year.

In total, credit lines increased 9.7% during the first quarter, up to $4.4 trillion, an increase of $391 billion year-over-year.

According to TransUnion high growth in credit lines was observed across the risk spectrum, but 60% of the increase was driven by super prime borrowers. Fourth quarter 2022 new account originations came in at 20.64 million accounts, representing a decline of -3.9% year-over-year and -4.3% quarter-over-quarter. Most of the impact was driven by a decline in subprime originations of -19% year-over-year. Bankcard 90+ DPD consumer-level delinquency remained flat quarter-over-quarter at 2.26% but remains up significantly from levels seen in the first quarter of 2022.

“Bankcard balances continued to grow as borrowers gained greater access to credit and subsequently leveraged that available credit. While bankcard originations were down slightly YoY and QoQ, they still topped 20 million for the fifth time over the course of the past six quarters. 90+ DPD delinquency rates by accounts were relatively flat among all risk tiers with the exception being subprime, which were at 12.42%, up from 9.44% a year ago,” said Paul Siegfried, SVP and Credit Card Business Leader at TransUnion.

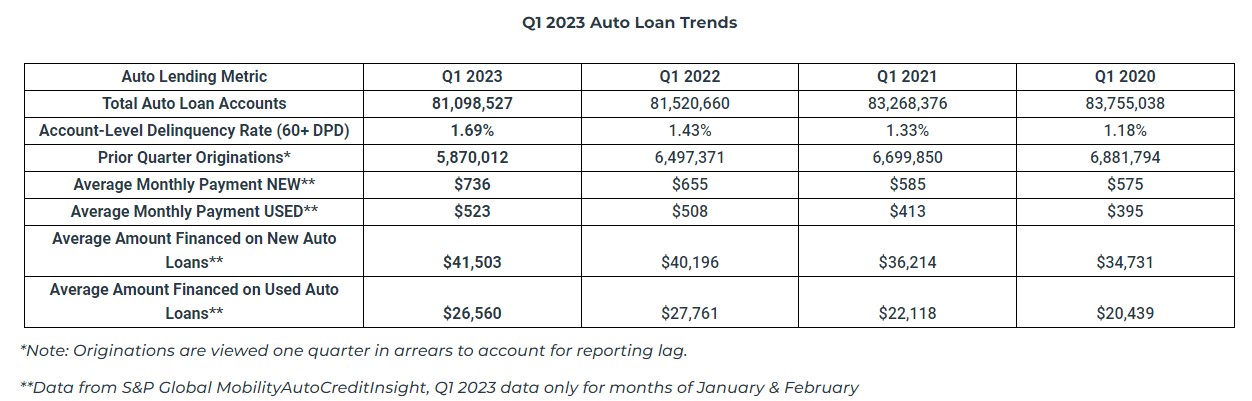

Finally, auto loans were down 9.7% year-over-year to 5.9 million. This is the lowest number recorded since the fourth quarter of 2013. As consumers are holding onto their cars longer due to the inflated used car market, originations were down across all risk tiers, with all tiers seeing decreases between 10% and 13%, with the exception of super prime consumers which only decreased 1%.

The new vs. used split remains steady, with used cars making up 60% of all car purchases in Q1 2023. Leasing continues to lag, only accounting for 18% of new vehicle registrations, down from 20% YoY. The average amount financed for new vehicles was up 3.4% YoY, while the average amount financed for used vehicles was down 2.6% YoY. Monthly payments were up YoY for both new cars (+11.9%) and used cars (+3.9%).

Satyan Merchant, SVP and Automotive Business Leader at TransUnion had this to say on the report:

“Driven by lower inventories and higher interest rates, originations remain down from the same quarter one year ago. However, as production begins to catch up to demand, there is hope that this trend will reverse course soon, at least among new cars. The used market is expected to remain tight, as the lower level of new car sales starting in 2020 means fewer recent model-year used cards available. Affordability remains a central issue for consumers, especially those below prime. We continue to pay close attention to delinquencies but continue to see positive signs among vintage data.”