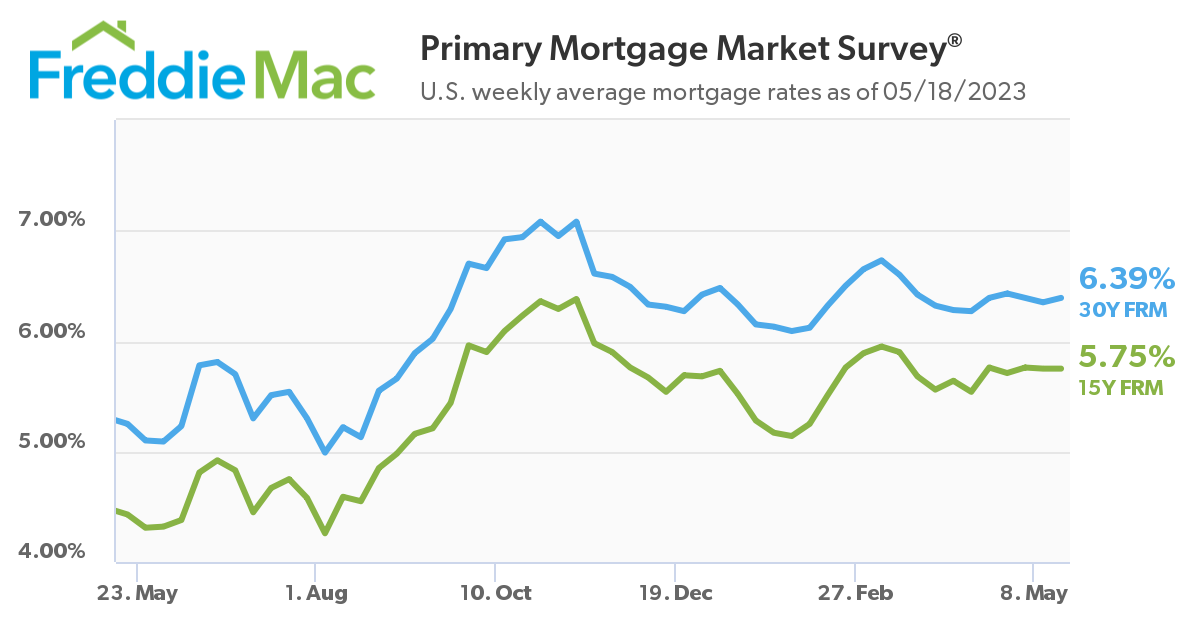

Freddie Mac, in its latest Primary Mortgage Market Survey (PMMS), has reported the 30-year fixed-rate mortgage (FRM) rising week-over-week, averaging 6.39% as of May 18, 2023, up from last week when it averaged 6.35%. A year ago at this time, the 30-year FRM averaged 5.25 percent.

Freddie Mac, in its latest Primary Mortgage Market Survey (PMMS), has reported the 30-year fixed-rate mortgage (FRM) rising week-over-week, averaging 6.39% as of May 18, 2023, up from last week when it averaged 6.35%. A year ago at this time, the 30-year FRM averaged 5.25 percent.

This week’s rise was a change in pace as the FRM had fallen the previous two weeks.

“The 30-year fixed-rate mortgage averaged 6.39% this week, as economic crosscurrents have kept rates within a 10-basis point range over the last several weeks,” said Sam Khater, Freddie Mac’s Chief Economist. “After the substantial slowdown in growth last fall, home prices stabilized during the winter, and began to modestly rise over the last few months. This indicates that while affordability remains a hurdle, homebuyers are getting used to current rates and continue to pursue homeownership.”

Also this week, the 15-year FRM averaged 5.75%, unchanged from last week. A year ago at this time, the 15-year FRM averaged 4.43%.

“Mortgage rates increased to the highest level in two months, which put a damper on borrower demand last week,” said Mortgage Bankers Association (MBA) President and CEO Bob Broeksmit. “Higher rates and low inventory levels continue to keep many prospective first-time buyers on the sidelines. Purchase applications for FHA loans–popular with many first-timers–were down 5% from last week, and 17% from a year ago.”

The uptick in rates brought with it a dip in overall mortgage application volume, as the MBA reported that volume fell 5.7% week-over-week, according to its Weekly Mortgage Applications Survey. The MBA’s Refinance Index decreased 8% from the previous week, and was 43% lower than the same week one year ago, while the seasonally adjusted Purchase Index fell 4.8% from one week earlier. The unadjusted Purchase Index decreased 5% compared with the previous week, and was 26% lower than the same week one year ago.

“Buyer demand has been sensitive to the ebb and flow of mortgage rates, but near-peak home prices and elevated inflation mean many would-be buyers are still waiting on the sidelines,” noted Realtor.com Economic Data Analyst Hannah Jones. “Mortgage rates have bounced within a tight range since September 2022, as the Fed’s actions to slow the economy and stubborn inflation have made the future relatively cloudy. Recent data shows signs of a stubborn, though slowing economy, suggesting that the Fed’s contractionary actions are having the intended effect. However, inflation remains well above the target level, and unemployment remains near all-time lows. The economy remains on fragile footing, and a U.S. default would cause an interest rate spike that could erase any progress towards a healthier housing market by cutting deeper into home sales. Though a default remains unlikely, the closer we get to a possible event date without an increase in the debt limit, the more likely households will be affected by higher interest rates. The sooner the debt impasse is resolved, the less likely it is to negatively affect households already plagued by high prices.”

The National Association of Home Builders (NAHB) reports that the limited amount of existing inventory has injected life into new home construction, resulting in strong gains in builder confidence in May, despite continued challenges in the availability of raw materials, supply chain disruptions, and tightening credit conditions for new constructions loans.

“Lack of existing inventory continues to drive buyers to new construction,” said NAHB Chief Economist Robert Dietz. “In March, 33% of homes listed for sale were new homes in various stages of construction. That share from 2000-2019 was a 12.7% average. With limited available housing inventory, new construction will continue to be a significant part of prospective buyers’ search in the quarters ahead.”

Affordability continues to be a hurdle for many as home price increases trend upward, as the National Association of Realtors (NAR) latest quarterly report found that seven out of 10 metropolitan markets registered home price gains in Q1 of 2023. Seven percent of the 221 metros tracked by NAR registered double-digit price increases, but that number fell from 18% from Q4 of 2022.

“Home shoppers continue to face low home inventory, high prices, and elevated mortgage rates, leaving many discouraged in their search,” said Jones. “Many potential sellers feel ‘locked in’ by their current low mortgage rate, and are hesitant to enter into a market that would require taking on a higher rate to buy a new home. Constrained buyers and reluctant sellers mean the spring market hasn’t picked up as much momentum as in years past, but each improvement in affordability is met with an increase in buyer activity. However, increased buyer activity has not been met with increased seller activity, and in many markets, buyers are competing for the few fresh listings available. Prices are likely to remain elevated in many markets where low inventory, especially at an affordable price point, is creating a competitive environment.”