A new release from the Federal Housing Finance Agency (FHFA) revealed that in June 2021, the Federal Interagency Task Force on Property Appraisal and Valuation Equity (PAVE) was created to develop strategies to identify and eliminate racial and ethnic bias in home valuations.

On March 23, 2022, Task Force members released the PAVE Action Plan to advance property appraisal and valuation equity.

On October 24, 2022, the FHFA released Uniform Appraisal Dataset (UAD) Aggregate Statistics with information on property appraisal statistics at the national, metropolitan area, state, county, and neighborhood levels.

Since June 2021, multiple other actions taken by stakeholders and federal, state, and local agencies have increased awareness of racial bias in home valuations and have increased enforcement of prohibitions on discriminatory appraisals.

On June 29, 2023, FHFA released its fourth quarterly UAD Aggregate Statistics, including a new “Appraisal Gap” dashboard highlighting potential bias in appraisals. In this blog, we use a subset of the data to explore changes in property appraisal statistics in white and minority neighborhoods.

To study whether the appraisal valuation outcomes between white tracts and two minority tract categories have changed over time, the FHFA divided the quarterly data into two time periods:

- Phase 1: Appraisals conducted prior to the second quarter of 2021, before the creation of the Interagency PAVE Task Force in June 2021.

- Phase 2: Appraisals conducted following the first quarter of 2022, after the release of the Action Plan in March 2022.

Of the 25.9 million appraisals for purchase properties in the UAD Aggregate Statistics from 2013 Q1 through 2023 Q1, 21.1 million (81%) occurred in Phase 1, and 2.4 million (8%) occurred in Phase 2.

Appraisal Gap

Appraisal valuation can be at, above, or below contract price based on the appraiser’s opinion of value for the property. However, unlike appraisals that are at or above the contract price, low appraisals can delay or even derail the closing of the sale. For instance, a homebuyer can back out of the contract if the purchase agreement has an appraisal clause.

A low appraisal may limit the amount a lender is willing to finance, which may require the seller and/or the buyer to cover the shortfall. The seller may have to cover at least part of the shortfall through reducing the contract price.

From Q1 2013 through Q1 2023, nearly 26% of the appraisal valuation was equal to the contract price, 9.2% of appraisals were below the contract price (low appraisals), and 64.7% were above the contract price. The percentage of both the low and the high appraisals increased in Phase 2 as compared to Phase 1.

While the percentage of low appraisals is in single digits across all census tracts, the FHFA presented the percentage of low appraisals by the three tract categories for three different time periods.

From Q1 2013 through Q1 2023, the percentage of low appraisals was 8.1% for properties in white tracts as compared to 13.4 percent in minority tracts and 16.5% in high minority tracts.

The more than double the percentage of low appraisals in high minority tracts as compared to white tracts is a signal of potential racial and ethnic bias in home valuations. Because we know that there is some anchoring effect for appraised values at or near the contract price, appraisal gap makes for a stronger inference of bias in both the raw statistic and when controlling for explanatory factors.

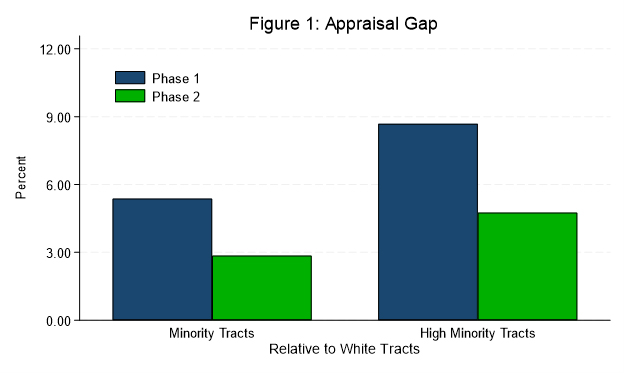

The overall percentage of low appraisals was 7.4% in white tracts, 12.8% in minority tracts, and 16.1% in the high minority tracts. Thus, the appraisal gap between white and minority tracts in Phase 1 was 5.4 percentage points. The appraisal gap between white and high minority tracts was 8.7 percentage points.

While the percentage of low appraisals is still higher for minority and high minority tracts as compared to white tracts, the appraisal gap narrowed because of an increase in the percentage of low appraisals in white tracts and a subsequent decline in the percentage of low appraisals in minority tracts.

The appraisal gap between white and minority tracts dropped to 2.9 percentage points while the appraisal gap between white and high minority tracts dropped to 4.8 percentage points.

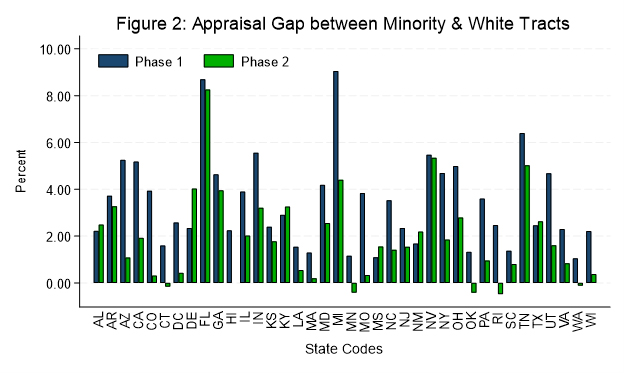

At the state level, the appraisal gap between minority and white tracts declined in nearly all states in Phase 2 as compared to Phase 1.

In six states—Alabama, Delaware, Kentucky, Mississippi, New Mexico, and Texas—the appraisal gap between minority and white tracts increased in Phase 2.

In five states—Connecticut, Minnesota, Oklahoma, Rhode Island, and Washington—the percentage of low appraisals in minority tracts was lower than the percentage of low appraisals in white tracts in Phase 2.

In all other states, minority tracts continued to have a higher percentage of low appraisals as compared to white tracts but the gap narrowed substantially.

To read the full report, including more data, charts, and methodology, click here.