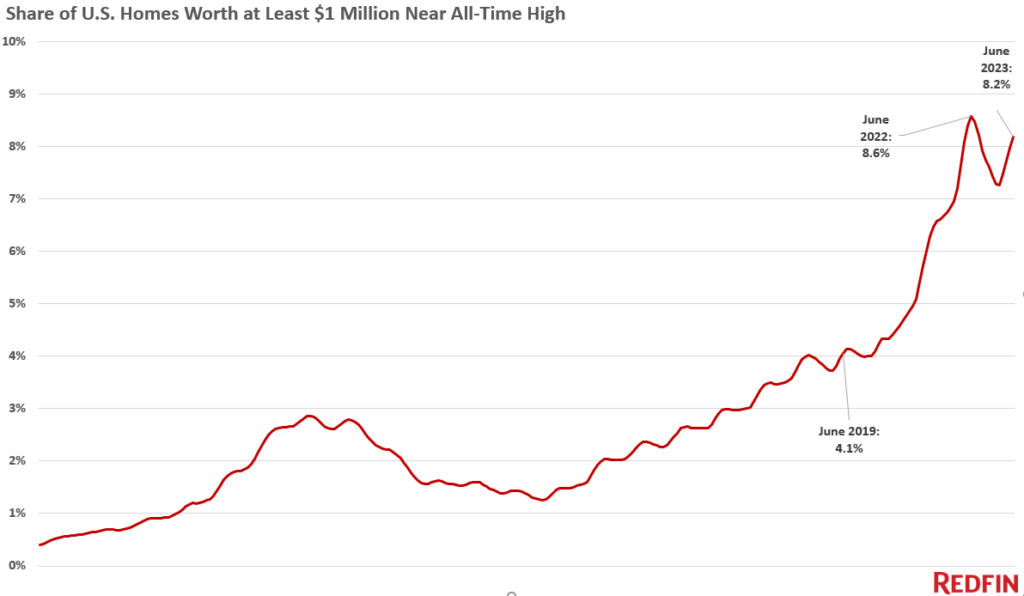

According to a new report from Redfin, just 8% of single-family homes throughout the country are worth more than $1 million, a number which has retreated from an all-time high of 8.6% from just over a year ago.

According to a new report from Redfin, just 8% of single-family homes throughout the country are worth more than $1 million, a number which has retreated from an all-time high of 8.6% from just over a year ago.

However, the share of homes that are worth more than $1 million is climbing after dipping to a 12-month low of 7.3% in February 2023. That’s because home prices are rising on a year-over-year basis after falling at the beginning of the year. The median U.S. home-sale price rose 3% in July, the biggest increase since last November. Prices are rising faster for high-end homes, with the median sale price of U.S. luxury homes up 4.6% year over year to $1.2 million in the second quarter.

The elevated mortgage rates seen at the moment are discouraging home sellers creating a “lock-in effect” that has limited inventory so severely that the few homes on the market are actually appreciating in value because of the demand from some people. That’s driving home prices up and pushing many of those on the cusp above the million-dollar mark.

“The supply shortage is making many listings feel hot,” said Redfin Economics Research Lead Chen Zhao. “In most of the country, expensive properties that are in good condition and priced fairly are attracting buyers and in some cases bidding wars, mostly because for-sale signs are few and far between right now.”

“Still, there’s no rush to offload high-value homes,” Zhao continued. “Recent economic signals that the U.S. may avoid a broad recession could cause high-end buyers to feel more confident in making a major purchase in the coming months. There may be more demand coming down the pipeline.”

In fact, the number of homes that cross the $1 million mark has doubled since the pandemic, coming up from 4% in June 2019. The share has shot up because home prices skyrocketed in 2020 and 2021 as record-low mortgage rates and remote work drove Americans to buy homes.

By the numbers, East Coast homes—particularly New England—are crossing the $1 million mark the fastest. Just over one-quarter (25.8%) of homes in the Bridgeport, Connecticut metro—which is made up of many popular New York City suburbs—are worth at least $1 million, up from 23.1% a year ago, the biggest increase of the metros in this analysis. It’s followed by Boston, where the share increased from 20.3% to 21.5%, and Newark, New Jersey (8.7% to 9.7%).

In 55 of the 99 most populous metropolitan areas, the portion of homes worth $1 million or more is up year-over-year, but the percentage of growth in these cities are relatively small at less than one percentage point. The portion of million-dollar-plus homes is unchanged in three metros and down in the remaining 41.

The West Coast is seeing the fastest loss of $1 million or more homes. The share dropped from 39.3% to 33% over the last year in Seattle, the biggest decline of the metros in this analysis. It’s followed by Oakland, California (55.1% to 49%) and Oxnard, California (40.2% to 34.5%). Los Angeles, San Diego, San Jose, San Francisco, Anaheim, New York and Washington, D.C. are also among the metros where the share fell.

The West Coast is losing high-valued homes the fastest because those markets have cooled more than others. Rising mortgage rates and the faltering tech economy deterred homebuyers in many of those places over the last year, though they are now starting to bounce back as buyers get used to elevated rates and the economy smooths out.

Still, California has the highest share of million-dollar-plus homes in the country by a steep margin. First is San Francisco, where 81.2% of homes are worth at least $1 million, down from 84.2% a year earlier. It’s followed closely by San Jose (79.6%, down from 82.9%). Next come Anaheim, Oakland, San Diego and Los Angeles, all places where the share of seven-figure homes has fallen a bit over the last year, but where roughly 40% to 50% of all are still worth at least $1 million.

Click here to see the report in its entirety.