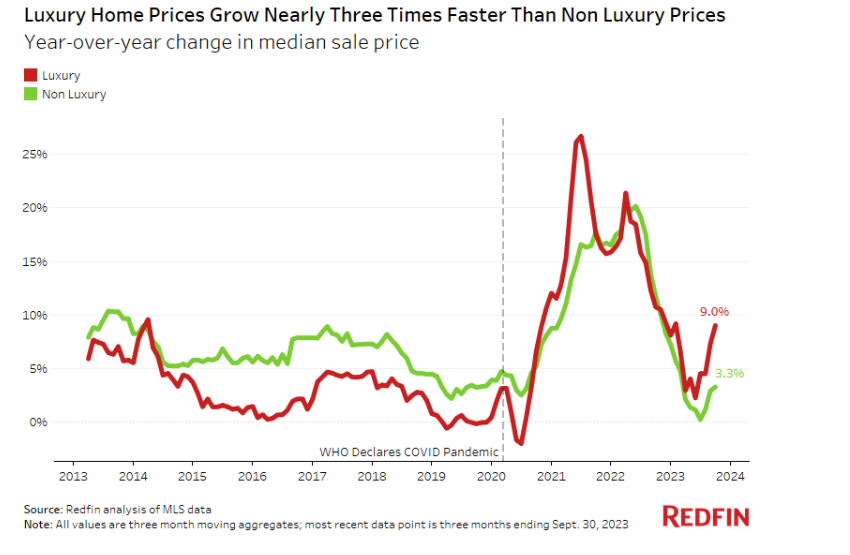

Redfin reports that the median sale price of luxury U.S. homes rose 9% year-over-year to $1.1 million in Q3, while the median sale price of non-luxury homes climbed 3.3% to $340,000, both at the highest level of any third quarter on record.

Redfin reports that the median sale price of luxury U.S. homes rose 9% year-over-year to $1.1 million in Q3, while the median sale price of non-luxury homes climbed 3.3% to $340,000, both at the highest level of any third quarter on record.

Redfin defines luxury homes as those estimated to be in the top 5% of their respective metro area based on market value, and non-luxury homes as those estimated to be in the 35th-65th percentile based on market value.

“Wealthy homebuyers have more tools to weather the storm of high mortgage rates,” said Redfin SVP of Real Estate Operations Jason Aleem. “Many of them can afford to pay in cash, meaning they’re escaping high mortgage rates altogether. Others are choosing to take on a higher rate and refinance later—an expensive option that isn’t feasible for a lot of lower-income consumers. Affluent Americans are still spending big, in large part because of pandemic savings and resilient housing and stock values.”

More than two in five (42.5%) luxury homes that sold in Q3 were purchased with cash, up from just over one-third (34.6%) a year earlier. By comparison, just 28% of non-luxury homes that sold were bought in cash, little changed from Q3 of 2022.

“While many luxury buyers have the resources to forge ahead even when mortgage rates are elevated, stubbornly high rates and home prices will likely push some affluent house hunters to the sidelines in the coming months,” said Redfin Chief Economist Daryl Fairweather. “High costs, along with the uptick in the number of high-end homes for sale, could cause luxury price growth to cool."

In terms of inventory, the total supply of luxury homes for sale (active listings) grew 2.9% from a year earlier in Q3, compared with a record 20.8% decline in the supply of non-luxury homes.

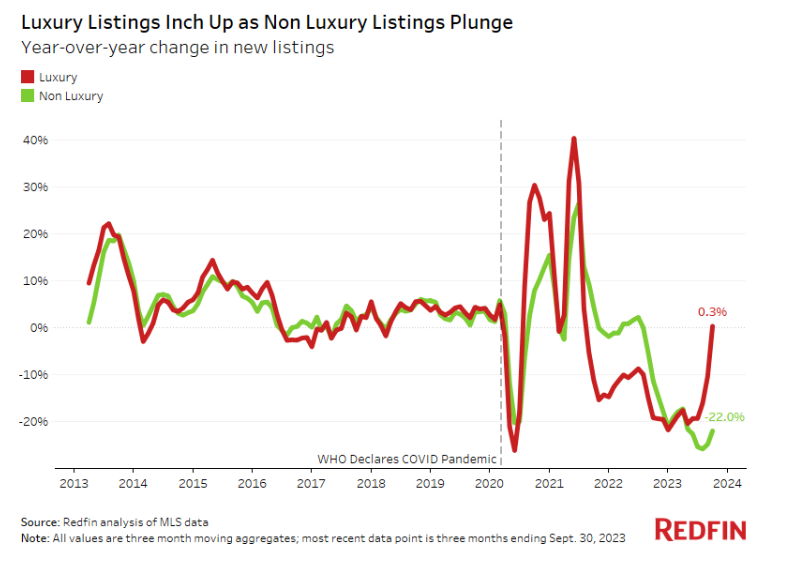

New listings of luxury homes rose 0.3%, while non-luxury new listings fell 22%. Luxury new listings were below pre-pandemic levels, but not by much. Non luxury new listings stood at the lowest third-quarter level since 2012. One reason luxury listings have held up relatively well is because high-end homeowners are less likely to feel locked into their low mortgage rate, either because they don’t have a mortgage at all, or they have the means to move and take on a higher rate.

Another reason that luxury listings are outperforming is an increase in homebuilding. Newly-built homes tend to be more expensive, meaning they often fall into the luxury tier.

Luxury home sales declined 10.6% year-over-year in Q3, compared to a 17% drop in non-luxury sales. Home sales are still falling from a year ago across the board because mortgage rates have climbed so much. Freddie Mac reported in its latest Primary Mortgage Market Survey (PMMS) that the 30-year fixed rate mortgage (FRM) slid three basis points week-over-week, dipping three basis points to 7.76% week-over-week. But the declines have eased—especially for luxury sales. That said, both luxury and non-luxury home sales were at the lowest Q3 levels since 2014.

While luxury home sales were down from a year earlier in most areas, 14 major U.S. metropolitan areas saw increases. In Tampa, luxury sales surged 35.8% year-over-year in the third quarter—the largest increase in the country. Next came Las Vegas (33.4%); Austin, Texas (14.5%); Sacramento, California (10.1%); and San Francisco (9.6%).

“It’s an opportune time to be a cash buyer, and there are a lot of cash buyers in Florida,” said Redfin Tampa Sales Manager Eric Auciello. “We’re still seeing many affluent house hunters move in from the Northeast and West Coast because they want lower taxes, different politics and/or to be closer to family. Tampa also has a ton of new construction, a lot of which is high-end condos.”

Regionally, luxury new listings in Tampa rose 13.9% year-over-year in Q3, a larger increase than every metro but New York. Rising flood insurance costs are likely another reason Tampa’s luxury market is outperforming its non-luxury market, Auciello said. Cash buyers aren’t required to purchase flood insurance. And for luxury buyers who do take out mortgages, their high-end homes are often elevated further above the ocean and built more resiliently, which often makes them easier to insure. Additionally, affluent buyers are more likely to be able to afford rising insurance premiums.

Redfin’s metro-level data includes the 50 most populous U.S. metropolitan areas, with the exception of Houston, which the company removed due to a data issue. All of the changes below are year-over-year changes:

- Prices: The median sale price of luxury homes rose most in New Brunswick, New Jersey (15.3%); Virginia Beach, Virginia (11%); and Baltimore (8.7%). Prices fell the most in Austin, Texas (-8.8%); Oakland, California (-6%); and Seattle (-4.6%).

- Supply: Active listings of luxury homes rose most in Austin, Texas (46%); San Antonio, Texas (25.6%); and Nashville (22.9%). They fell most in Cincinnati (-19.4%); Chicago (-18.3%); and Newark, New Jersey (-16.6%).

- New listings: New listings of luxury homes rose most in New York (17.1%); Tampa, Florida (13.9%); and San Antonio, Texas (12.7%). They fell the most in Atlanta (-19.8%); Newark, New Jersey (-18.4%); and Chicago (-17.2%).

- Home sales: Luxury home sales rose the most in Tampa (35.8%); Las Vegas (33.4%); and Austin, Texas (14.5%). They fell the most in New York (-33.5%); Philadelphia (-23.2%); and Baltimore (-23%).

Click here for more data from Redfin’s analysis of the nation’s luxury home sales marketplace.