As prices stray further from what qualifies as someone’s “within budget," a new Point2 study revealed that house buying power is diminishing for aspiring homeowners who find home prices—and sizes—far exceeding their income. The harsh reality is that last year’s income would have bought more for less.

So, how much can Americans afford to spend on a home anymore?

Compared to last year, the average 2023 home seeker in the U.S. could afford to spend about $3,100 less on a home. Although not encouraging, it’s a drop in the ocean compared to the year-over-year $96,800 loss in buying power that they experienced last year.

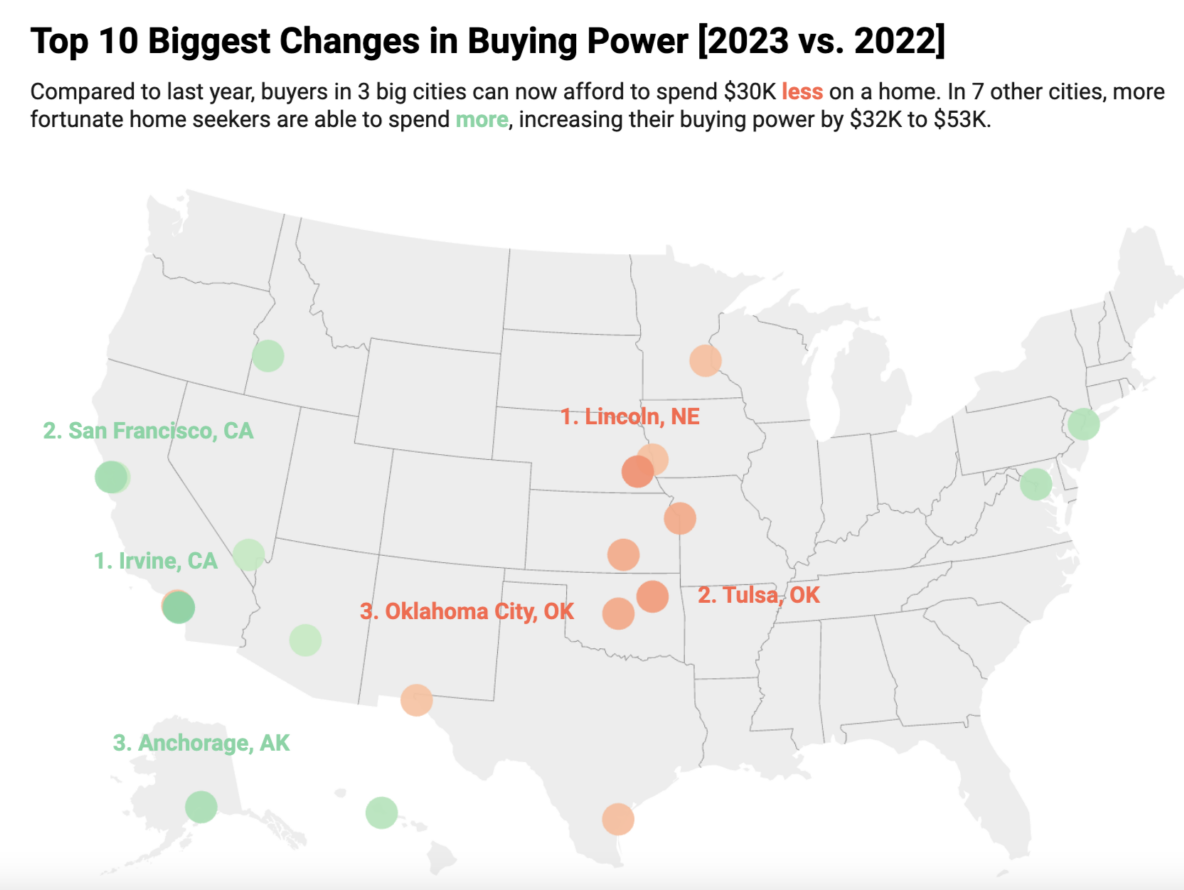

Buyers in Lincoln, NE, Oklahoma City, and Tulsa, OK, lost more than $30,700 of their budget for a home. Following the latest rate increase, those in nine other cities could afford $20,000 to $30,000 less than what they could in 2022.

But buying power is not the only thing that aspiring homeowners lost, as homebuyers in 61 large cities now afford less living space than they did last year. Home seekers in Detroit, MI, Tulsa, OK, and Wichita, KS, lost the most—more than 300 square feet.

With the average size of a bedroom in the U.S. around 132 square feet, some of these drops in space represent the equivalent of 1, 2, or almost 3 bedrooms.

The property ladder is less shaky in cities that experienced gains in buying power: homebuyers in seven large cities—including in Irvine, CA, San Francisco, Anchorage, AK, and Washington, D.C.—could afford to spend $30,000 more than last year.

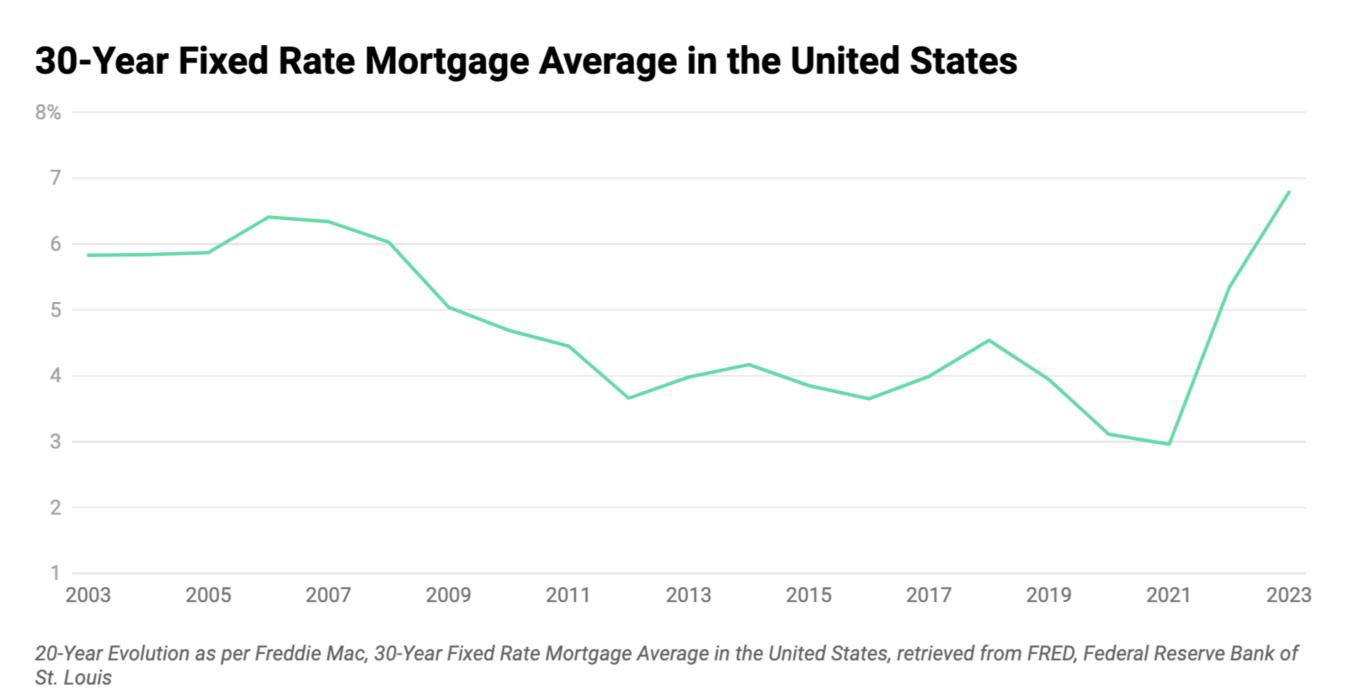

The uphill battle with mortgage rates was experienced across the nation. Fixed mortgage rates climbed from around 3% at the end of 2021 to 7% at the end of last year to about 7.5% as of this November—the highest levels in 20 years. Last year’s dramatic uptick prompted Point2 to analyze its impact on affordability and the average living space that comes with it, with equally dramatic results. While yearly changes this time around are not as harsh, things are far from ideal for the median-income homebuyer in 2023—a year defined by drastic measures to fight inflation.

Back in 2022, the average American with a $74,800 median income was able to afford a $278,200 home.

Although the median income in the United States has increased to nearly $78,200 this year, the average homebuyer can now afford to spend even less on a home. More precisely, aspiring homeowners would be able to buy a $275,000 property in 2023, meaning exploding interest rates and dragging incomes that can't keep up have lost potential homeowners more than $3,100 in buying power.

What’s worse, with the national median sale price at $412,000, this hypothetical $275,000 home that buyers could actually afford has become a unicorn in the U.S. housing market.

Cities with the Most Affordable Home Prices in 2023:

- Detroit: $111,750

- Cleveland: $114,728

- Buffalo, NY: $148,077

- El Paso, TX: $156,600

- Toledo, OH: $156,971

- Milwaukee: $157,674

- Cincinnati: $161,006

- Tulsa, OK: $168,061

- Newark, NJ: $169,040

- Memphis, TN: $174,862

Cities with the Least Affordable Home Prices in 2023:

- Fremont, CA: $654,821

- San Francisco: $559,144

- San Jose, CA: $539,156

- Arlington, VA: $523,711

- Irvine, CA: $498,161

- Gilbert, AZ: $458,121

- Seattle: $454,332

- Washington, D.C.: $421,394

- Scottsdale, AZ: $412,210

- Chandler, AZ: $403,794

Mortgage Rates Surge, Causing Buying Power Shifts Among the U.S.' Largest Cities

In just one year, home seekers in Lincoln, NE, Oklahoma City, and Tulsa, OK, lost more than $30,700, whereas they gained more than $42,000 in Irvine and San Francisco, CA.

Back in 2022, homebuyers in about half of the country’s 100 largest cities were crippled by losses of more than $100,000 in buying power compared to a year prior. This year, the differences in affordable home prices are not as significant as they were in that post-pandemic period. However, the affordability crisis is highlighted by the fact that the median home price in the U.S. is now 50% higher than the affordable home price. What’s more, the share of homes that fall under this “affordable” category makes up less than 28% of the national for-sale inventory.

Notably, in many large urban centers, the median home price is twice what the average buyer can afford. The outlook is harsher for those looking to buy a home in Los Angeles or New York City, where the median home prices are more than 200% higher than what they could afford without being financially burdened.

In light of mortgage rate hikes and increased prices, the very concept of affordability slips further and further away. And nowhere have home seekers lost more money than in the capital city of Nebraska. On a median income of $65,261, homebuyers in Lincoln could afford to spend only $191,053 on a home.

For comparison, one year ago, they could’ve afforded a more expensive $229,706 property on a smaller, $62,391 median income. This has led to a disappointing $38,650 loss in buying power in just one year.

To read the full report, including more data, charts, and methodology, click here.