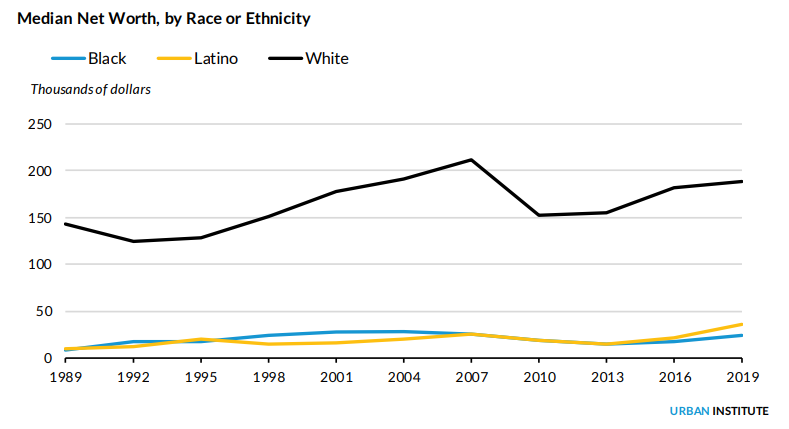

Efforts to close the persistent and detrimental Black-white homeownership gap, which is currently at 30 percentage points, must include not only measures to decrease the barriers to Black homeownership opportunity, but also mechanisms to ensure that homeownership is sustainable once achieved.

Mortgage reserve accounts are among the innovative solutions that could help homeowners overcome temporary hardships and get back on track with their mortgage payments, instead of falling into foreclosure, according to a new report from the Federal Home Loan Bank of San Francisco (FHLBank San Francisco) and the Urban Institute.

The new comprehensive report from the Racial Equity Accelerator for Homeownership examines a variety of new product structures aimed at supporting homeowners who experience temporary financial hardship, with a particular focus on how mortgage reserve accounts could help homeowners avoid default. This solution would disproportionately benefit Black families, who are more than twice as likely as white families to lose their home to foreclosure.

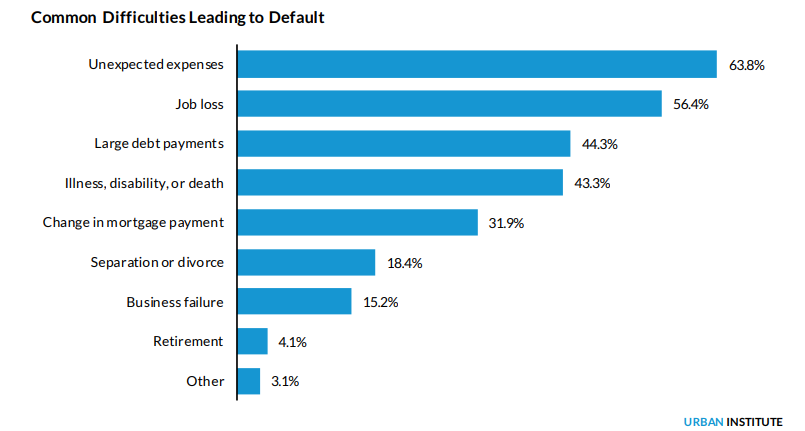

Recent research indicates that the greatest number of defaults are caused by shocks such as unexpected expenses (64%); job loss (56%); large debt payments (44%); or illness, disability, or death (43%); and that Black homeowners are more vulnerable to all these shocks due to their generally lower levels of liquid assets, more precarious employment, larger debt-to-income ratios, greater medical debt, and higher cost of homeownership.

The long history of reduced access to wealth-building opportunities, that Black households have experienced means they have less financial cushion to fall back on in the event of a financial shock; in contrast, the typical white family has eight times the wealth of the typical Black family.

“Efforts to promote Black homeownership and narrow the Black-white wealth gap are undermined when homeownership is not sustained,” said Janneke Ratcliffe, VP of the Housing Finance Policy Center at the Urban Institute. “For this reason, we need to redouble our efforts to develop effective ways to give homeowners breathing room so that a financial rough patch does not lead to losing a home.”

“The housing finance industry has created a robust foreclosure prevention toolkit over the past 15 years, but there’s still significant room for improvement, and we need to pursue multiple new avenues to reduce the risk of default. These financial tools, designed to help families keep their homes and build generational wealth, would also make mortgages less risky for lenders, insurers, and investors,” said Teresa Bryce Bazemore, President and CEO of FHLBank San Francisco. “Our joint research with the Urban Institute has identified a number of promising ways to help close the racial gap in homeownership and wealth building. This latest report highlights the potential of mortgage reserve accounts, and we welcome the opportunity to further explore this type of solution.”

The report, Using Mortgage Reserves to Advance Black Homeownership, explores solutions that have been proposed or could be enhanced to sustain homeownership, particularly in addressing shocks that hit Black homeowners harder than others. These solutions, which range from tried-and-tested approaches to still-undeveloped ideas, fall into three broad categories: enhanced foreclosure prevention (e.g., forbearance programs, loan modification), insurance (e.g., mortgage protection insurance, home warranty insurance, mortgage insurance that protects the borrower rather than the lender, a borrowers mutual insurance fund), and dedicated reserve accounts.

While all these tools have potential and many could work together, this report focuses on the mortgage reserve account, a savings account tied to an individual mortgage and funded by reducing the down payment. If borrowers experience an income shock or an unexpected expense, they typically use the account to cover mortgage payments.

Several mortgage reserve models have been developed and tested, some of which—such as the Prosperity Now pilot program and the Self-Help credit union network’s Savings Account for Emergencies program—include matched savings to encourage participation. Mortgage reserve account programs are also being explored as part of the Equitable Housing Finance Plans. Research suggests that such accounts mitigate foreclosures by providing emergency savings for borrowers to draw on if needed.

The authors of Using Mortgage Reserves to Advance Black Homeownership analyze default rates and loss severities on loans and determine that reserves improve performance, even on mortgages with higher loan-to-value ratios, and reduce overall losses, even though severities are higher. However, reserve accounts do involve trade-offs for both homeowners and lenders, and more study and testing are needed to determine the optimum amount and duration of reserves and the conditions under which the reserves can be used, as well as to answer more detailed operational questions. The authors outline a blueprint for piloting a mortgage reserve account program that could generate a critical mass of evidence to inform further product development.

This report is the third in a series of four developed through a two-year, $1.5 million collaboration between the Urban Institute and FHLBank San Francisco. Previous reports examined incorporating alternative data into mortgage underwriting and mitigating the impact of student debt on Black homeownership. Future research will address using artificial intelligence and other new technologies to overcome historical mortgage lending biases.

To read the full report, including more data, charts, and methodology, click here.